The Atlas Global Downside Protected (GDP) equity strategy is designed with the goal of addressing the three most important issues faced by equity investors:

Do current market conditions favor a relatively high, or relatively low, portfolio allocation to public equities?

How should equity investments be allocated across geographies?

What’s a good way to avoid being harmed by the periodic severe bear markets experienced by equity investors?

Performance

The MSCI All-Country World ETF (ACWI) was down-0.7% in February 2016.

GDP strategy performance was up 0.1%, which was 0.8% better than the index. From strategy inception on June 9, 2015 through the end of February 2016, the GDP strategy has a loss of 8.9%.

That is 2.9% better than the loss of 11.8% for the MSCI global equity index over the same period.

What Worked

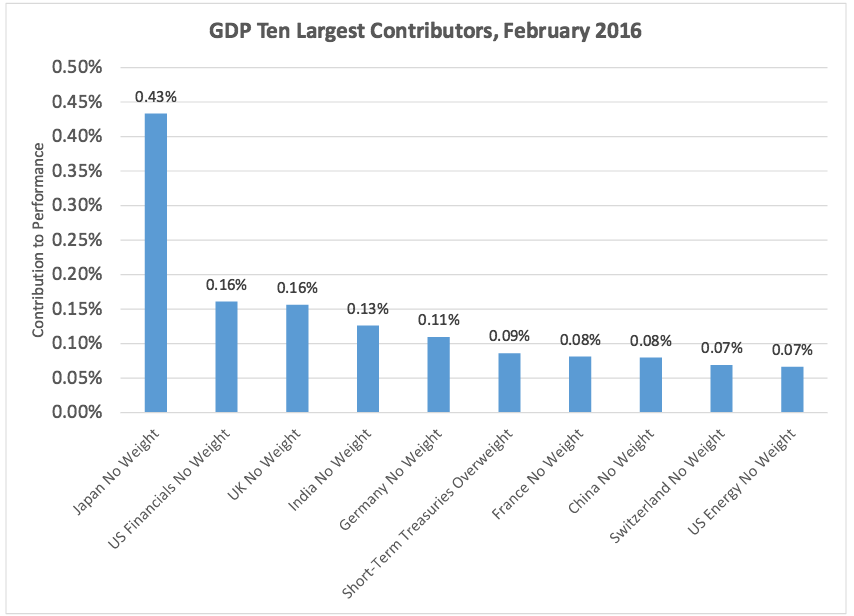

Exhibit A shows the ten largest contributors to the performance relative to the index in February.

About half of the markets had losses in February, and being underweight or out of those markets helped relative performance.

In particular, the strategy benefited from underweighting Japan, which was down 5.3% in February.

What Didn’t

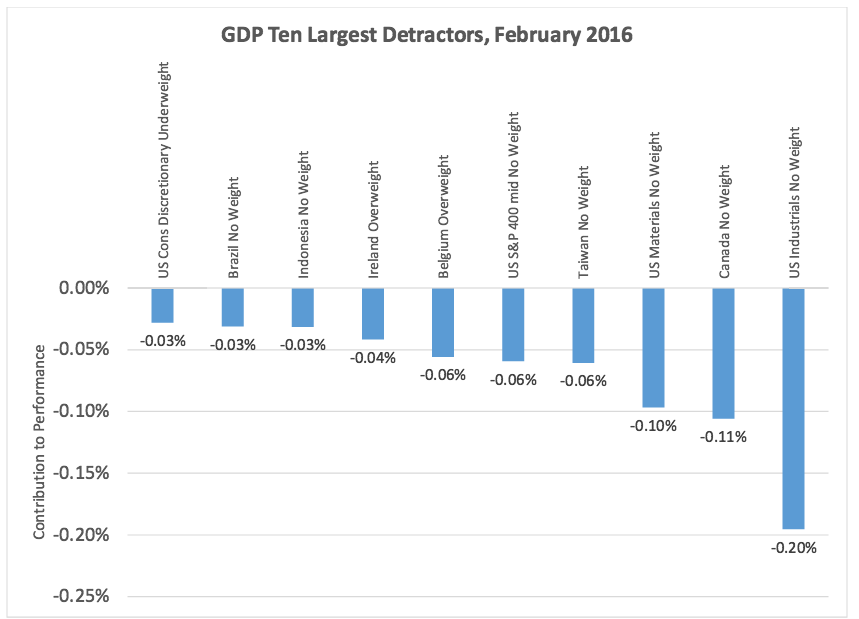

Some markets that we had avoided bounced back in February.

Exhibit B shows the ten largest detractors to performance relative to the index.

The largest detractor was being out of the US Industrials sector, which gained 4.3% in February.

Rebalance

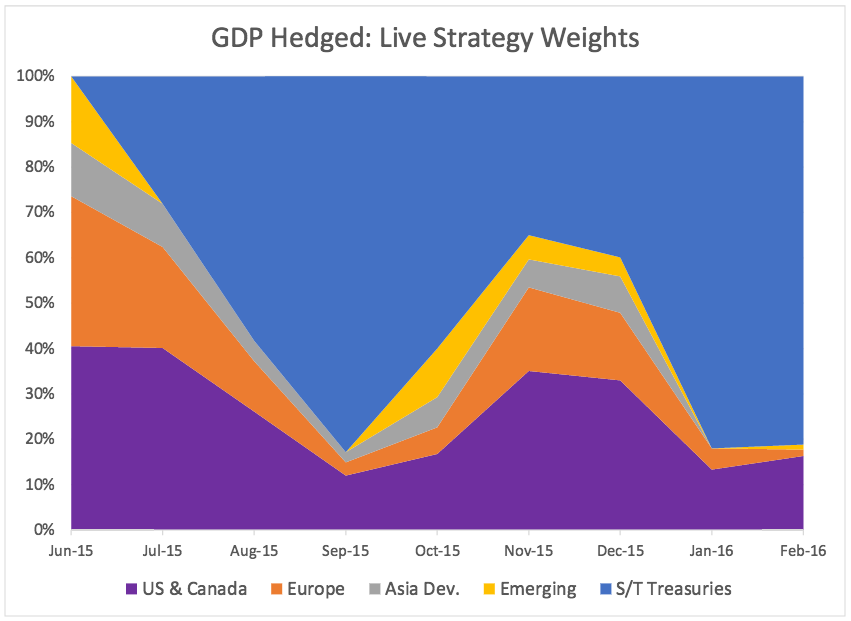

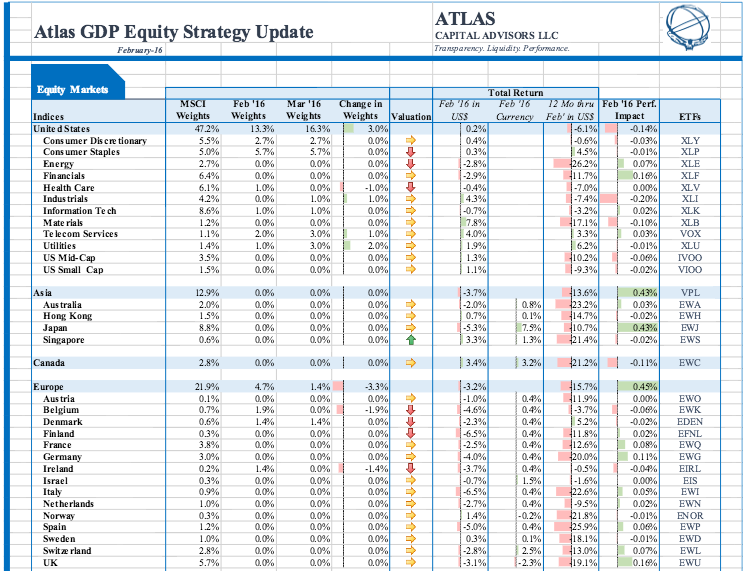

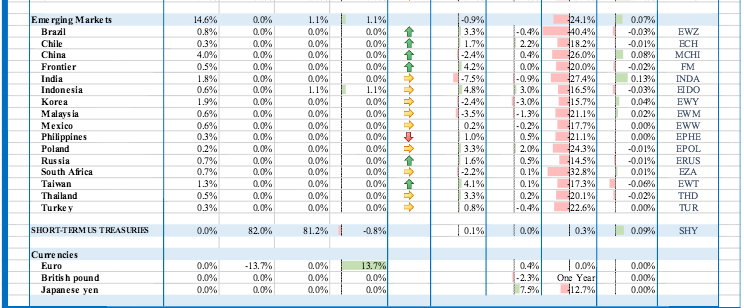

Last month’s rebalance Exhibit C shows the geographic weights of the currency-hedged GDP strategy by month.

The strategy drops out of markets which have negative sentiment as indicated by price behavior.

At the end of February there were few markets with positive enough characteristics for us to hold them in the strategy.

As of the February rebalance, equity holdings in GDP are 19% of assets, about the same as a month earlier.

Our holdings encompass just eight of the 48 markets we track (six US sectors, plus Denmark and Indonesia).

What’s Next?

The GDP strategy does not rely on us being market pundits. However, at this point we remain comfortable with our low weight to equity holdings.

The recent equity market rebound has coincided with a recovery in oil prices. We have doubts about the sustainability of that rebound, given that the world is running out of places to store the excess oil being produced.

We also think the challenges in the high-yield debt market have a ways to go before we hit bottom.

Key Variable

Given that we are now mostly in fixed income, the next stage of relative performance will depend on whether stock markets carry on falling or rebound (as they have so far in March).

The next two tables shows our assessment of which equity markets are attractively priced (the ones with a green arrow pointing up in the “Valuation” column).

Monitoring Markets

We do not currently own positions in any of these markets because of current sentiment.

You can see from the Total Return columns that all of these markets have quite negative returns for the past year, but some of them had modestly positive returns in February.

We are monitoring these markets carefully and will go in with an overweight once we are comfortable that sentiment has shifted.

This discipline, of waiting for price confirmation before moving into markets that appear to have attractive valuation characteristics, is one of the most important design principles in the strategy.

Summary

The most challenging periods for the performance of the GDP strategy are when there are large zigzags in price action, such as have occurred since we launched in mid 2015.

We are pleased with how the strategy has continued to adapt to these rapidly changing market conditions and are confident that GDP is dynamic enough to respond effectively to future market developments.

Photo Credit: Jose’ Moutinho via Flickr Creative Commons