By: Jose Torres, Interactive Brokers’ Senior Economist

The Santa Rally is showing no signs of fatigue as we approach the last week of January, with market bulls cheering Netflix’s surprise increase in subscribers. Despite an ongoing series of hotter-than-expected economic data, the rally is resilient, supported by relaxed financial conditions driving economic activity. This morning’s S&P Global Purchasing Managers’ Index (PMI) exceeded forecasts, but tomorrow’s GDP report and Friday’s PCE Inflation print are likely to be more impactful upon investor sentiment. However, against this backdrop, market participants are expecting the first Fed cut to arrive in May rather than March, with robust data serving to extend the journey across the monetary policy bridge.

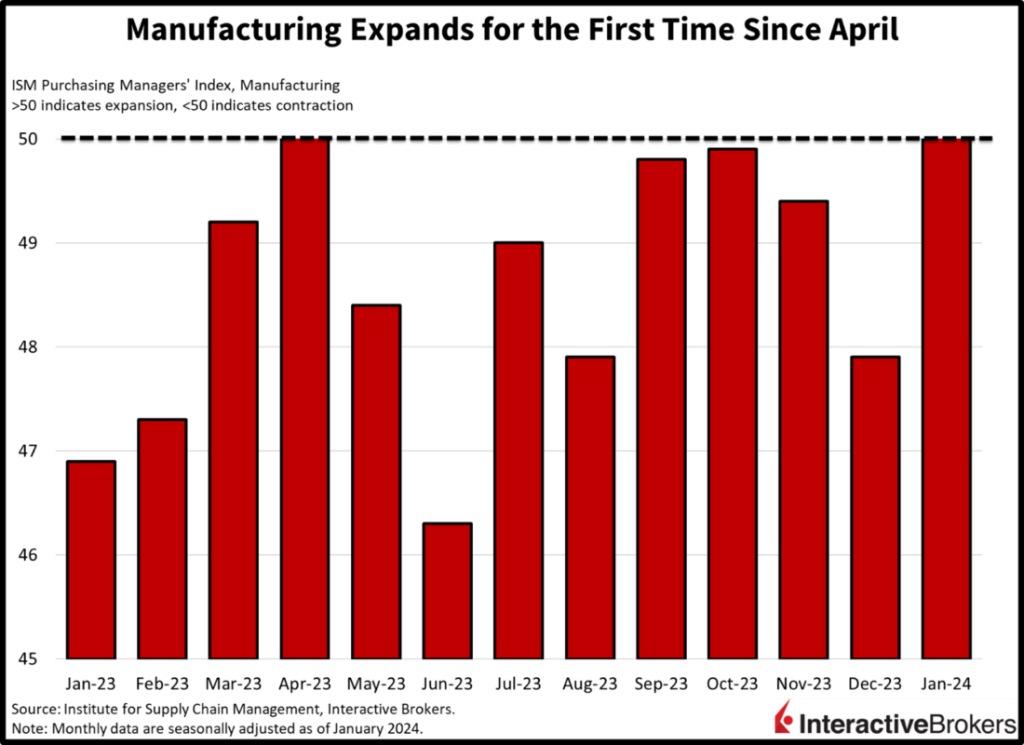

Manufacturing Expands for The First Time in a While

Today’s PMI reflected strong surprises, with manufacturing notably shifting from contraction into expansion. Business confidence was a key driver, propelling the positive change as retailers briskly increased inventories in anticipation of improved future performance. Additionally, input costs rose at the fastest pace since last April. These factors pushed the Manufacturing PMI to 50.3 this month, shattering expectations for an unchanged level of 47.9. The expansion marks the first month of growth in nine. However, weak demand and transportation delays from adverse weather and geopolitical conflicts weighed on performance. Employment also capped the headline figure, with goods producers marginally trimming headcounts.

Services Sectors Remain Robust

The services sector also surprised to the upside, growing at a faster pace than December. The Services PMI of 52.9 exceeded the 51 projected and December’s 51.4. An uptick in customer traffic, which increased at the fastest pace since June, was the primary driver of the increase. Employment growth did slow down, however, as companies increasingly focus on efficiencies while only increasing prices marginally. These measures seek to boost worker productivity, maintain competitiveness and preserve margins. Similar to manufacturing, confidence also rose sharply, driven by expectations of potential Fed rate cuts boosting business prospects.

Europe is in Recession

Across the Atlantic, European PMIs continued to indicate recessionary conditions with both manufacturing and services continuing to contract. The manufacturing sector contracted at a slower speed this month while services declined slightly faster as the segments reported levels of 46.6 and 48.4, respectively, versus 44.8 and 48.8 for December. Geopolitical conflicts weighed on Europe more than the US, with the Suez Canal turmoil significantly impairing supply chain conditions and intensifying price pressures. In fact, the rate of inflation jumped to its hastiest clip since May. New orders also weighed on headline figures, while employment and business confidence offset some of the weakness. The region’s largest economies, Germany and France, didn’t provide much optimism, however, with both nations experiencing sharp deteriorations in economic conditions.

Netflix Surprises but Texas Instruments Warns

Lower cost streaming entertainment options are gaining traction while in other areas of the economy, demand for natural gas is surging while semiconductor manufacturers are experiencing revenue weakness.

- Netflix reported a strong quarter with advertising-supported subscriptions driving a surge in new customers and earnings jumping significantly from the year-ago quarter. The company generated an earnings per share (EPS) of $2.11, which missed the analyst consensus estimate of $2.20 but nevertheless climbed significantly from $0.12 in the year-ago quarter. Its revenue of $8.83 billion, furthermore, climbed from $7.85 billion year-over-year (y/y) and beat the analyst consensus of $8.7 billion. Netflix has been cracking down on subscribers sharing their passwords and has offered shared account options and advertising-supported accounts. Those efforts contributed to the company adding 13 million subscribers, exceeding the analyst expectation of 8.7 million and bringing its total subscriber count to 260.8 million. Analysts anticipated 256 million accounts. In the fourth quarter, the ad-supported offering accounted for 40% of its new subscribers and grew 70%. Netflix also said it will phase out its lowest-fee advertising offering that has no advertising in Canada and the UK. Netflix also said future improvements to its offering may lead to it increasing its subscription fees and it anticipates generating a current-quarter EPS of $4.49 while analysts had forecast $4.10.

- Texas Instruments, which manufactures semiconductors, reported a decline in revenue and earnings. It also issued a cautious outlook for the current quarter. The company’s wide range of end markets, including industrial, consumer electronics and automobile manufacturers is considered an indicator of chip demand across the broader economy. For the fourth quarter, revenue of $4.08 billion dropped 13% y/y and missed the consensus estimate of $4.13 billion. Its EPS of $1.49 declined from $2.13 in the year-ago quarter but beat the analyst expectation of $1.46. Texas Instruments CEO Haviv Ilan said the company experienced weakness in its industrial and automotive sectors. The company estimates its first quarter revenue will range from $3.45 billion to $3.75 billion while analysts had estimated revenue of $4.06 billion. It estimates a first quarter EPS ranging from $0.96 to $1.16 a share, significantly below the analyst expectation of $1.42.

- Baker Hughes, one of the world’s largest providers of products and services for oil and natural gas production, generated strong fourth-quarter revenue growth that pushed its earnings above the analyst consensus expectation. Activity by US shale producers is slowing, with North America revenues climbing only 1%, but international demand has been growing as foreign energy firms are building liquid natural gas (LNG) facilities. After adjusting for irregular expenses, Baker Hughes produced an EPS of $0.51, exceeding the analyst expectation of $0.47 and increasing from $0.38 y/y. Its revenue of $6.83 billion climbed from $5.90 billion y/y but trailed the consensus estimate of $6.91 billion. Baker Hughes benefited from countries seeking to lower carbon emissions by using natural gas instead of coal. Additionally, geopolitical risks, including Moscow’s invasion of Ukraine, has caused increased demand for new sources of LNG to replace Russia as a provider of the commodity. In the fourth quarter, for example, Baker Hughes secured a $1 billion LNG contract in the United Arab Emirates. Also in the fourth quarter, Baker Hughes trimmed $150 million in costs and continued to streamline operations.

Technology Leads Market Rally

Bullish sentiments continue to dominate equity markets with all major US indices higher on the session. Unsurprisingly technology is leading with the Nasdaq Composite Index up 0.8% while the S&P 500 is up 0.7%. Other leaders include the Russell 2000 and Dow Jones Industrial indices with gains of 0.5% and 0.4%, respectively. Sectoral breadth is split with the defensive health care, utilities and consumer staples sectors lower alongside cyclical real estate and materials. The other six sectors are higher, led by communication services, up 1.2%, and technology and energy, which are both up 1.1%. Energy is benefitting from a sharp increase in crude oil prices, driven by intensifying tensions in the Red Sea, a big draw in US inventories and optimism regarding stimulus from Beijing, the world’s largest importer. WTI crude is up 1.4%, or $1.07, to $75.52 per barrel, its highest level in four weeks. Bond yields are generally higher, with 2- and 10-year Treasuries trading at 4.37% and 4.15%; the former is unchanged while the latter is up 2 basis points (bps). The dollar is weaker as firmer monetary policy expectations out of Tokyo and Frankfurt weigh on the greenback. Specifically, the Bank of Japan is expected to lift its key rate into positive territory while today’s news of the sharpest Euro inflation since May points to a hawkish Lagarde. The greenback is down relative to the euro, pound sterling, franc, yen, yuan and Aussie dollar while it’s up against the Canadian dollar.

Are We Here Again?

Since 2021, an important feature of short-term inflationary cycles is that when the marketplace and Chair Powell dismisses them, they somehow come back. January’s hot US economic reports portraying a robust December raise concerns for the rest of the year. Additionally, January’s PMIs indicate a global acceleration in inflation, driven by relaxed financial conditions and disruptions in the supply chain due to geopolitical factors. These developments have the potential to significantly amplify price pressures considering the Consumer Price Index bottomed at 3% last June. While December’s CPI was 3.4%, the ongoing developments may push the figure closer to 4% in the coming months, derailing plans for monetary policy easing and triggering substantial market re-pricings. If GDP and PCE inflation come in hot tomorrow and Friday, I’m expecting a mean Chair Powell to approach the mound at next week’s Fed meeting. He may even be as tense as at Jackson Hole in August 2022, when his remarks led to a 20% decline in equity markets in only six weeks.

This post first appeared on January 24th, 2024 on the IBKR Traders’ Insight blog

PHOTO CREDIT: https://www.shutterstock.com/g/rozbyshaka

Via SHUTTERSTOCK

Visit Traders’ Academy to Learn More About PMIs and Other Economic Indicators.

DISCLOSURE: INTERACTIVE BROKERS

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}

{kind=link}