Originally posted on February 27, 2026 on SSGA blog

Learn how economic factors uniquely impact different asset classes — and why macroeconomic-environmental diversification, not just asset class diversification, may help build wealth over the long-term.

The world around us is constantly changing, and these changes impact financial markets in a variety of ways. Inflation is up, monetary policies evolve, trade tariffs are revised, economies witness growth revisions—all these changes affect financial markets and individual asset classes differently.

Understanding the impact of different economic factors may help investors better prepare their portfolios to be more resilient to macro shocks and market surprises across different environments.

What kinds of factors affect markets?

Various types of economic factors, from macro to micro to geopolitical ones, all can uniquely impact asset class performance, so let’s take a closer look at each.

Macroeconomic factors

Due to their direct impact on consumers’ spending power, macroeconomic factors tend to have a far-reaching impact on money flowing into the economy. These factors include:

Interest rates: In a high-interest-rate environment, borrowing costs increase, potentially reducing consumer spending and business investment. Conversely, in a low rate environment, spending power potentially increases as borrowing costs tend to decrease, boosting business investment.

Inflation: In an inflationary environment, consumers’ spending power can decrease as the cost of goods increases. The reduced flow of money into the economy affects businesses as people conserve cash, choosing to spend only on essentials and to forego luxuries.

Economic growth: Most often tracked by the GDP of a country, economic growth is an indicator of the overall prosperity of a country. Economic growth tends to result in increased consumer spending and business investment. Resulting corporate profits enable businesses to expand further.

Currency movements: In our global economy, currency movements play a vital role in market movements. Cross-border and international trade are greatly impacted by exchange rates. A stronger currency may give businesses more purchasing power while devaluing export opportunities. Inversely, a weak currency can make imports more expensive. All this impacts trade and the cross-border flow of goods for an economy, leading to a potential drag or boost to growth.

Microeconomic factors

Microeconomic factors have more targeted and direct impacts on specific sectors or industries, or even on individual companies. These factors include:

Industry landscape: Changes in trends or consumer behavior can impact an industry’s prospects over time. These changes force companies to adapt and innovate. For example, scientific data and increased health awareness have impacted the fast food and tobacco industry as consumers are growing increasingly health conscious.

Technological advancements: Technological improvements and their adoption can have direct and indirect impacts on multiple sectors based on the nature of the improvement, propelling innovative companies and making others obsolete. Most recently this can be seen in the use of artificial intelligence (AI). The Tech sector got a major boost as companies adopted the use of AI in their processes and non-Tech companies that embraced AI innovation enjoyed greater investor confidence.

Geopolitical and global factors

In a global economy, international relations play an increasingly important role in shaping the economies of individual countries and larger global economic prospects. These factors include:

Global crises: Crises that affect a significant part of the world can have ripple effects for economies. Natural disasters, pandemics, global shortages, and climate change are some examples of these. Due to their unexpected and often unprecedented nature, they can have crippling effects on countries and companies that aren’t adequately prepared.

Geopolitical conflicts: War-affected regions can create uncertainty in financial markets as exports, imports, and trade routes become affected and resource availability from the affected region impacts dependent nations.

Trade and tariff policies: Changes in policies affect import and export duties and the availability of resources. These not only affect costs, but also have downstream impacts on the availability of raw materials for industries.

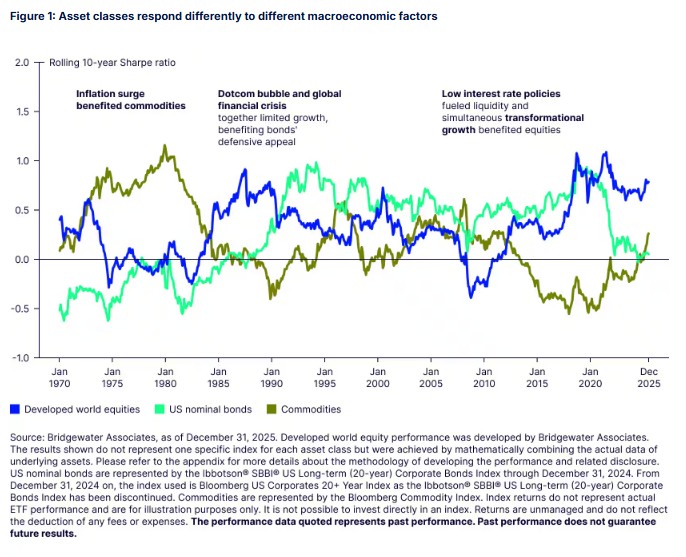

How asset classes have reacted to changes in economic environments

In the past, unexpected global, macroeconomic, and environmental changes have increased volatility and impacted markets. They’ve led to sudden shocks from which the market took days, weeks, and even months or years to recover.

Here are four examples, two recent and two more than 30 and 50 years ago, to show that while market trends change, the impact of economic factors on asset class performance may be more reliable.

COVID-19 pandemic, 2020: Growth shock

On March 11, 2020, as economic outlooks changed unexpectedly following the World Health Organization (WHO) declaring the COVID-19 outbreak a global pandemic, markets saw dramatic movements. And given the severity of the health crisis, this resulted in a growth shock.

The global stock market fell by 34% from its pre-pandemic high before fully recovering by August 2020 following aggressive fiscal and monetary policies.1 Conversely, bond markets rallied as rates fell once the growth outlook was revised lower—a factor boosting demand for gold but restraining broader commodity prices.2

Here, assets with a positive bias toward falling growth would have balanced out assets with a negative bias to falling growth, as illustrated below by the subsequent three-month returns from stocks’ pre-pandemic high.

High inflation, 2021-2022: Inflation shock

Inflation spiked following the pandemic to over 5% by mid-2021 and then to over 9% by mid-2022.3 To curb rampant inflation, the Federal Reserve (Fed) raised interest rates from 0.25% to 5.5% throughout 2022 and into 2023. Other central banks hiked rates too, as inflation surged globally.

Global equities fell, as high inflation eroded purchasing power and recession fears rose. While growth was falling, the inflation shock and the coordinated rise in rates across global central banks impacted bonds’ principal future value. But inflation-sensitive assets rose.

Here, bonds didn’t diversify stocks, as falling growth limited stocks’ potential while falling inflation impacted bonds.

Russian default crisis, 1998: Growth shock

In the summer of 1998, the Russian government defaulted on its debt and devalued its currency, the ruble. This occurred while many East Asian nations were still trying to repair their local economies following the 1997 Asian Financial Crisis.

Fears of additional non-developed countries facing a run on their currency, and questions about the nations’ solvency, led to increased market volatility and spillover risk. The crisis impacted currency and commodity markets and contributed to a decline in global growth. It also had far-reaching impacts beyond emerging market nations, including the collapse of US hedge fund Long Term Capital Management that required a Fed bailout.

Global equities then fell by more than 20% from pre-crisis highs over three months. Here, bonds provided the most balance given their relationship to falling growth, while positive growth assets faced challenges. Given the region’s relationship to commodity supply chains, inflation expectations increased—offsetting some of the demand-driven impacts to commodity prices during those three months when the crisis was at its peak.

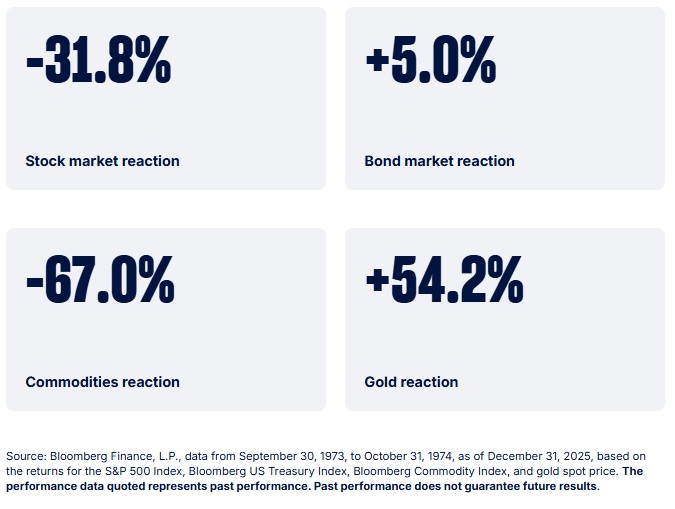

Oil crisis, 1973: Growth and inflation shock

In October of 1973, the Organization of Arab Petroleum Exporting Countries (OAPEC) announced an oil embargo that would ban oil exports to the US. This put a strain on the US economy, given its dependence on foreign oil. The supply shock caused energy shortages, elevated inflation, and a global economic crisis.

US equities fell 32% over the following year, while inflation-sensitive commodities and gold soared over 50%. Bonds produced a positive return, but not on a real return basis as inflation spiked to over 12% and yields on cash-like Treasury Bills exceeded that of US 10-year Treasurys.4

Counter changing economic environments with balance

Diversification can help reduce the impact of sudden upsets in the stock and bond markets. But, as described above:

- Sometimes, economic factors can negatively affect both stock and bond markets

- Concentration risk can develop even in a 60/40 portfolio

- Inflation can erode your principal, whether it’s invested in stocks or bonds

Taking a more active approach to portfolio allocation can help mitigate the damage from sudden market shifts—and even potentially help portfolios adapt more readily, or be more resilient, to changing environments. But tracking changing environmental factors and how they could impact different asset classes is not easy. And if multiple factors are at play at once, factoring all in could lead to some real analysis paralysis!

The bottom line—there are factors we know will affect markets and others we simply never see coming. The best approach may be to build portfolios that balance risks across growth and inflation environments. That way, instead of struggling to predict the shifts that may lie ahead, you’re prepared to perform in any season, no matter which way the economic winds blow.

PHOTO CREDIT: https://www.shutterstock.com/g/Red_Vector

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES:

1 Bloomberg Finance, L.P., as of December 31, 2025, based on MSCI ACWI Index returns. The performance data quoted represents past performance. Past performance does not guarantee future results.

2 Bloomberg Finance, L.P., as of December 31, 2025, based on the Bloomberg US Treasury Index, gold spot price, and Bloomberg Commodity Index. The performance data quoted represents past performance. Past performance does not guarantee future results.

3 Bloomberg Finance, L.P., based on US CPI year-over-year changes, as of December 31, 2025.

4 Bloomberg Finance, L.P., data from September 30, 1973, to October 31, 1974, based on CPI year-over-year changes, St. Louis Federal Reserve based on US 10-Year and US 3-month Treasury bill rates, as of December 31, 2025. The performance data quoted represents past performance. Past performance does not guarantee future results.

DISCLOSURES:

Investing involves risk including the risk of loss of principal.

The performance data quoted represents past performance. Past performance does not guarantee future results.

Diversification does not ensure a profit or guarantee against loss.

Index returns reflect capital gains and losses, income, and the reinvestment of dividends. Index returns are unmanaged and do not reflect the deduction of any fees or expenses.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing in commodities entail significant risk and is not appropriate for all investors. Commodities investing entail significant risk as commodity prices can be extremely volatile due to wide range of factors. A few such factors include overall market movements, real or perceived inflationary trends, commodity index volatility, international, economic and political changes, change in interest and currency exchange rates.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.