Recent shocks in global macro policy and politics have caused substantial moves in equity markets, only for the effects to shortly thereafter simmer down and reverse rapidly. We drill down into two of the most recent episodes and consider what this may mean as we head into the future.

Japan’s Roller Coaster

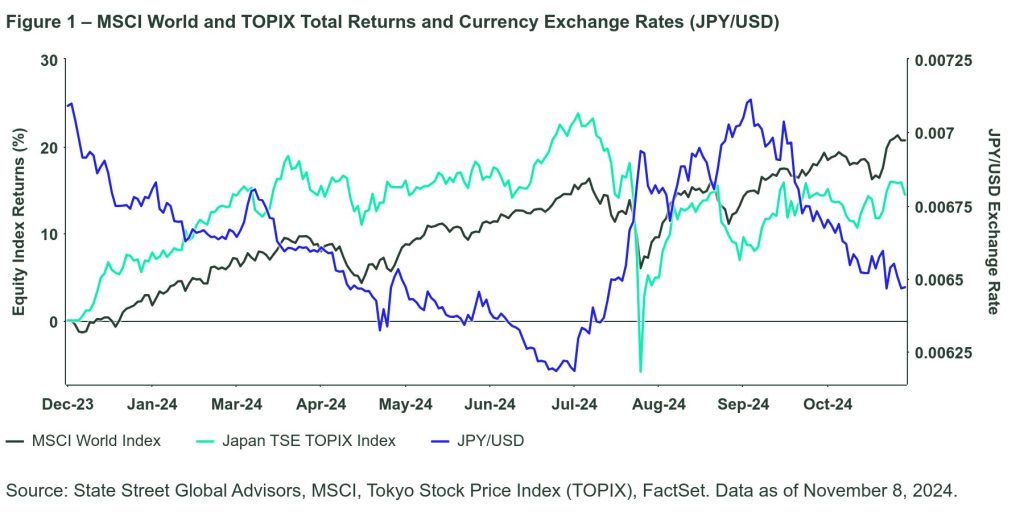

In late July and early August 2024, the Japanese equity market hit unexpected turbulence. While we don’t generally favor ex-post rationalization of market moves, the prevailing narrative starts with the Bank of Japan raising its benchmark interest rate from 0.1% to 0.25% on July 31. A subsequent weak jobs report in the US increased speculation around the Federal Reserve cutting its interest rate sooner, and by more than expected. The resulting shift in interest rate differentials led to a rapid unwind of the hugely popular yen carry trade (borrow in yen and buy higher yielding currencies such as the US dollar, Australian dollar or Mexican peso, depending on one’s risk appetite). These changes in the currency markets and interest rates quickly found their way into the stock market and Japanese shares plummeted.

The price action in Japanese equities and currency was substantial. On August 5, the Tokyo Stock Price Index (TOPIX) tumbled by 12% (Figure 1). The ripple effects globally were much lighter with the MSCI World Index only falling by 3%. Just over a week later, however, both Japanese and World equity indices had completely recovered from the early August routing.

China’s Reverse Course

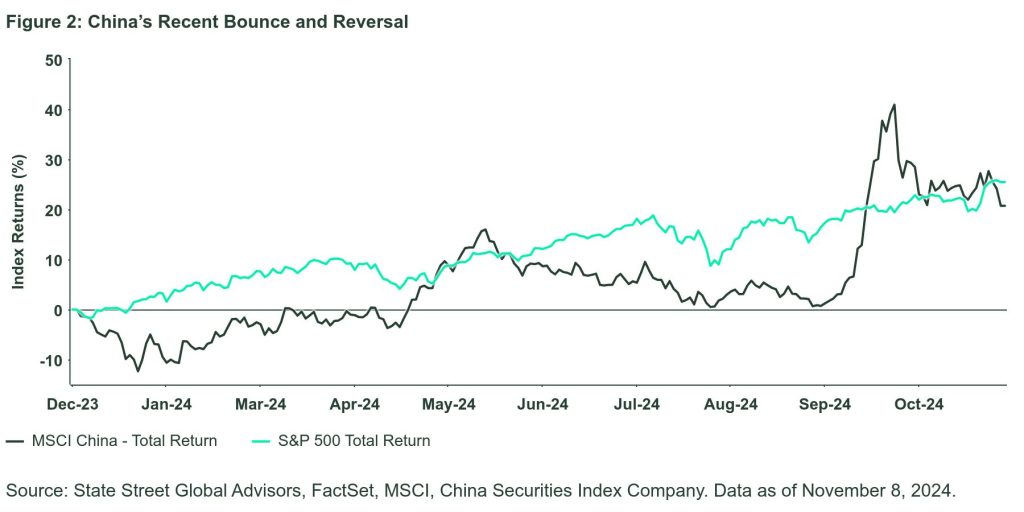

Over the past few years, the Chinese equity market has significantly lagged its counterparts across both developed and emerging markets as we have written about in a previous commentary (refer to Ripples From China). Stimulus measures announced at the end of September resulted in a sizable re-rating of the Chinese equity markets, soon followed by a subsequent dip in early October (Figure 2).

In the aftermath of the knee-jerk reaction, markets started to digest the economic impact of the announced stimulus measures and saw equity markets reverse. A further set of measures publicized in November, which still fail to address issues such as the state’s high debt levels, problems in the real estate sector, and weak domestic demand, were also unenthusiastically welcomed. Further market weakness ensued.

Shocks as Drivers of Momentum and Volatility Returns

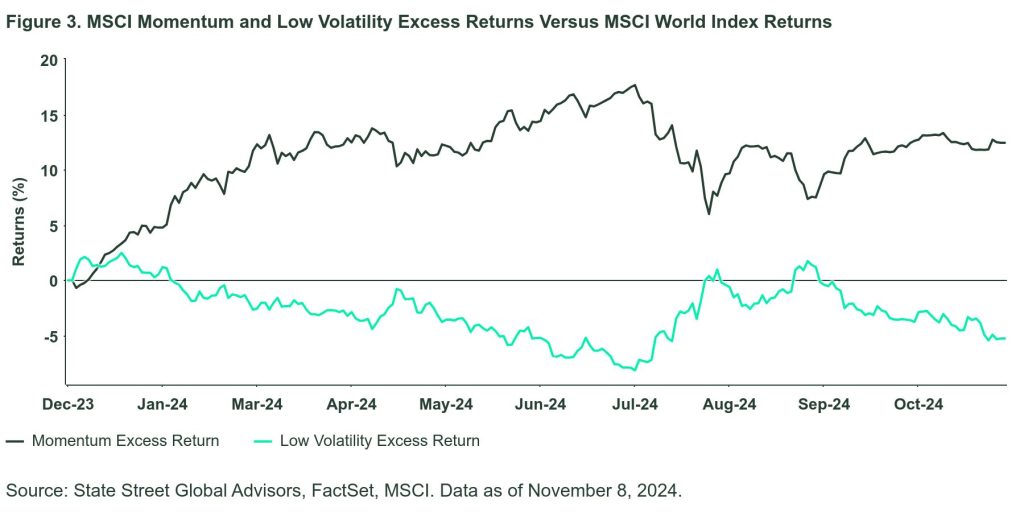

At a factor level, Momentum has been one of the strongest performers through the course of 2024. Lower risk stocks have underperformed this year, apart from a brief rally over the course of the summer months.

Although Momentum is often thought to reverse at turning points, or in times of market shock, the data shows that its low point since the year-to-date high of July 11 was on August 5 (Figure 3). This similarly coincides with the best of the returns from low volatility stocks versus high volatility. That particular market event served merely to disrupt what looked like a newly establishing trend, and reverted back to its prior themes.

In contrast to the Japan events mentioned above, the Chinese stimulus event barely caused a ruffle in the path of Momentum or Volatility.

The Bottom Line

Over the past few months we have started to see a pickup in volatility in equity markets. This volatility is associated with idiosyncratic events as noted above, as well as the unknowns leading to the US elections. Equities in aggregate remain expensive compared to their history. With valuations at lofty levels and uncertainty persistent as global economies look for a landing, we believe that volatility is here to stay.

The outcome of the US election has been one of the largest uncertainties of late. The equity market reaction to the recent US election has been stark. In the first six days since the election outcomes have been known, the US equity market is up 4%. In contrast, Europe is down by 2% and emerging markets (EM) have fallen by 3%. This EM dip is led by an almost 5% decline in China, a nation which faces the headlights of trade wars and tariffs.

Predicting outcomes from politics, policy or elections is a challenging exercise. Critically, we do not try to forecast these events within our investment process. Predicting the reaction to these outcomes may be even harder as the dust settles from an initial knee-jerk reaction to events.

Ultimately, we wait to see the longer-term effect on fundamentals for companies, rather than focus on the immediate surge in US stocks after the election. We favor setting our course over a longer horizon, taking account of both risk and return in our investment process and refraining from overreactions to short-term noise.

Originally posted on November 27, 2024 on SSGA blog

PHOTO CREDIT : https://www.shutterstock.com/g/Hlop4ik

VIA SHUTTERSTOCK

DISCLOSURES:

For use in EMEA: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons, and persons of any other description (including retail clients) should not rely on this communication.

Important Risk Information

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

The views expressed are the views of Systematic Equity – Active through October 17, 2024, and are subject to change based on market and other conditions.

Quantitative investing assumes that future performance of a security relative to other securities may be predicted based on historical economic and financial factors, however, any errors in a model used might not be detected until the fund has sustained a loss or reduced performance related to such errors.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

{kind=link}

{kind=link}