By:

Lee Clements, Director, Applied SI Research, FTSE Russell

Alexis R. Rocamora, Sustainable Finance & Investment Lead – Asia Pacific, LSEG

The GX transition programme, what it means for investors and how sustainability data and transition indices can help to navigate it.

- Japan’s GX (green transformation) strategy is a broad, ambitious and well-financed transition plan that is designed to cut carbon emissions, improve energy efficiency and boost green innovation.

- Under the plan, ¥3.7 trillion of government transition bonds have already been issued and mandatory emissions trading will start in 2026.

- Carbon intensity, transition efforts and green revenues exposure will become key attributes for assessing the economic potential of Japanese companies.

- LSEG can help with comprehensive SI data covering carbon intensity, TPI climate transition metrics and green revenues. FTSE Russell offers multiple Japanese climate transition equity indices utilising these metrics to help investors allocate capital.

As the world faces the concurrent challenges of the energy transition, energy security and slowing economic and productivity growth, Japan’s government has launched an ambitious $1trn transition plan called the GX (green transformation) strategy. The GX strategy aims to cut emissions, improve efficiency and boost green innovation throughout the Japanese economy.

The GX transition programme

The announcement of Japan’s GX Strategy by Prime Minister Kishida in December 20221 was followed by a series of key policy announcements by successive governments in 2023 and 2024, aiming to guide the strategy’s implementation2.

The GX policy aims to help Japan achieve its 2030 and 2050 climate change targets3 by shifting to clean energy, driving economic growth, and by mobilising ¥150trn ($1 trn) in public-private investments over 10 years. Its implementation relies on two pillars:

- A Green Transformation based on the stable supply of energy: this involves the promotion of energy saving, an increase in renewable energy generation, the use of nuclear power, and support for research and development (R&D) in other technologies, such as the use of hydrogen and ammonia as energy sources and carbon capture and storage (CCS).

- Growth-oriented carbon pricing: this includes the issuance of ¥20trn ($134 bn) of sovereign GX Transition Bonds in 10 years to support upfront investments, the implementation of carbon pricing mechanisms to incentivise GX investments, and enhancements to the financing of support programs for public-private partnerships.

As part of its growth-oriented carbon pricing framework, the GX policy will introduce an emissions trading scheme – called GX-ETS – for carbon intensive sectors4 from financial year 2026, including allowance auctioning for power generation companies from financial year 2033, as well as a carbon levy targeting fossil fuel importers from financial year 2028. These measures will finance the issuance of the GX Transition Bonds, which will serve as a springboard to spur private investments to help meet the promised ¥150trn target5.

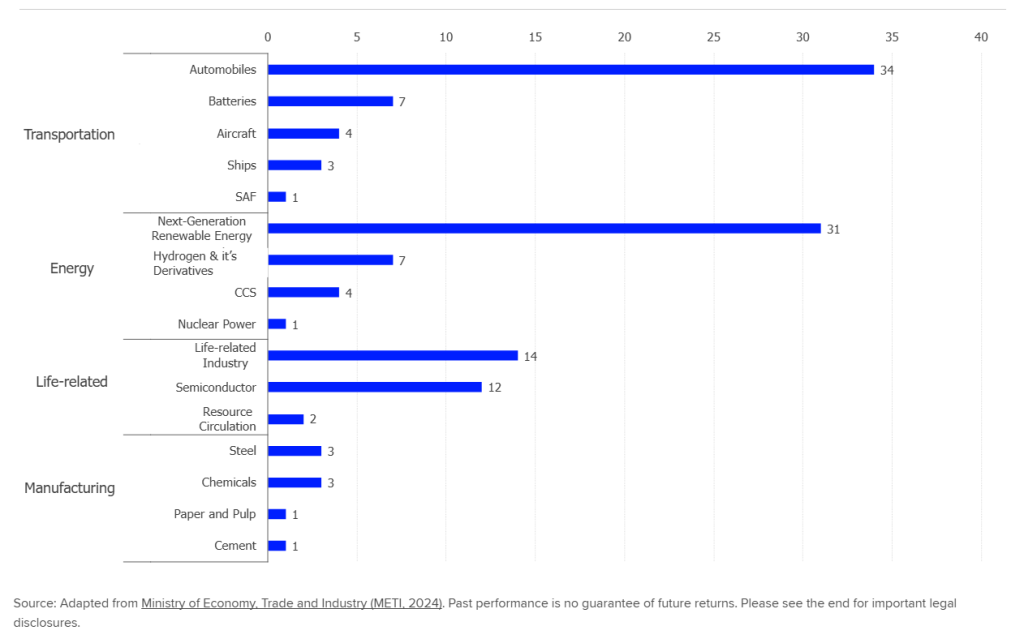

In addition, financial support mechanisms—including the Green Innovation Fund, the Economic Security Fund, various tax credits, debt guarantees and supplementary fiscal budgets—are being deployed through public-private partnerships as a way to fund the investments in the technology types shown in the chart below.

AMOUNT OF PUBLIC & PRIVATE INVESTMENT TARGETED UNDER THE GX PROGRAM BY TECHNOLOGY TYPE (in ¥trn)6

Source: Adapted from Ministry of Economy, Trade and Industry (METI, 2024). Past performance is no guarantee of future returns. Please see the end for important legal disclosures.

Unlike most environmental and climate policies in Japan — which are typically initiated by the Ministry of the Environment — GX falls under the purview of the Cabinet Secretariat and the Ministry of Economy, Trade and Industry (METI), reflecting a distinct approach to policy leadership and accountability7. The GX Acceleration Agency was established in 2024 to support the implementation of the GX policy with regards to financial mechanisms, ETS operations, carbon levy collection and research8. Furthermore, the program is supported by the GX League, a forum for cooperation between companies, government and academia established in April 2022, including – as of September 2025 – 747 companies, representing over 50% of Japan’s greenhouse gas (GHG) emissions9.

The GX plans are already far beyond the theoretical phase, with ¥3.7trn ($24.7 bn) already raised by sovereign transition bonds10 and Japanese utilities starting to issue transition bonds to fund projects such as the restarting of nuclear reactors. As we look to 2026, transition bond issuance has the potential to accelerate as the emission trading scheme becomes mandatory.

Carbon intensity, transition and green revenues become key attributes of future growth for Japanese corporates

As the GX policies help to re-orientate the Japanese economy towards low-carbon growth and greater energy efficiency, climate metrics will become increasingly vital in analysing the risks and opportunities faced by Japanese companies:

- The emissions trading scheme and carbon levy will make understanding a company’s carbon intensity – both absolute and relative to its sector peers – critical in assessing its future carbon-related costs.

- As trillions of yen in transition funding will reward those companies that are actively decarbonising, assessing companies’ transition efforts will become crucial in understanding their eligibility for financial support from the GX policy.

- Finally, with funding also directed to the Green Innovation Fund and rising demand for green products and services, determining a company’s exposure to green revenues will be an important indicator of its growth potential.

Originally posted on October 15, 2025 on LSEG blog

PHOTO CREDIT: https://www.shutterstock.com/g/image_ninja

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES:

1 http://www.meti.go.jp/press/2022/12/20221223011/20221223011.html

2 See notably http://www.meti.go.jp/press/2022/02/20230210002/20230210002.html, https://laws.e-gov.go.jp/law/505AC0000000032, https://cdnw8.eu-japan.eu/sites/default/files/imce/2024.4.18%20METI.pdf and https://www.jaif.or.jp/en/news/7079

3 Japan’s climate targets include a carbon neutrality target (established by Japan’s Green Growth Strategy in December 2020) and an intermediary emissions reduction target of 46% by 2030 (established by Japan’s Strategic Energy Plan in October 2021)

4 Companies emitting >100,000 tons of CO2 per annum, primarily steel, power and chemical

5 https://www.lseg.com/en/insights/ftse-russell/grjapan.com/sites/default/files/content/articles/files/gr_japan_overview_of_gx_plans_january_2023.pdf

6 NB: The total doesn’t exactly add up to ¥150 trillion as those figures include cross-sectoral measures.

7 http://japan.influencemap.org/policy/GX-Green-Transformation-5477

8 https://www.gxa.go.jp/en/

9 https://gx-league.go.jp/member/

10 Between FY2023 and FY2025, Japan has issued or planned to issue a total of ¥3.6671 trillion in GX Economy Transition Bonds, broken down as follows: ¥1.5401 trillion in FY2023, ¥1.4012 trillion in FY2024, and ¥0.7258 trillion in FY2025. Read more in this document from Japan’s Ministry of Finance

DISCLOSURES:

© 2025 London Stock Exchange Group plc and its applicable group undertakings (“LSEG”). LSEG includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) FTSE Fixed Income Europe Limited (“FTSE FI Europe”), (5) FTSE Fixed Income LLC (“FTSE FI”), (6) FTSE (Beijing) Consulting Limited (“WOFE”) (7) Refinitiv Benchmark Services (UK) Limited (“RBSL”), (8) Refinitiv Limited (“RL”) and (9) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, WOFE, RBSL, RL, and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “FTSE4Good®”, “ICB®”, “Refinitiv” , “Beyond Ratings®”, “WMR™” , “FR™” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of LSEG or their respective licensors and are owned, or used under licence, by FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, WOFE, RBSL, RL or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator. Refinitiv Benchmark Services (UK) Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by LSEG, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical inaccuracy as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of LSEG nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or LSEG Products, or of results to be obtained from the use of LSEG products, including but not limited to indices, rates, data and analytics, or the fitness or suitability of the LSEG products for any particular purpose to which they might be put. The user of the information assumes the entire risk of any use it may make or permit to be made of the information.

No responsibility or liability can be accepted by any member of LSEG nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any inaccuracy (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of LSEG is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of LSEG nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing in this document should be taken as constituting financial or investment advice. No member of LSEG nor their respective directors, officers, employees, partners or licensors make any representation regarding the advisability of investing in any asset or whether such investment creates any legal or compliance risks for the investor. A decision to invest in any such asset should not be made in reliance on any information herein. Indices and rates cannot be invested in directly. Inclusion of an asset in an index or rate is not a recommendation to buy, sell or hold that asset nor confirmation that any particular investor may lawfully buy, sell or hold the asset or an index or rate containing the asset. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index and/or rate returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index or rate inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index or rate was officially launched. However, back-tested data may reflect the application of the index or rate methodology with the benefit of hindsight, and the historic calculations of an index or rate may change from month to month based on revisions to the underlying economic data used in the calculation of the index or rate.

This document may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of LSEG nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of LSEG. Use and distribution of LSEG data requires a licence from LSEG and/or its licensors.