Author: James Roberts

Author: James Roberts

Covestor models: Fortune’s Most Admired, StockDiagnostics, Best Ideas

On Feb. 6, Barron’s published its semi-annual Barron’s-Zacks ranking of Wall Street broker’s focus lists. It was not a pretty picture, with only one research firm achieving noteworthy results.

The most significant thing in the article with respect to my investment strategy was the fact that the Charles Schwab’s Stock Equity Ranking System ranked ninth for the six months surveyed with a return of -12.13%. The Schwab Equity Ranking continues to be a significant component of the fundamentally based strategy I use and its poor performance in 2011 offers support for my decision to decrease the relative importance of the Stock Equity Ranking System by adding three more inputs.

Those three inputs are the Starmine system offered through Fidelity, the monitored list by Dines Theory Forecast, and a ranking that I devised which rewards stocks with lower volatility. The result will be a less volatile portfolio which may produce lower overall returns.

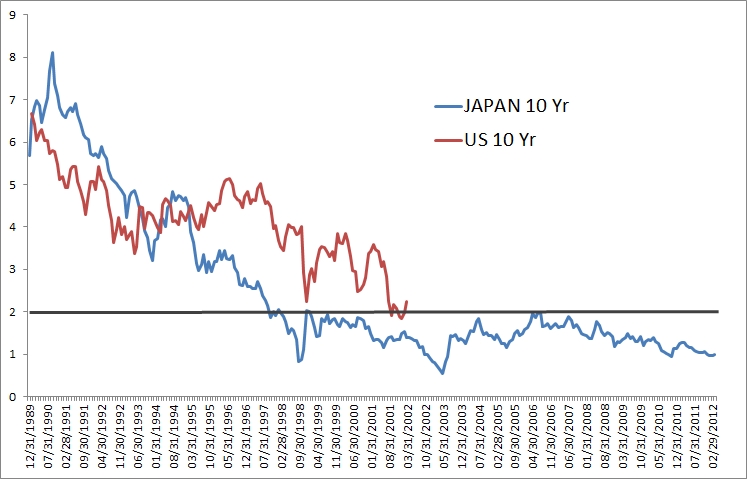

That is a price I am willing to pay, since my portfolios do not presently contain any bonds. Bonds are arguably the ideal addition to a portfolio to achieve a low correlation with the S&P 500. The Dines Theory portfolios contain an approximate 13% current weighting in ETFs that provide exposure to short term treasuries. I have trouble, however, in believing that the risk of increased interest rates is not great from current levels. Unfortunately, that sentiment kept me out of the best performing sector last year.

There are, however, several ways to achieve lower correlation with the S&P index. One that comes to mind is the inclusion of precious metals in a portfolio. Another is to lean towards companies that pay dividends as high as or higher than the S&P 500 Index. Master Limited Partnerships engaged in energy pipelines and infrastructure offer another way to get increased income factor to reduce volatility. There is an index available to track the performance of this sector: the Alerian MLP Index (AMZ and AMZX). This index tracks the 50 most prominent energy Master Limited Partnerships.

In addition to the Master Limited Partnerships, one could consider investing in the companies that act as general partners in the MLPs. Williams Companies (WMB) and Oneok (OKE) come to mind. Still another method of achieving lower correlation to the S&P Index is by including some companies that have a history of low correlation. I am researching an online service this month to help me in applying that idea to my portfolios.

{kind=link}