By: Jose Torres, Interactive Brokers’ Senior Economist

Markets firmed up this morning following lighter-than-expected home sales data. While real estate and other rate-sensitive sectors of the economy are slowing, Black Friday and Cyber Monday events are providing investors with some optimism regarding consumer spending. Meanwhile, market players are looking for clues against the backdrop of a full week of economic data that wraps up with Powell.

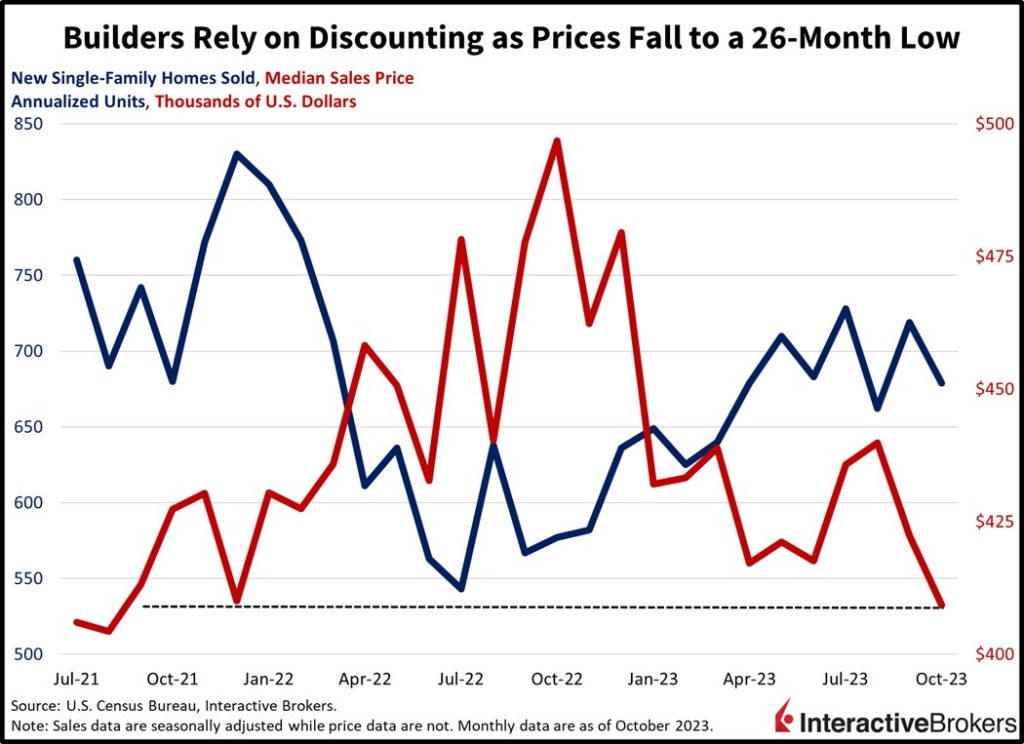

8 Handle Pressures Activity

New home sales weakened in October despite builders offering price discounts and interest rate concessions. Even with those incentives, mortgage rates with an eight handle caused many potential homeowners to be priced out of the market.

October’s seasonally adjusted annualized units (SAAU) of 679,000 missed expectations for 723,000. The pace of transactions declined 5.6% month-over-month (m/m), with September’s figure revised to 759,000 SAAU. On a favorable note, sales in the Northeast and South climbed 13.2% and 2.1% m/m. The West and Midwestern regions performed poorly though, with transactions dropping 23.3% and 16.4%. Furthermore, median and average prices dropped 3.1% and 5.5% m/m. On a year-over-year (y/y) basis, median and average price levels dropped 17.6% and 10.4%.

Markets Strengthen on Weaker Data

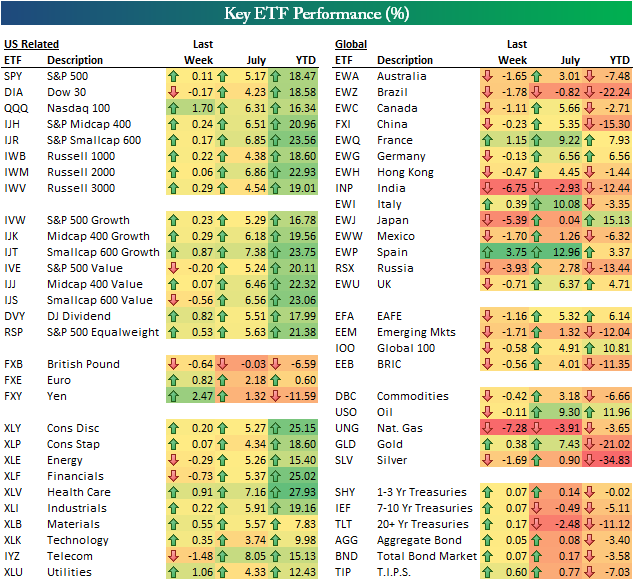

Markets are mixed as investors bought the dip in stocks following this morning’s real estate data, which was released intraday at 10:00 am Eastern Time. Softer data also pushed yields lower simultaneously. Most major U.S. equity indices are lower, however, as the Russell 2000, Dow Jones Industrial and S&P 500 indices drop by 0.4%, 0.1% and 0.1%. The Nasdaq Composite Index is higher though, as market players scoop up shares of Amazon on holiday shopping optimism. The Nasdaq is up 0.1% while Amazon is higher by 1.4%. Beneath the surface though, there’s some evidence that the recent rally has run its course, with cyclicals getting punished due to weaker economic prospects. Sectoral breadth is quite terrible, with all sectors lower minus technology, real estate and consumer discretionary. In fixed-income land, yields on the 2- and 10-year Treasury maturities are down 3 and 4 basis points to 4.93% and 4.43% as investors dial up Fed rate cut expectations. Meanwhile, the dollar is near the flatline as the greenback gains versus its Canadian counterpart, the euro and the yuan. The U.S. currency is higher relative to the yen, franc, pound sterling and Aussie dollar though.

OPEC + Meeting in Focus

Oil prices dropped nearly $1 per barrel this morning after recording their first weekly gain in five weeks. WTI crude has recovered since though, with prices now higher on the session by 0.5% or $0.35 to $75.47 per barrel. After four weeks of declines, oil prices climbed last week on speculation that Riyadh and Moscow would extend production cuts through the early portion of next year and that OPEC + members might strike an agreement to further curtail output. News last week that the cartel had postponed a meeting to November 30 that was intended to determine production levels caused prices to soften. The postponement was attributed to disagreements regarding production quantities for Africa. Unnamed sources, however, say that OPEC + has moved closer to striking an agreement, according to Reuters. Other factors contributing to softening prices include higher-than-expected crude stockpiles in the U.S., reports that Abu Dhabi might increase exports and efforts by Baghdad to resume exports through Ankara. Additionally, the International Energy Agency has reported that supply could outpace demand in 2024.

Holiday Shopping Robust, So Far

Black Friday data doesn’t depict the strength of consumer spending during the entirety of the holiday season, so we will carefully assess more shopping information as it becomes available in the coming days. Additionally, tomorrow’s Consumer Confidence report and Thursday’s Consumer Spending data will provide important insights into the health of Americans’ budgets while Friday’s ISM Manufacturing release, which includes new order and inventory data, will offer a glimpse of retailers’ expectations for consumer spending. Wednesday’s third quarter GDP revision will also provide some details. The week wraps up with incoming data potentially influencing the tone of Federal Reserve Chairman Jerome Powell’s presentation. If he dishes out dovish comments, investors may finish the week by enthusiastically stocking up on equities and bonds. Hopefully, protesters will sit out Powell’s presentation, unlike a recent event during which he told ballroom ushers to shut the door to keep disruptors at bay. While the event may have influenced his mood, Powell refused to close another door—the door on the possibility of additional rate hikes. If he maintains that position, investors who are expecting rate cuts as early as March are likely to be disappointed.

Visit Traders’ Academy to Learn More About New Home Sales and Other Economic Indicators.

This post first appeared on November 27th 2023, IBKR Traders’ Insight Blog

PHOTO CREDIT: https://www.shutterstock.com/g/SeventyFour

Via SHUTTERSTOCK

DISCLOSURE: INTERACTIVE BROKERS

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}