By:

Dane Smith, Head of North American Investment Strategy and Research

Chris Carpentier, CFA, FRM, Senior Investment Strategist

Markets brush off Moody’s US debt downgrade, signaling resilience. But rising rates and fiscal strain still pose long-term risks for investors.

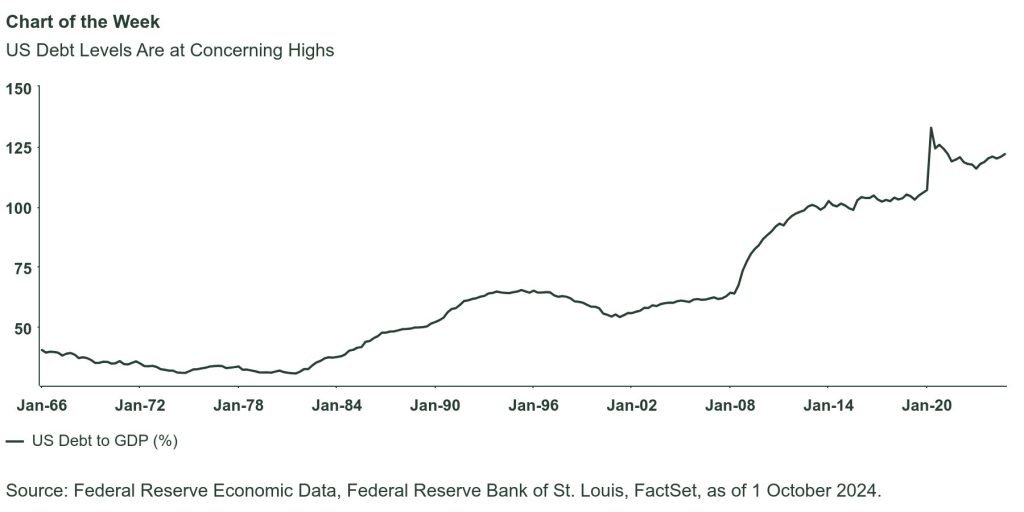

US debt levels have risen to concerning heights, prompting increased scrutiny from economists and policymakers. Despite widespread political awareness of the issue, current indications suggest that government spending will be maintained or even slightly increased, rather than curtailed. Although the United States continues to hold a high-quality debt rating, the growing debt burden may lead to higher risk premia, ultimately increasing the cost of borrowing.

Markets Shrug Off a Well-telegraphed US Debt Downgrade

Last week, Moody’s downgraded US debt from AAA to Aa1. This move, while significant, was generally already expected and not much of a surprise. Other ratings agencies had made similar adjustments in the past; S&P downgraded US debt back in 2011, and Fitch followed suit more recently in 2023. Despite the downgrade, the market reacted calmly. The 10-year yield barely moved, and the S&P 500 index saw a slight increase of 0.09% on the first trading day after the news.

The market’s muted response suggests that investors had already priced in the downgrade. However, this event continues to highlight concerns about elevated debt levels and their potential implications on the appropriate term premia across the yield curve. As illustrated in the Chart of the Week, US debt levels remain high, hovering around 120% of GDP. This is a stark reminder of the fiscal challenges facing the country.

One major difference between now and the 2010s is higher interest rates. The cost of financing this debt is increasing, adding another layer of complexity to the fiscal landscape. While the new spending bill is still being finalized, early indications suggest that reducing the debt load is not a priority, and debt levels are expected to remain high.

The upward pressure on yields has significant implications for asset allocators over the long term. Higher yields make bonds more attractive compared to equities, potentially shifting the balance in investment portfolios. Higher yields also mean higher costs for financing corporate operations, which pressures corporate earnings and acts as a headwind for both equities and corporate credit spreads.

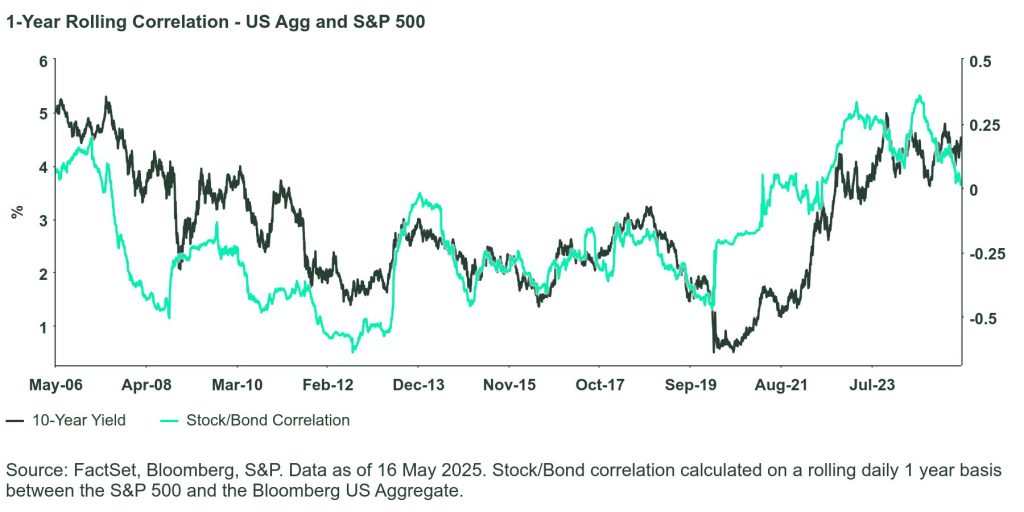

Moreover, the concurrent price behavior of equities and bonds, which have exhibited a negative correlation over the past 20 years, tends to break down at higher yield levels. This negative correlation is a cornerstone of many asset allocation strategies, particularly during times of market volatility. If interest rates remain high, the reliability of this negative stock/bond correlation diminishes, making the role of other diversifiers even more critical.

Overall, we continue to believe that interest rates will be lower over the medium to long term. However, we do not dismiss the impacts of heavy debt loads and continued fiscal deficits. These factors will undoubtedly play a role in shaping the economic landscape and influencing investment decisions.

While the market has taken the recent downgrade in stride, it serves as a reminder of the ongoing fiscal challenges and the potential implications for investors. Elevated debt levels, higher interest rates, and the evolving dynamics between equities and bonds are all factors that need to be carefully considered in the context of long-term investment strategies.

Originally posted on May 26, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/Wlliam+Potter

VIA SHUTTERSTOCK

DISCLOSURES

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of Dane Smith and Christopher Carpentier through the period ended May 22, 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

Investing involves risk including the risk of loss of principal. Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent. All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Currency Risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.

{kind=link}