By Alan Meng, SI Research Lead

- Objective Measurement: Investors must objectively measure the fair value of SLBs to avoid overpaying for non-pecuniary features of the bond.

- Establishing Norms: As the SLB market expands, well-established norms at the issuer side and consensus among investors are essential for market efficiency.

- Transparency and Efficiency: More transparent and relevant target settings are crucial for fostering an efficient SLB market with minimal transaction costs.

Sustainability-linked bonds (SLBs) function as a performance-based debt instrument. They allow issuers to raise capital with financial characteristics of the bond (e.g., coupon payments) being tied to predefined sustainability targets. This type of instrument has been woven into the broader landscape of the ‘labeled bond market,’ alongside their counterparts including green, social, and sustainability bonds.

SLBs are any type of fixed income security where the financial and/or structural characteristics depend on whether the issuer achieves agreed Sustainability/ESG objectives. This type of instrument has been woven into the broader landscape of the ‘labeled bond market’, alongside their counterparts including green, social, and sustainability bonds.

Since debuting in 2019, it took less than four years for the SLB market to pass the USD 250 bn cumulative issuance milestone (which took green bonds a decade to accomplish). At present, the outstanding amount of all SLBs exceeds 10% of the size of green bonds and represents 7% of the overall labeled bonds universe. However, as the SLB market is still in its infancy and evolving, it continues to be a subject of debates and scrutiny.”

Since debuting in 2019, it took less than four years for the SLB market to pass the USD 250 bn cumulative issuance milestone (which took green bonds a decade to accomplish). At present, the outstanding amount of all SLBs exceeds 10% of the size of green bonds and represents 7% of the overall labeled bonds universe. However, as the SLB market is still in its infancy and evolving, it continues to be a subject of debates and scrutiny.

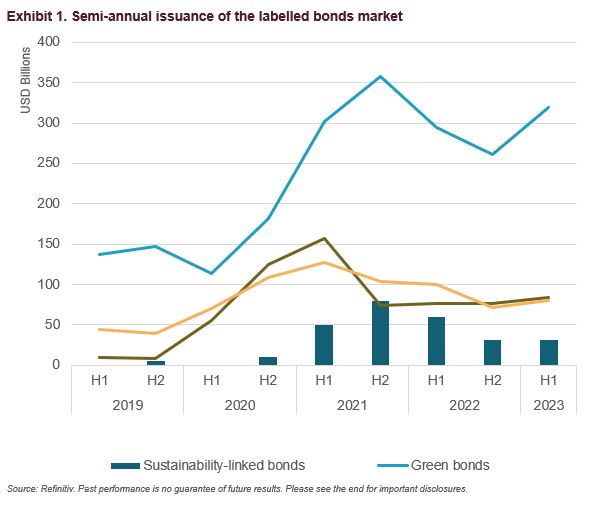

Like its counterparts, the issuance volume of SLBs have been affected by the broader fixed-income market volatility, leading to a slowdown in new offerings throughout 2022 and slower recovery in the first half of 2023 (Exhibit 1). This might also be tied to typical SLB market characteristics including the lack of frequent and large issuances from financials, supranationals and governments, as well as a greater presence of high yield issuers (28% for SLBs vs 4% for green bonds[i]) that are particularly vulnerable to the high interest rate market conditions. Nevertheless, the demand for SLBs has remained robust, with deals often being heavily oversubscribed and attracting premiums on the primary market[ii].

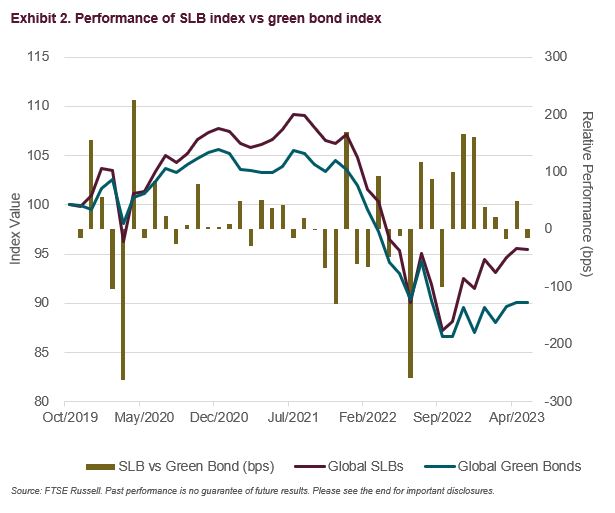

Recognising the need to track the performance of the SLB market, FTSE Russell has introduced the FTSE Global Sustainability-Linked Bond Index. Taking a transparent and cautious approach, the index comprises constituent SLBs that are aligned with the five core principles outlined in the International Capital Market Association (ICMA) Sustainability-linked Bonds Principles[iii]. And we have also seen positive results with the SLB Index showing resilient performance in a challenging market environment (FTSE Global Green Impact Bond Index) (Exhibit 2).

European Central Bank’s acceptance of SLBs as eligible collateral for the Eurosystem credit operations[iv], and the recent updates of ICMA’s Sustainability-linked Bonds Principles with additional guidance for sovereign and sub-sovereign issuers, are expected to further stimulate the SLB market. At the same time, the ongoing debates surrounding the credibility of targets and the meaningfulness of financial characteristics reflect its early stage of development.

Carbon targets take center stage for SLBs…

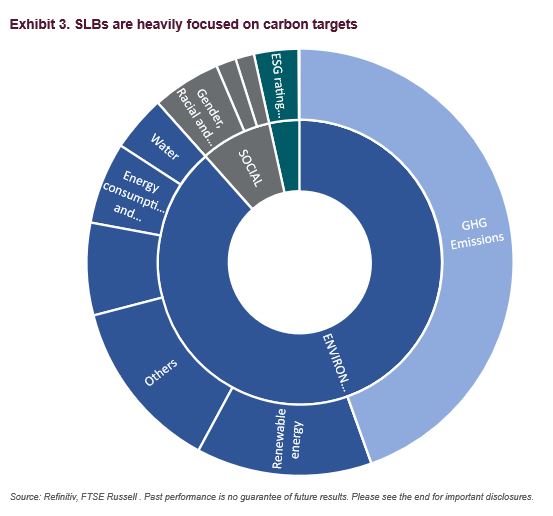

While issuers are afforded the flexibility to establish performance targets across a wide range of sustainability topics, carbon related targets have gained the most prominence. Our analysis of the entire pool of 923 targets across 585 SLBs reveals that 88% of targets are dedicated to environmental objectives. In contrast, social and governance-related targets account for 8% and 4% respectively. Notably, carbon targets comprise almost half of the overall count of targets (Exhibit 3). And 482 SLB deals have incorporated at least one carbon target, representing 83% of the total SLB issuance count.

As of H1 2023, 35 SLBs have passed their first observation dates. Out of these, only three SLBs have failed to meet targets, with two failing short on carbon targets. Consequently, the failures have triggered coupon step-ups and led to ESG rating downgrades for certain issuers[v]. Currently, investors tend to remain vigilant about corporates’ emission targets (including those set by SLB issuers), due to the nuances surrounding the ambition level and achievability. Going beyond SLB issuers, our recent study on emission targets of a wider scope of corporates shows, only one in three companies hit their emission reduction target for 2020 or prior[vi].

Although it has been perceived by a group of investors that to establish an effective SLB market, occasional failures should be embraced[vii], the market’s resilience awaits further examination as most SLBs are set to face their initial observation dates in 2025.

…with a focus on hard to abate sectors

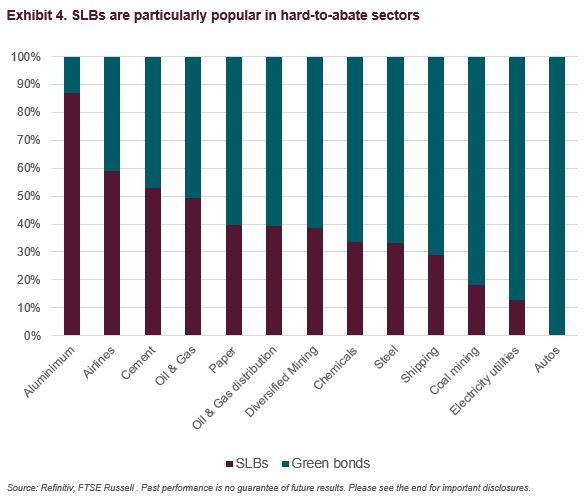

It’s noteworthy in this context that carbon-intensive, hard-to-abate sectors[viii] have been among the most enthusiastic SLBs issuers. For instance, cumulative issuance amounts of SLBs have seized a considerable share and surpassed green bonds in sectors such as Aluminium, Airlines, and Cement (Exhibit 4). While green bonds in these sectors still must earmark proceeds for eligible green projects such as renewable energy installation or green buildings, SLBs serve as a complementary avenue to unlock the finance for transition. They might find greater traction among corporations, especially those grappling with significant emission challenges, as the demand for transition grows more pronounced. Meanwhile, the credibility of both target settings and financial incentives requires closer scrutiny.

Understand the nuances of bond characteristics

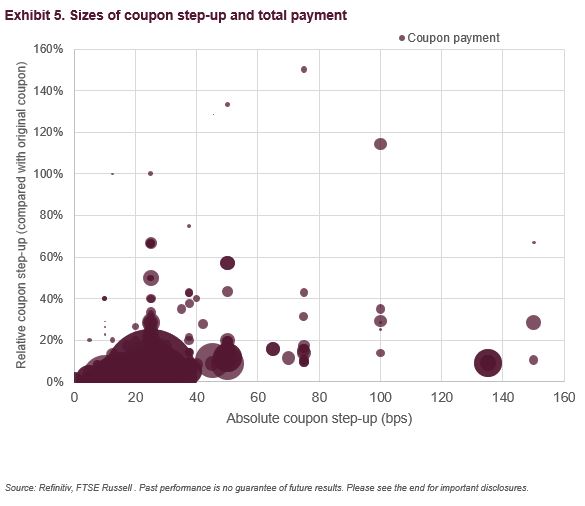

While there has not been a consensus on the meaningful financial and structural characteristics, issuers have embraced the coupon step-up structure, representing over 70% of all SLB targets. Our analysis found that the prevailing market practice is to employ a 25-basis point step-up, with the average basis points of step-up amounting to 10% of the original coupon. However, the market has shown a wide spectrum of variations (Exhibit 5).

Coupon attributes must be understood in the context of the underlying target’s robustness. For instance, while one could argue that a higher coupon step-up reflects the issuer’s determination to meet targets, a significant step-up in conjunction with a less ambitious target may be construed as an attempt of greenwashing.

Bond holders must also take into consideration the implication of an aggressive step-up, including the strain it could put on an issuer’s solvency and impact on the issuer’s credit risks. In Exhibit 5, the size of the bubbles indicates the potential total coupon payments of each bond upon step-up, highlighting a diverse range of outcomes and another layer of complication for investors to factor in their assessment. Again, understanding the ambition and achievability of targets is crucial for investors to objectively measure the fair value of SLBs and avoid overpaying for the non-pecuniary features of the bond[ix].

As the SLB market expands, we expect to see well-established norms at the issuer side and consensus among investors, as well as more transparent and relevant target settings which are imperative for fostering an efficient SLB market with minimal transaction cost.

For more information on Sustainable Investment and trends, subscribe to the blog.

Footnotes:

[i] Measured by the presence of high yield issuers in the FTSE Global Sustainability-Linked Bond index and FTSE Global Green Impact Bond Index respectively.

[ii] Investor Appetite Drives Pricing Benefits for Sustainability-Linked Bond (SLBs) | Climate Bonds Initiative

[iii] Sustainability-Linked-Bond-Principles-June-2023-220623.pdf (icmagroup.org)

[iv] FAQ on sustainability-linked bonds (europa.eu)

[v] Growing pains for SLB market as coupon step-ups loom | IFR (ifre.com)

[vi] Are corporations walking the walk on climate pledges? | FTSE Russell

[vii] Borrowers urged to issue more sustainability-linked bonds – OMFIF

[viii] TPI classification is used to define the scope of emission intensive sectors.

[ix] AFII SLB II (anthropocene fi.org)

First posted on FTSE Russell Blog on August 3rd, 2023

Shutterstock image by https://www.shutterstock.com/g/Pcess609

Disclosure:

© 2023 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) FTSE Fixed Income Europe Limited (“FTSE FI Europe”), (5) FTSE Fixed Income LLC (“FTSE FI”), (6) The Yield Book Inc (“YB”) and (7) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “FTSE4Good®”, “ICB®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under license, by FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB or BR. FTSE International Limited is authorized and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analyzing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing in this document should be taken as constituting financial or investment advice. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any representation regarding the advisability of investing in any asset or whether such investment creates any legal or compliance risks for the investor. A decision to invest in any such asset should not be made in reliance on any information herein. Indexes cannot be invested in directly. Inclusion of an asset in an index is not a recommendation to buy, sell or hold that asset nor confirmation that any particular investor may lawfully buy, sell or hold the asset or an index containing the asset. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back-tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This document may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a license from FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB, BR and/or their respective licensors.