By: Kevin Flanagan, Head of Fixed Income Strategy

Key Takeaways

- Inflation has shown notable improvement from its 2022 peak readings, but the road ahead may not be easy.

- Both Core CPI and Core PCE inflation readings reversed course in 2023, but the pace of improvement has slowed down in the last two to three months.

- There could be some daylight emerging between Fed policy makers regarding the timing and extent of rate cuts, with Fed Chairman Powell less deterred by recent inflation readings and Governor Waller suggesting a reduction in the overall number of rate cuts or pushing them further into the future.

Even though I have never come anywhere close to running a marathon of any sort, I am told the last mile could be the most difficult part of the endeavor. Looking at how inflation has performed to begin 2024, it appears the improvement investors have witnessed over the first 25 miles of this marathon could have been the easy part, and the road to mile number 26 may be harder.

The money and bond markets may have gotten a little complacent on inflation trends after the 2023 experience. Indeed, the peak readings of 2022 for both headline and core inflation were put in the rearview mirror rather quickly, as price pressures cooled off on an almost monthly basis. Given the rally in the Treasury market that was witnessed in Q4 of last year, there is little doubt that this type of improvement was expected to continue, perhaps leading to the Federal Reserve achieving their 2% threshold in the process.

Core Inflation

For this blog post, I am going to focus solely on inflation minus food and energy, using two different gauges: the Consumer Price Index (CPI) and the Personal Consumption Expenditures Price Index (PCE). Interestingly, one could argue the markets focus more on the CPI gauge, while the Fed uses the PCE measure for its official inflation target.

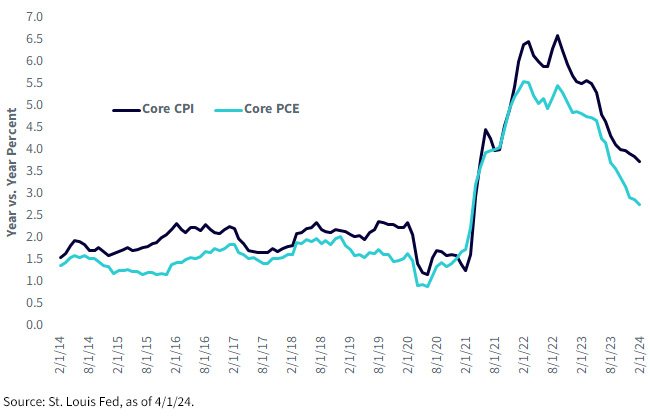

As you can see, both core inflation readings reversed course in 2023, but the degree of improvement has leveled off somewhat. Core CPI and PCE each hit their peak year-over-year gains of 6.6% and 5.5%, respectively, in September 2022 and dropped to roughly 4% and 3% toward the end of last year. However, the pace of improvement has become a bit more grudging over the last two to three months, with Core CPI coming in at 3.8% and Core PCE at 2.8% in February, the latest data available.

Given this backdrop, what’s a central banker to do? Looking at recent comments from Fed Chairman Powell and Governor Waller, one gets the consistent message that the voting members are not in a hurry to cut rates, but that rate cuts will more than likely occur this year. However, there seems to be some daylight between these two policy makers’ views on when and by how much. While Powell doesn’t seem to be overly deterred by the recent inflation readings, Waller did say the data is leading him to believe that “it is appropriate to reduce the overall number of rate cuts or push them further into the future.”

Powell has also recently mentioned that perhaps inflation doesn’t need to get down precisely to the Fed’s 2% target. Does that mean that Core PCE at 2.5% would be viewed as an acceptable point to begin cutting rates? If you look at the history of Core CPI and Core PCE, there is usually a spread between their year-over-year readings, with the post-COVID period of December 2020–December 2021 being the only exception over the last 10 years. If this spread holds, would the Fed feel comfortable lowering rates if Core CPI was somewhere between 3% and 3.5%?

Conclusion

While the Fed may look to begin easing in such a scenario, the U.S. Treasury 10-year note may not be that thrilled, especially if the labor market data remains resilient and solid.

PHOTO CREDIT :https://www.shutterstock.com/g/rozbyshaka

Via SHUTTERSTOCK

Originally Posted April 3rd 2024, on WisdomTree’ blog

Disclosure:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.