By: Christopher Gannatti, CFA, Global Head of Research

Key Takeaways

- In 2024, central banks bought over 1,000 metric tons of gold, for the third year in a row, signaling a strategic shift amid rising geopolitical and currency risks.

- A spirited policy debate spurred on by President Trump regarding the interest rate policy of the U.S. Federal Reserve has been driving investors toward gold in April 2025.

- Demand from tech, driven by AI-related semiconductor needs, combined with resilient jewelry consumption in India and China, underscores gold’s multi-dimensional relevance in a volatile global environment.

There’s a tectonic shift unfolding in global finance—subtle in appearance, but profound in implication. The traditional signposts of market anxiety—stocks, bonds, even crypto—are being bypassed in favor of something far older: gold. The real question in 2025 isn’t just why gold is rising. It’s who is doing the buying—and what that tells us about the future of capital flows, monetary governance and geopolitical trust.

Gold has more than rallied—it has broken records, both nominal and real, surpassing its 1980 inflation-adjusted peak to breach $3,400 and then $3,500 per ounce.1 But this isn’t a speculative frenzy. It’s a quiet reallocation by institutions with long memories and deep pockets: Chinese sovereign funds shifting out of U.S. private equity, central banks responding to fears about the independence of the Federal Reserve and European investors buying physical bars over Easter weekend.2 Gold is now more than just a hedge; it is becoming a consensus signal—a barometer for systemic concern and strategic repositioning.

Central Banks: Already Focused on Gold Prior to April 2025

In 2024, central banks bought over 1,000 metric tons of gold—for the third year in a row.3 This is not normal. For decades, central banks were net sellers of gold. Now they’re stockpiling it again.4 Why?

Take Poland. It led the charge, adding nearly 90 metric tons to its reserves.5 China followed closely, with the People’s Bank of China reporting its fourth straight month of buying gold, leading to reserves valued at $208.64 billion at the end of February 2025.6 These are not cosmetic moves—they’re statements. In a world of rising geopolitical risk and currency weaponization, gold is one of the few assets that travels well across borders and regimes.

ETFs and Investors: The Quiet Comeback

But this isn’t just about state actors. After a muted 2022–2023 period, investors are coming back to gold, too—especially through ETFs.

In the second half of 2024, global gold ETFs flipped from outflows to inflows, driving a 25% year-on-year increase in overall investment demand.7 This was not a speculative move—it was a rotation. As real yields peaked and equity market leadership narrowed, investors started looking for ballast.

And it’s not just the institutions. Bar and coin demand quietly bought over 1,180 metric tons worth in 2024, roughly in line with 2023’s levels.8

That dynamic has only accelerated in early 2025. Gold’s historic surge past $3,500 came not during a crisis, but amid a breakdown in political consensus about the independence of the Fed.9 The implications of Trump’s attacks on Fed Chair Jay Powell and the resulting market fallout have only intensified the search for non-sovereign, non-yielding stores of value.

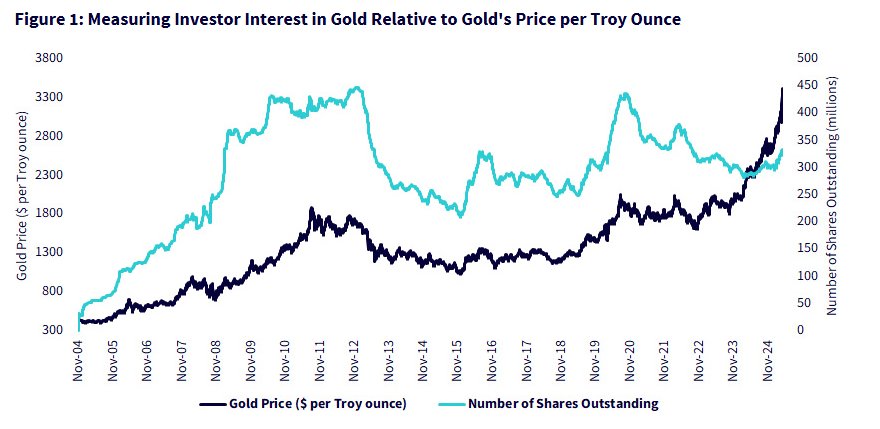

Investors are also measuring the shares outstanding of the largest ETF tracking the price of gold10 and comparing that to the movement in the gold price. Gold’s price has been making new record highs in April 2025, but so far there were far more shares outstanding on the largest gold ETF in 2020, around the time of the pandemic. The implication is that investor interest in gold, at least among ETF market participants, could significantly increase from here. When gold’s price was rising in late 2010 and again in 2020, it was clear that the number of shares outstanding did have a positive relationship with these price moves.

The Unexpected Buyer: Technology

Then there’s the surprise guest at the table: tech.

Gold demand from the technology sector grew 7% last year, reaching 326 metric tons.11 AI, ironically, is driving part of that. High-performance semiconductors and processors require high-conductivity materials like gold for reliability. The more advanced the chip, the more likely it’s plated with the yellow metal.

It’s a fascinating loop: the same future-facing technologies disrupting markets are also reinforcing demand for one of the oldest monetary assets in history.

Jewelry: Still Standing, Even at $3,000+ per Troy Ounce

Even with prices hovering near all-time highs, gold jewelry demand has remained surprisingly strong—especially in markets like India and China, where gold ownership is still as much cultural as it is financial.

Yes, demand dipped 11% from 2023 levels due to higher prices, but consumption hit 1,877 metric tons in 2024.12 When a millennia-old form of wealth preservation meets modern consumer aspiration, demand doesn’t just disappear, it adapts.

The Takeaway: When Everyone Wants the Same Thing

When central banks, hedge funds, retail investors, tech manufacturers and consumers in countries such as India are all buying the same thing—it’s worth paying attention.

Gold is not just an inflation hedge. It’s not just a geopolitical hedge. It’s not just a store of value. It’s all of these things, and its relevance grows in direct proportion to our collective uncertainty.

If the story of 2024 was trust being tested—in currencies, in policy, in the durability of tech rallies—then the story of gold is about people and institutions recalibrating what it means to be safe.

And as 2025 unfolds, the list of gold buyers may be the most interesting sentiment indicator of all.

Originally posted on April 24, 2025 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/dajingjing

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES:

1 Source: James Steel, “Precious Metals Daily: Gold at New Highs on USD Fall; Looks Overextended but No Sign of Imminent Pullback,” HSBC Global Research, 4/21/25.

2 Source: Alim et al., “Gold Hits $3,500 for First Time as Donald Trump’s Attack on Jay Powell Rattles Markets,” Financial Times, 4/22/25.

3 Source: World Gold Council, headline written 2/5/25.

4 Source: https://www.visualcapitalist.com/charted-30-years-of-central-bank-gold-demand/

5 Source: Joseph Hoppe, “Gold Demand Rose to Fresh High in 2024, Report Says,” Wall Street Journal, 2/5/25.

6 Source: Zhang et al., “China’s Central Bank Ups Gold Reserves for Fourth Straight Month in February,” Reuters, 3/7/25.

7 Source: “Gold Demand Rose to Fresh High in 2024, Report Says,” Morningstar, 2/5/25.

8 Source: https://www.gold.org/news-and-events/press-releases/global-gold-demand-hits-new-high-prices-soar-2024

9 Source: Alim et al., 4/22/25.

10 Source: Refers to SPDR Gold Shares (ticker GLD), which had more than $93.4 billion in assets under management as of 3/31/25.

11 Source: Hoppe, 2/5/25.

12 Source: https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2024

DISCLOSURES:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}