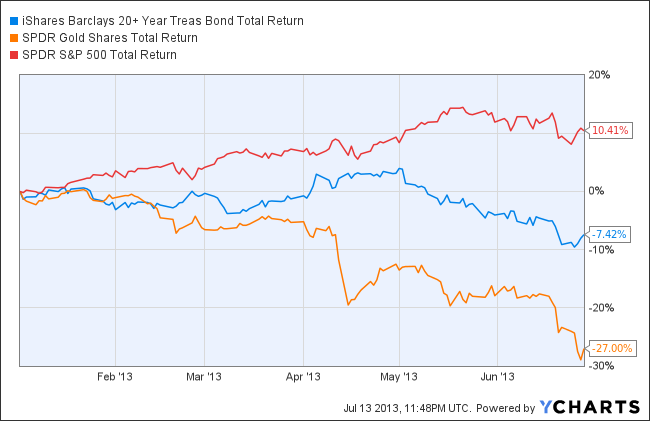

Second quarter and year-to-date 2013 was not kind to long-term U.S. Treasuries (TLT) and gold (GLD). With higher-than-expected job creation reported and ongoing Fed talk about QE “tapering”, U.S. Treasuries and gold took a shellacking as investors fled the party before the punch bowl was taken away.

In 2013, U.S. Treasury bonds and gold have cratered to new-52 week lows falling 7.42% and 27.00%, respectively, while equities (SPY) have climbed 10.41%. See chart below.

After the fallout in Treasuries, Fed Chairman Ben Bernanke wasted little time to reassure markets by announcing that a “highly accommodative monetary policy for the foreseeable future is what’s needed in an economy plagued by high 7.6% unemployment and low 1% inflation.”

The markets promptly jumped on Bernanke’s pro-QE comments. The three major equity averages all rose better than 1%. Additionally, Treasury and gold prices advanced while the U.S. dollar plunged in the wake of Bernanke’s comments.

To calm QE-holics, Bernanke reiterated, “It may well be sometime after we hit 6.5% unemployment before rates reach any significant level. There is some prospective, gradual and possible change in the mix of instruments, but that shouldn’t be confused with the overall thrust of policy which is highly accommodative.”

With Bernanke’s foot on the QE pedal and equity markets reaching all time highs, we remain cautiously optimistic. It’s safe to say that the low-hanging fruits are few and far between today. In that light, we were able to add two new positions in the second quarter.

The larger of the two acquisitions was Dell Inc. (DELL). Dell is currently in a proxy battle between founder and CEO Michael Dell and private equity firm Silver Lake against major shareholders Carl Icahn and Southeastern Asset Management.

The Special Committee of the Board of Directors of Dell has backed Dell and Silver Lake’s offer to take the company private in an all-cash deal valued $24.4 billion or $13.65 per share. Icahn and Southeastern are urging investors to vote against the deal at the Special Meeting of Shareholders scheduled for July 18, 2013. Stay tuned.

Whether the deal gets voted down or not, we believe we are in a good position to win either way. A $13.65 buyout would be accretive to the portfolio immediately. A stay public outcome would likely result in share price erosion in the short-term, but an overall higher long-term gain (albeit with higher uncertainty/risk).

As we head into the third quarter, the portfolio remains defensively positioned due to higher general market valuations. While we believe it’s prudent to be cautious at these levels, we remain steadfast in our search for opportunities wherever when can find them. To learn more about Prudent Value, please click here.

The investments discussed are held in client accounts as of June 30, 2013. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.