By: Dane Smith, Head of North American Investment Strategy and Research

We highlight distinct areas of the US market that warrant attention as we begin the new year. These focus areas may overlap or diverge in their impact and relevance.

Introduction

We begin the year optimistic about 2026. However, we recognize that institutional investors face a dynamic landscape shaped by stretched valuations, evolving AI adoption, and persistent macro risks, as geopolitics and shifting US policies continue to impact asset allocation. We emphasize the need for diversified portfolios, selective sector exposure, and a focus on quality, despite the constructive backdrop.

1. Geopolitics and US policy

We revised our 2026 growth estimates higher due to expected tax refunds, ongoing deregulation, robust capex continuing, and easier financial conditions. However, policy uncertainty remains elevated heading into the midterms, as trade and immigration frameworks remain fluid.

Geopolitical tensions—spanning Russia/Ukraine, Venezuela, Iran, China, and even NATO allies—remain mostly discounted by markets, but still affect supply chains, foreign exchange (FX) dynamics, and risk premia. For example, sovereignty-driven industrial policy is redirecting capex toward strategic technology and energy sectors, often at higher cost structures.

Investment implications:

Expect short-lived, episodic shocks around major political dates and policy headlines. These shocks heighten the importance of asset allocation and risk repricing, where capital flows may increasingly support gold and a more dynamic currency view.

2. The US consumer

Consumption accounts for roughly 68% of US GDP.1 Core inflation should moderate as the Fed delivers non recessionary rate cuts (our baseline is for ~50-75 bps of cuts in 2026). While this should ease borrowing costs, affordability pressures for lower income cohorts will persist. Consumer strength is therefore likely to remain K-shaped.

While our outlook is constructive, wage indicators across employer and worker surveys (Average Hourly Earnings, Employment Cost Index, Atlanta Fed Wage Growth Tracker) suggest cooling wage growth heading into late 2025, underscoring that the labor market is the key macro risk for 2026.

Investment implications:

A softer US dollar could benefit emerging markets. Equity positioning should be selective across discretionary and macro-sensitive sectors, such as industrials and financials (Figure 1). In fixed income, we continue to expect curve steepening and see opportunity in securitized non-agency investment grade (IG) bonds, including mortgage-backed securities.

3. AI industrialization

The coming year marks a transition from hype—exemplified by the Magnificent 7’s five year cumulative return of 173%2—to enterprise-level AI buildout.

If what we observe in geopolitics is the symptom, the structural implications of AI dominance are the root cause.

We think that AI is not a bubble, but instead a fundamental driver of markets and policy, and a key differentiator of global power moving forward.

This year, data centers, semiconductors, and software deployments are set to scale further, with productivity gains emerging first in tech-adjacent verticals (industrial automation, healthcare IT, energy infrastructure), before broader diffusion.

To be clear, 2026 is likely too soon to see AI deliver major economy-wide productivity gains. But we do expect the beginnings of ROI in specific areas (see tech-adjacent verticals).

Investment implications:

Consider a barbell approach between AI infrastructure enablers (cloud, semiconductors, power, and thermal systems) and operational adopters with margin leverage. Monitor electricity markets and grid-related capex bottlenecks.

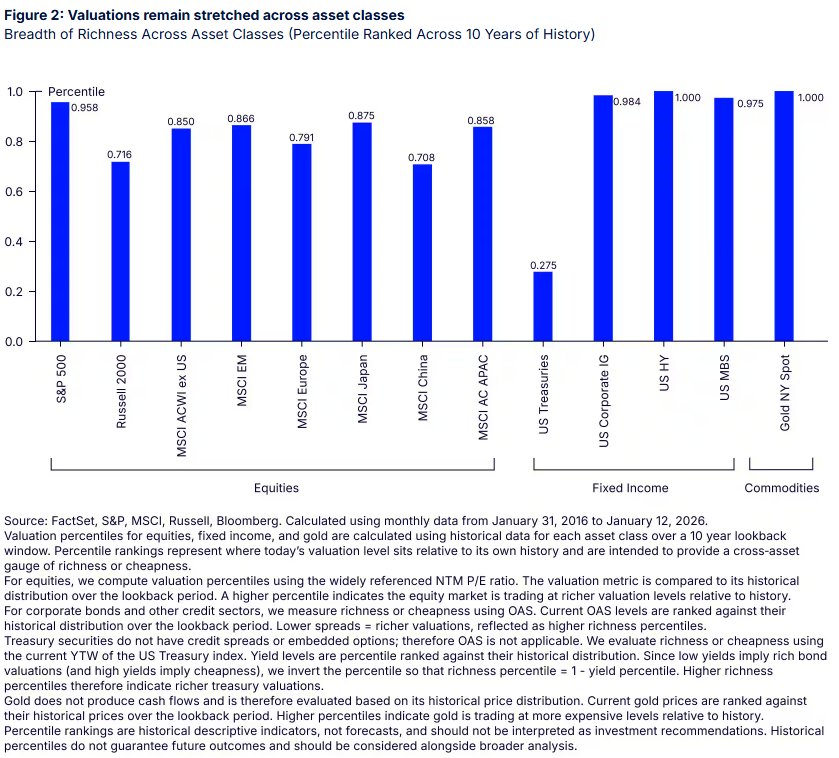

4. Valuations (Everything is rich!)

Across equities, credit, and private markets, elevated valuations define the cross-asset backdrop heading into 2026 (Figure 2). US equities trade near cycle high multiples amid disinflation and policy hopes; credit spreads remain tight versus long-run medians; and private assets face exit and liquidity constraints. Some estimates for North American private-equity buyouts are at more than seven years,3 as IPO windows and secondaries reopen gradually.

Tight spreads reflect economic confidence but also intense demand for income, as IG issuance remains active despite some slow-down (1H2025) in non-IG segments in response to policy uncertainty. On the corporate side, companies with strong cash flows, compelling ROI, and healthy balance sheets are best positioned to support higher valuations.

Investment implications:

Diversify with real assets and alternatives, and build portfolio resiliency. Investors can consider tilting to active management over passive, and exploiting valuation dispersion.

5. US exceptionalism

The “US leader” investment narrative took a hit in 2025, as the MSCI World ex US outperformed the US (+14.7%, with the US dollar down ~9.4%). But US exceptionalism isn’t over yet. Early 2026 demand should benefit from ~$100 billion in tax refunds4 and continued corporate full expensing, which will support consumption and capex. AI-related capex alone is projected to exceed $500 billion.5

S&P 500 earnings growth is expected to reach 14.8% for CY 2026,6 outpacing most major regions. The debate continues over the “push and pull” of capital, where the US could begin getting capital back as valuations no longer look as attractive overseas, and fundamentals become a primary driver of equity returns again. However, investors’ concerns about aggressive foreign policy in the US could weaken capital flows to the US.

US Treasuries remain dominant—representing ~68% of global sovereign issuance and 45% of corporate issuance. While competing forces shape long-end yield dynamics, the unparalleled depth and liquidity of Treasuries—especially during periods of geopolitical stress—reinforce their appeal versus other markets. Baseline 2026 forecasts project US growth at ~2.4%,7 beating consensus expectations and running significantly ahead of Europe and APAC, where trajectories remain more modest and uncertainty persists.

Investment implications:

Lean into US cyclicals with pricing power and AI-linked capex exposure. Balance rate risk amid curve steepening, while maintaining selective ex-US exposure where fiscal stance and FX create positive carry.

Originally posted on January 15, 2026 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/GoodStudio

VIA SHUTTERSTOCK

FOOTNOTES:

1 Bureau of Economic Analysis and Federal Reserve Economic Data (FRED).

2 FactSet, State Street Investment Management.

3 S&P Global.

4 US Treasury Department.

5 State Street Investment Management and FactSet.

6 FactSet.

7 State Street Investment Management.

DISCLOSURES:

Marketing Communication

Important Risk Information

Investing involves risk including the risk of loss of principal.

Information Classification: General

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

The views expressed are the views of Dane Smith through the period ending January 14, 2026, and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward- looking statements. Please note that any such statements are not guarantees of any future performance, and actual results or developments may differ materially from those projected.

Diversification does not ensure a profit or guarantee against loss.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

International Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions. Investments in small-sized companies may involve greater risks than in those of larger, better known companies. Investments in mid-sized companies may involve greater risks than in those of larger, better known companies, but may be less volatile than investments in smaller companies.

There are risks associated with investing in Real Assets and the Real Assets sector, including real estate, precious metals and natural resources. Investments can be significantly affected by events relating to these industries.

Investing in foreign domiciled securities may involve risk of capital loss from unfavorable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

Past performance is not a reliable indicator of future performance.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data. State Street Investment Management, One Congress Street, Boston, MA 02114.

{kind=link}