By: Kevin Flanagan, Head of Fixed Income Strategy

Key Takeaways

- After a sluggish start, the Treasury yield curve steepening gained momentum in late 2025 as the Federal Reserve cut rates by 75 basis points over three months, driving short-term yields lower.

- With moderate economic growth and inflation likely to stay above 2% in 2026, longer-term yields could rise while short-term rates stay flat, further steepening the curve.

- An active/passive bond barbell strategy offers investors a timely way to lock in income while maintaining a shorter duration than the benchmark Agg, aligning with evolving yield curve dynamics.

As we get ready to close out 2025, one stand-out trend in the U.S. Treasury (UST) market has been the steepening of the yield curve. The question now is whether this trend will continue into 2026, and if it does, how should investors position their bond portfolios? The answer: the active/passive barbell.

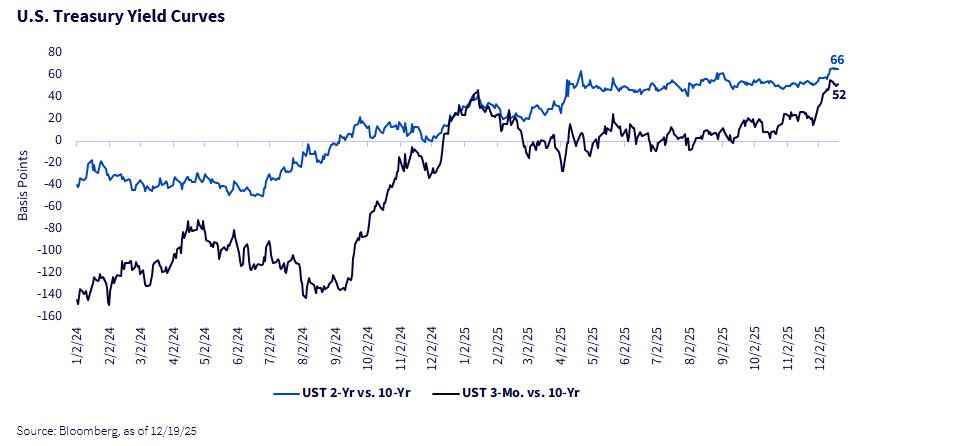

When examining the Treasury yield curve, the two prominent measures to be analyzed are the 3-month/10-year and 2-year/10-year constructs. As the graph clearly illustrates, calendar year 2025 finally brought both spreads into positive territory. As one would expect, the reversal in the trade from curve inversion, or negative differentials, to readings on the plus side of the ledger began with the Federal Reserve’s first rate cuts in September 2024.

However, as you can see, the initial steepening trade following the 2024 Fed rate cuts kind of ran out of gas. It really wasn’t until the Fed kick-started round two of rate cuts in this easing cycle that the curve steepener trade returned in a more visible fashion. Specifically, it was the 3-mo/10-yr construct that has recently experienced this trade. Given the direct correlation of the 3-month t-bill yield to the Fed Funds Rate, this should come as no surprise, given the fact the Fed has now cut rates by 75 basis points over the last three months. The 3-month yield was catching up to what the 2-year note had already discounted regarding where the Fed Funds Rate was headed. As a result, the spreads between these two curves are now closer to being aligned.

What Will 2026 Have in Store?

For next year, it appears as if the path of least resistance would be for the curve steepener trade to continue. Perhaps the most intriguing question is how it will steepen. Remember, it really is just math. The yield curve direction will be predicated on the two maturities you are measuring in terms of yield. Our baseline for next year is that the economy is going to post moderate growth and inflation will remain above the Fed’s 2% target. Against this backdrop, and one of a Fed with a ”house divided,” short-term yields, or the front-end of the curve, would probably be flattish or perhaps could drift a bit lower. Longer-dated maturities (the back-end of the curve), however, could witness an increase in yields. Hence, the yield curve steepens.

Conclusion

So, back to the beginning. The active/passive bond barbell allows investors to have flexibility in their income and duration positioning. It provides a means to lock in income while keeping the duration profile below that of the benchmark Agg.

Originally posted on December 24, 2025 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/nastudios

VIA SHUTTERSTOCK

DISCLOSURES

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Alejandro Saltiel, Andrew Okrongly, Behnood Noei, Bradley Krom, Brendan Loftus, Brian Manby, Christopher Gannatti, David Graichen, Hyun Ku Kang, Jeff Weniger, Jeremy Schwartz, Jonathan Steinberg, Joseph Grogan, Joseph Tenaglia, Kara Dombroski, Kevin Flanagan, Lauren Pfendt, Liqian Ren, Lonnie Jacobs, Matt Wagner, Rick Harper, Ryan Krystopowicz, and Vanya Sharma are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.