By: Jose Torres, Interactive Brokers’ Senior Economist

Investors are brushing aside weaker-than-expected flash Purchasing Managers’ Index (PMI) data from the U.S. and the European Union and are instead focusing on the potential for Nvidia’s earnings call tonight to include a bullish outlook for artificial intelligence that could benefit the popular technology sector. Lower yields in response to this morning’s data are also shoring up market sentiment, with spectators anxiously awaiting Fed Chair Jerome Powell’s speech in Jackson Hole, Wyoming this Friday.

This morning’s August PMI shows that services continued expanding in the U.S., but almost slipped into contraction territory. Manufacturing, meanwhile, continued its sobering downward slide, an ongoing issue that started after central banks began raising interest rates and consumer demand for goods plummeted dramatically after shoppers splurged on home items and other goods during the Covid-19 pandemic. Europe was even less fortunate, with both services and manufacturing hovering in deep contraction territory, supporting wagers of a negative third quarter GDP print for the region.

U.S. Businesses Face Revenue Pressures

The U.S.’s August PMI of 50.4 for services and 47 for manufacturing is much worse than projections of 52 and 47. The disappointment in services was driven by a reduction in new orders, as customer ordering contracted amidst the sharpest decline in demand all year. Revenue pressures across both services and manufacturing prompted companies to stall hiring, with August’s pace of job creation halting to near-zero. Still, however, rising wages, higher commodity prices and lofty fuel expenses contributed to rising price pressures across the economy.

Europe Services and Manufacturing Contract

Similar to the U.S., the E.U. suffered this month from stagflationary vibes characterized by declining consumer demand amidst persistent cost pressures.

The U.S. can at least find company in its dreary PMI, with results for Europe being even more dismal. Services recorded a disappointing 48.3 score while manufacturing scored an even weaker 43.7. Services missed the consensus expectation of 50.5 while manufacturing came in a bit above 42.6. The results reflect continued contraction from July’s PMI of 50.9 for services and 42.7 for manufacturing. Similar to the U.S., the E.U. suffered this month from stagflationary vibes characterized by declining consumer demand amidst persistent cost pressures.

U.S. Housing Market Continues to Struggle

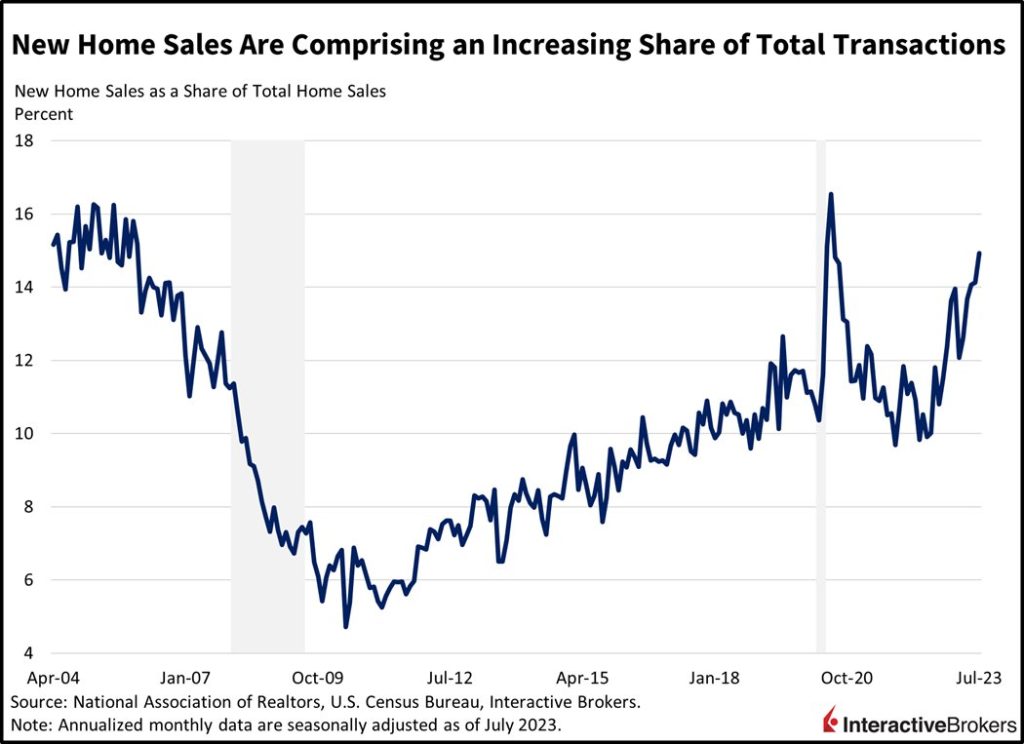

Higher interest rates, upward price pressures and reduced credit availability are not just pressuring consumers and manufacturers, with this morning’s mortgage applications release reaching a fresh 28-year low. The low level of transactions continues to be driven by sales of existing homes being essentially frozen due to the cost of moving having become significantly higher as low mortgage rates from the pandemic time period can’t be transferred from old residences to new ones.

New homes sales have benefited from this trend. July new home sales tallied 714,000 million seasonally adjusted annualized units (SAAU) while existing home sales totaled only 4.07 million SAAU. Sales for new homes came in above expectations of 705,000 SAAU and improved from June’s 684,000. Existing homes reflected the opposite trend, falling short of estimates of 4.15 million SAAU and declining from June’s 4.16 million. Homebuilder Toll Brothers has benefited from this trend and has generated strong year-over-year (y/y) sales growth despite housing becoming increasingly less affordable. Toll Brothers has passed at least some of its higher construction costs onto customers by increasing its prices while generating a 5% second-quarter y/y increase in the number of delivered units. Its revenue climbed 8%: Analysts anticipated a 4% decline. The company expects to deliver between 9,500 and 9,600 units this year, up from earlier guidance of between 8,900 and 9,500 units.

Markets Seek Direction

Markets are anticipating Nvidia’s results and Jackson Hole with optimism amidst broad-based gains in equities and softer bond yields. Tech is leading this morning, with the Nasdaq Composite Index up 1.5% while all other major U.S. equity indices are up by at least 0.4%. Sectoral participation is wide, with all sectors higher except for utilities and energy. Recessionary tilted data is weighing on Fed tightening expectations, the dollar and yields. Odds of a 25-basis point (bp) hike at the September and November meetings have shifted lower to 11% and 36%, respectively. The 2- and 10-year Treasury maturities are down 10 bps each to 4.95% and 4.22% while the Dollar Index is down 12 bps to 103.47. Softer demand conditions globally are weighing on energy markets with WTI crude oil down 0.9% to $78.91 per barrel.

Today’s decline in yields is a reverse for the bond market, even as yield-hungry investors are finding fixed-income asset pricing more attractive. The U.S. 10-year Treasury yield recently hit 4.36%, a level last reached in 2007. After cash in the U.S. Treasury declined during the debt ceiling debate in Washington, D.C., the country is replenishing its coffers. It has already issued approximately $600 billion in debt and is expected to issue another $700 billion by year-end. At the same time, the Treasury market has lost the following large buyers that have been less sensitive to debt yields:

- The Fed, which is engaged in quantitative tightening. It is allowing its balance sheet to decline as its existing debt holdings mature.

- Banks, which are increasingly holding on to cash for dear life instead of bonds after a bank run this spring caused the failure of various smaller regional banks.

- Foreign countries that are selling U.S. Treasuries in response to geopolitical matters.

Corporations Warn of Weakening U.S. Consumers

Macy’s and Lowe’s yesterday joined a growing list of retailers who have provided dreary forecasts for consumer spending. Their cautious statements were followed by similar comments from Foot Locker and Peloton this morning, causing their stock prices to tank more than 20%.

- Macy’s reiterated its June forecast of a 6% to 7% 2023 decline in same-store and licensed-store sales relative to last year. Consumers are increasing their spending on services, such as travel and entertainment, while balances for Macy’s credit cards are rising and the October resumption of student loan repayments is approaching. Despite these challenges, Macy’s second-quarter adjusted earnings per share (EPS) of $0.26 beat the consensus expectation of $0.13 and revenue of $5.13 billion exceeded the consensus expectation of $5.09 billion. For the quarter, comparable store sales declined 8.2% y/y.

- Lowe’s CEO Marvin Ellison expects consumers in the near term to continue spending less on discretionary do-it-yourself projects. From a longer-term perspective, the older age of housing and low inventory of existing homes for sale is likely to support sales of home renovation materials. Lowe’s maintained its guidance for comparable sales to decline between 2% and 4% this fiscal year. For the second quarter, it generated an EPS of $4.56 and revenue of $24.96 billion compared to the consensus expectation of $4.49 and $24.99 billion.

- Foot Locker shares tanked 30% this morning after the company said its second-quarter sales dropped 9.9% due to consumer softness. It expects sales to drop between 8% and 9% this year. After reporting a quarterly loss, it suspended its dividend.

- Peloton’s $642.8 million in sales declined from $678.7 million in the year-ago quarter. At the end of the second quarter, it had 3.08 million subscribers, up 4% y/y but a 29,000 quarter-over-quarter decline. The summer months tend to be slow because customers often stop exercising when they take vacations and Peloton, like many retailers, faces the challenge of consumers shifting their spending to travel, entertainment and other services. Additionally, a recall of Peloton bicycle seats caused many customers to pause their memberships.

A Doubleheader of Economic Action

With this morning’s economic and earnings data reflecting a consumer slowdown, the following doubleheader consisting of the following is on the calendar for this week:

- This afternoon’s earnings call by Nvidia may boost optimism on the artificial intelligence front and provide support to equity markets.

- This Friday’s speech from Fed Chairman Jerome Powell will inform market players of the Fed’s thinking regarding inflation, employment and financial stability. The recent rise in long-term yields and the health of the banking sector will be top of mind for investors while Powell and the committee consider how high and how long the fed funds rate should be. Similar to last March though, it’s only a matter of time before the Fed’s balance sheet trimming sparks an economic accident that is currently not priced into markets. In fact, the Fed’s assets are currently $193 billion lower than before the regional bank debacle that occurred this spring. Meanwhile, the balance ticks lower by the day to the tune of around $95 billion per month as quantitative tightening continues.

Visit Traders’ Academy to Learn about the Purchasing Managers’ Index and Other Economic Indicators.

This post first appeared on August 24th 2023, Traders’ Insight Blog

PHOTO CREDIT: https://www.shutterstock.com/g/Andrey+Suslov

Via SHUTTERSTOCK

DISCLOSURE: INTERACTIVE BROKERS

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.