By: Christopher N Laine, John G Siegrist and Timothy J Herlihy CFA

What do the first days of the Trump Administration tell us about emerging markets? From tariffs to AI, here are five possible scenarios we’re following.

Emerging market (EM) investors had been in fear mode since it became clear that Donald Trump would win reelection, as trade and tariffs had been a significant theme of his campaign. Indeed, going back to the 1980s, he often advocated for tariffs and more competitive USD exchange rates as ways to improve the US trade imbalance. As a result, markets have been expecting a significant salvo on the trade front – and we have seen the start of this as we enter February 2025. EM equity investors have been in a defensive posture (major outflows in EM equity funds in November and December 2024) – and it is fair to say they remain in a “wait and watch” mood on what we’re calling “wildcards.”

Wildcard #1: Trade Policy

The new US administration initially focused its efforts on domestic policy or areas with a clear domestic political focus. Tariffs were threatened, and eventually became explicit US policy. How these are resolved, retaliated, raised, or relinquished will be the major effect on EM economies and markets.

Tariffs will be a mainstay of US policy. Therefore, trade policy towards emerging markets is likely to be an overhang of idiosyncratic risk. Who ends up as the target will depend on specific circumstances and negotiation, especially if a secondary policy objective is at stake.

We expect that there will be two groups of countries: those that can/will do deals, and those countries that the administration will look to contain. China is clearly in the latter category, unless the president’s close economic advisors manage to convince him that a trade deal is more of a win than a tit-for-tat trade war. This would be unexpected by the market and very positive for EM sentiment. This should not be considered a ‘base-case,’ but an opportunity to buy the asset class.

India represents a country that is likely to be more in the ‘deal’ category. The country’s unique status, given its geopolitical importance, means the new administration may tread carefully. Interestingly, India has just cut tariffs on US goods (albeit from a relatively high level). This sort of news flow will clearly be pleasing to the new administration and may well be copied by certain markets, signaling a deal is preferred.

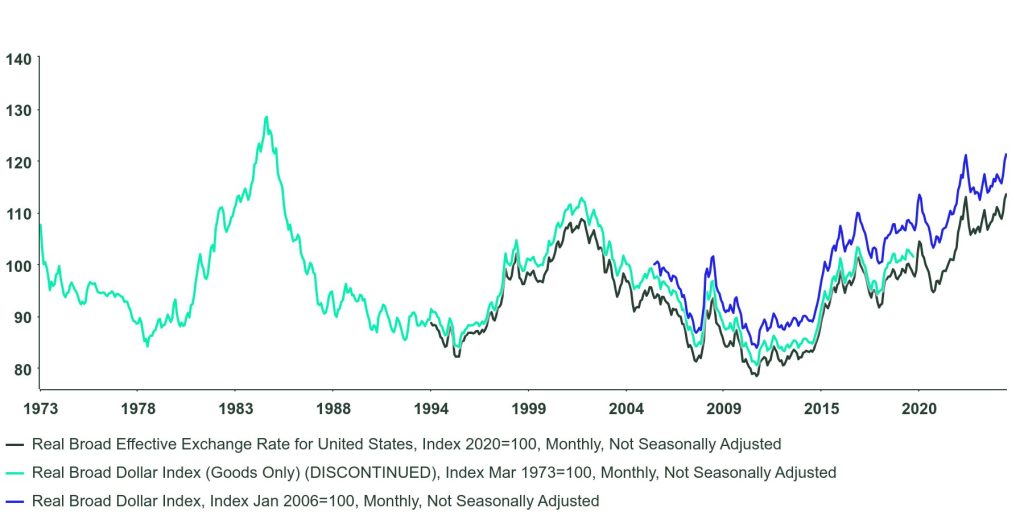

Wildcard #2: The Ol’ Greenback

President Trump has been very clear about his distaste for large US trade deficits and has repeatedly stated his preference for a weaker US dollar to increase the competitiveness of US products. Now, against the backdrop of an extremely strong dollar – by the way, we are getting awfully close to record high in the modern era – a strong USD keeps inflation lower and keeps the US in the good graces of global investors. These effects will be helpful for the new administration, but we cannot see that they will want the strength of the dollar to further increase. This may well mesh with their desire for lower US interest rates.

A gentle, orderly fall in the US dollar would indicate that the world economy is on a more even-keeled growth trajectory; it would help with the US imbalances and improve liquidity in economies outside the US. A modestly lower path for the dollar would be very beneficial to emerging market equities and perhaps help the administration’s stated goals.

Wildcard #3: China Policy Stimulus

What if the Chinese government really gets serious about delivering strong reform packages? After trying almost everything else, there was a hint of a real movement in the fall of 2024, when the government announced a series of measures that caught the market off guard. It didn’t last as investors soured on specifics, but the shift in focus of the authorities is clearly evident. The problem is clearly known (and has been carefully studied), but the solution has been a bit more elusive. Nonetheless, the attention and direction suggests there is a chance that sufficient measures may finally get taken – as each new set of measures indicates. As we saw in September 2024, the moves could be fast and furious. The short-China trade is ‘long in the tooth’ by conventional standards.

Wildcard #4: Return of the Bond Vigilantes – or the US Version of the ‘Liz Truss’ Trade

The US fiscal situation is in ‘yellow-light’ territory with high levels of US debt to GDP and very high levels of interest service as a percentage of US federal outlays. The new administration has made significant promises on tax cuts, but has been less clear on how these would be paid for. This is, of course, not news and all administrations will be faced with real policy choices when it comes time to govern. However, if the tax cut policy gets momentum, bond investors may look to apply some market discipline with higher rates. The uglier scenario would be if we saw higher rates, coupled with a shaky dollar. Again, this is not a baseline view, but one that increases (regardless of administration) over time. The US debt-to-GDP ratio in 1980 when President Reagan began his tax cutting agenda was 31%.1 We are a long way from that now at 123%.

Wildcard #5: The Future of AI Spend

The AI supply chain story has been a source of optimism in the EM universe over the last two years, with those stocks being clear beneficiaries of a one-way AI capex race. However, the news that Chinese startup DeepSeek was able to replicate the performance of US Large Language Models (LLMs) at a fraction of the cost sent reverberations across global markets in late January. Does this news mark the peak of the boom for AI supply chain stocks in South Korea and Taiwan?

The key challenge for AI suppliers in Taiwan and China is that the DeepSeek news, in unison with some of the macro uncertainties discussed above, will lead companies to question the unprecedented amounts being spent on computing power. While this would represent a headwind for semiconductor manufacturers, it could lead to growth in other pockets of EM as software and IT service providers in India and China see more immediate benefits from the AI theme.

A more optimistic outlook for the sector is that, rather than representing a paradigm shift, the DeepSeek news is another enhancement along a continuum of AI optimization gains and cost reductions – similar to the Meta’s decision in 2023 to share the code that drove its AI technology, Llama. It may even be the case that more efficient model training brought on by DeepSeek increases training demand, and capex expenditures continue to increase.

The Bottom Line: Macro Matters – But Macro Positioning is Only for the Brave

Our work continues to suggest that stock selection remains the key source of alpha generation in emerging markets. Macro headwinds will be volatile in 2025, but will likely be idiosyncratic and fast moving. We are not in the business of chasing headlines and see too much risk in taking large macro bets. We continue to recommend that investors stay diversified and look to take advantage of macro dislocations, only to add to broad stock positions when values arise. Turn your TV and social media off, please. You will be better off sticking with broad fundamentals – value, quality, and sentiment.

Originally posted on February 7, 2025 on SSGA blog

PHOTO CREDIT : https://www.shutterstock.com/g/Aroma_Art

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES:

DISCLOSURES:

Marketing Communication

ssga.com

State Street Global Advisors Worldwide Entities

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

The views expressed in this material are the views of Christopher Laine, Jay Siegrist, and Timothy Herlihy through February 4, 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Past performance is not a reliable indicator of future performance.

Investing involves risk including the risk of loss of principal.

Investing in foreign domiciled securities may involve risk of capital loss from unfavorable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations.

Investments in emerging or developing markets may be more volatile and less liquid than investing in developed markets and may involve exposure to economic structures that are generally less diverse and mature and to political systems which have less stability than those of more developed countries.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

For EMEA Distribution: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication. Investments in small-sized companies may involve greater risks than in those of larger, better known companies.

Companies with large market capitalizations go in and out of favor based on market and economic conditions. Larger companies tend to be less volatile than companies with smaller market capitalizations. In exchange for this potentially lower risk, the value of the security may not rise as much as companies with smaller market capitalizations.

The market values of growth stocks may be more volatile than other types of investments. The prices of growth stocks tend to reflect future expectations, and when those expectations change or are not met, share prices generally fall. The returns on “growth” securities may or may not move in tandem with the returns on other styles of investing or the overall stock market.

Actively managed funds do not seek to replicate the performance of a specified index.

The Strategy is actively managed and may underperform its benchmarks. An investment in the strategy is not appropriate for all investors and is not intended to be a complete investment program. Investing in the strategy involves risks, including the risk that investors may receive little or no return on the investment or that investors may lose part or even all of the investment.

This document provides summary information regarding the Strategy. This document should be read in conjunction with the Strategy’s Disclosure Document, which is available from SSGA. The Strategy Disclosure Document contains important information about the Strategy, including a description of a number of risks.

Diversification does not ensure a profit or guarantee against loss.