By: Kevin Flanagan, Head of Investment Strategy

Key Takeaways

- With the Fed potentially nearing the end of its rate-cutting cycle, 2026 is likely to bring continued steepening of the Treasury yield curve, reinforcing caution on long-duration bonds.

- A horizon analysis shows that ultra-short to intermediate-term maturities may offer positive returns, while longer-dated bonds risk underperformance amid rising back-end yields.

- Investors may find the most compelling opportunities in ultra-short strategies such as Treasury Floating Rates, which are well positioned in a flattening-to-steepening curve environment.

Within the fixed income arena, there have been three key issues that I have continually focused on over the last year or so: 1) yields returned to historically normal levels; 2) chasing duration has been a fleeting strategy; and 3) the path of least resistance is for the yield curve to steepen. For 2026, all three dynamics are likely to play out again in the money and bond markets. However, for this blog, I wanted to highlight what points #2 and #3 actually look like when put to the test.

What do I mean by ‘test’? A horizon analysis. For those not familiar with that term, in bond-land, a horizon analysis is a way to ‘shock’ a fixed income portfolio from an interest rate perspective. The analysis can be geared to scenarios in which yields fall, rise, remain flattish or reflect a combination of these outcomes. Remember, money and bond market yields along the maturity spectrum do not always move by the same magnitude in either a rising or falling rate setting, and in fact, may not even move in the same direction at all.

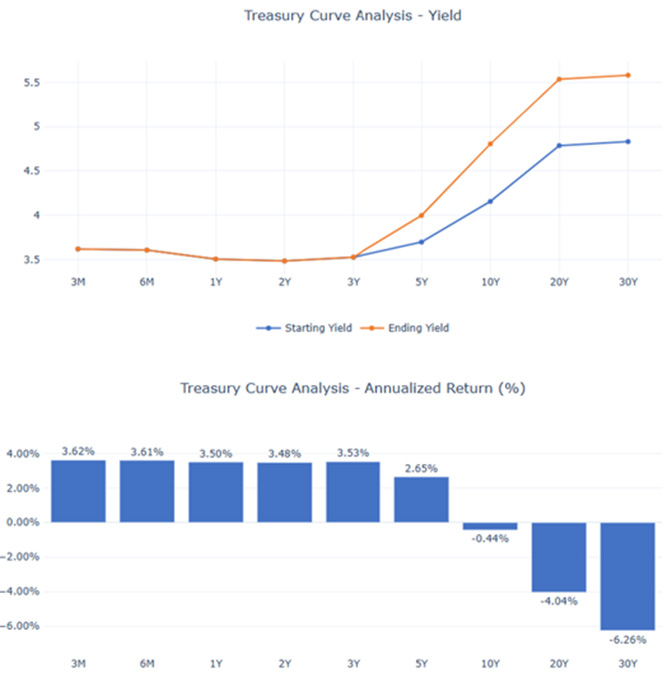

Source: WisdomTree, as of 12/31/25

For the horizon analysis in this blog, I utilized what could be a likely scenario for rates and the attendant yield curve, based upon WisdomTree’s 2026 Economic and Market Outlook.

Macro & Fed Assumptions

- Despite a ‘no hire, no fire’ labor market, the underlying economy remains in relatively good shape, with potential tailwinds from the One Big Beautiful Bill.

- While fears of tariff-induced price pressures have been reduced, inflation remains ‘sticky’ and above the Fed’s 2% target

- Fed policy is still skewed towards further easing, but we could be nearing, or at, the end of this rate cut cycle

Treasury Yield Assumptions

- Ultra-short- and short-term rates will be flat to moderately lower, reflecting Fed policy

- Intermediate to longer-term rates could experience upward pressure with any potential increases being more visible at the back-end of the curve

- The Treasury yield curve will more than likely continue to steepen

The Horizon Analysis

For the horizon analysis outlined here, I kept T-bill and short-term UST yields essentially unchanged while progressively increasing yields for the 5-year through 30-year maturities higher. As shown, the result is a yield curve that visibly steepens from its starting point The most important aspect of this exercise is what happens to annualized returns (the bottom bar chart). While the 3-month through 5-year maturities all produce positive results, the 10-year to 30-year part of the curve comes in on the negative side of the ledger.

Conclusion

The anticipated rate and yield curve scenario argues against extending duration. In fact, ultra-short options, such as Treasury Floating Rates, would potentially have the best positive return since they are referenced to the 3-month T-bill.

Originally posted on January 14, 2026 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/Santima+Suksawat

VIA SHUTTERSTOCK

DISCLOSURES

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Alejandro Saltiel, Andrew Okrongly, Behnood Noei, Bradley Krom, Brendan Loftus, Brian Manby, Christopher Gannatti, David Graichen, Hyun Ku Kang, Jeff Weniger, Jeremy Schwartz, Jonathan Steinberg, Joseph Grogan, Joseph Tenaglia, Kara Dombroski, Kevin Flanagan, Lauren Pfendt, Liqian Ren, Lonnie Jacobs, Matt Wagner, Rick Harper, Ryan Krystopowicz, and Vanya Sharma are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}