Kevin Flanagan, Head of Fixed Income Strategy

For those looking for a summer respite for the bond market in August…think again. Based on trading activity as I write this, the U.S. Treasury (UST) market had something else in mind, specifically what has transpired for the UST 10-Year yield. This is a topic I blogged about a couple of weeks ago from a portfolio duration perspective. However, for this post, I wanted to get into the root causes of the recent increase in the 10-Year yield and whether it is reasonable to expect a reversal any time soon.

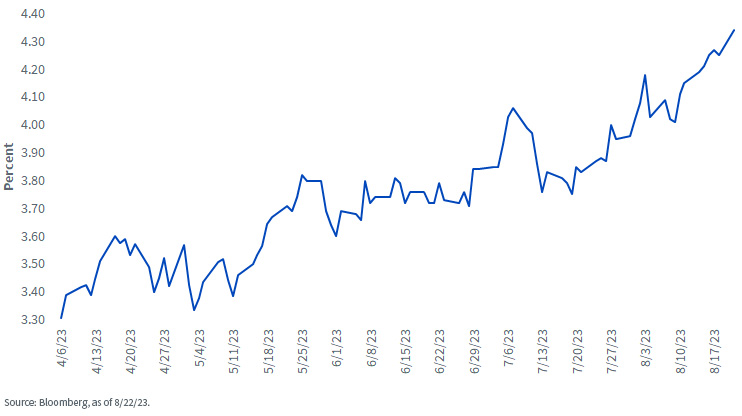

U.S. Treasury 10-Year Yield

Although there’s been somewhat of a seesaw pattern, the rise in the UST 10-Year yield really began back in early April. Since hitting its post-SVB low-water mark of 3.30%, the 10-Year reached as high as 4.34%, as of this writing, marking an incredible 100-basis point move to the upside, and eclipsing the prior high point of 4.24% that was printed back in October.

With the UST 10-Year yield now at its highest level in roughly 16 years, investors are wondering what comes next. In order to answer that question, we need to take a look at the reasons for this most recent move to the upside.

One does need to begin the process with the Fed. Although Powell & Co. are at, or close to, the end of this rate hike cycle, the policy makers continue to leave the door open for rate hikes. More importantly, the money and bond markets have now completely ruled out rate cuts for this year, pushing the timing for the potential first Fed Funds decrease to the end of Q1 next year, at the earliest. After much resistance from the money and bond markets, they have finally embraced the ‘higher for longer’ scenario.

Next up is the resiliency of the U.S. economy, especially the labor markets, where a widely expected recession for 2023 has essentially been removed from the equation, at least for this year. Along the same lines, even though inflation continues to cool overall, core price pressures have remained above the Fed’s 2% threshold. Add to these macro factors increasing supply concerns for Treasuries from trillion-dollar deficits, and voila, the next thing you know, the UST 10-Year yield experienced a technical breakout to the upside utilizing Fibonacci retracement levels.

So back to the title of this blog post. In order for the UST 10-Year yield to fall on a sustained basis from here, you have to peck away at the aforementioned factors. To begin with, the economy needs to show definitive signs of heading for a downturn (look to labor market data), with some added cooling in inflation. This could potentially push the Fed into a more friendly narrative on just how long rates have to stay in restrictive territory. Unfortunately, the supply issue is not going away any time soon and could get worse as the Treasury announced that more increases in coupon auction sizes could be coming in October.

Conclusion

Considering the recent momentum to the upside for the UST 10-Year yield, some consolidation could be expected in the near term. However, the path of least resistance, at this point, seems for the 10-Year yield to remain elevated.

This post first appeared on August 23th, 2023 on the WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/Rudzhan

Via SHUTTERSTOCK

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}

{kind=link}