By, Aneeka Gupta, Associate Director of Research at WisdomTree

2023 is off to a cautious start, heralded by the International Monetary Fund (IMF). It has warned that the upcoming recession will likely leave the global economy fundamentally damaged—with a recession in the U.S., a deeper slowdown in Europe and a drawn-out recession in the United Kingdom. This is quite possible; however, the current downturn may not look like downturns of the past as it’s supported by a more resilient labor market. As we transition to 2023, three questions from 2022 remain unanswered:

1. How sticky will the underlying inflation be?

2. How intense will the recession be?

3. Will we find a solution to Europe’s energy crisis?

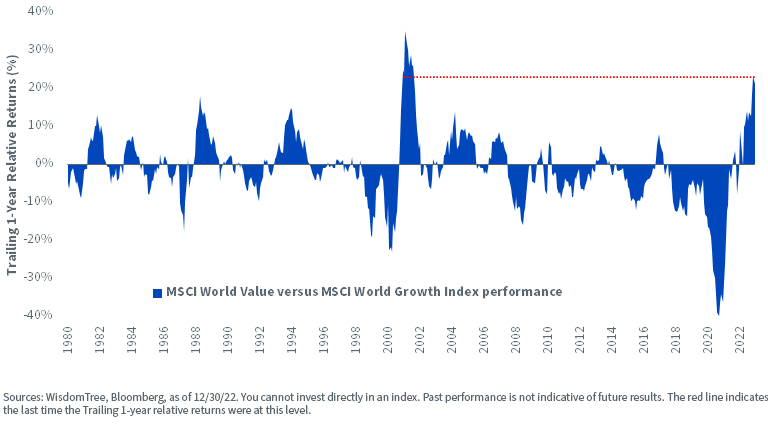

2022 was a tough year for equities, as evident by the 20% decline in the global stock market capitalization to $96.6 trillion1. Expensive growth stocks that had driven markets higher over the past decade began to correct sharply as the interest rate regime changed. In contrast, value stocks, while down for the year, were relative outperformers. The MSCI World Value Index outperformed its growth counterpart by 21% this year.1 The rising rate environment had a strong role to play in the higher relative performance.

Rotation from Growth into Value Stocks

Central Banks Turn up the Hawkish Rhetoric

While inflation has begun showing signs of easing globally, central banks in the U.S., Europe and the UK continue to remain hawkish. The Federal Open Market Committee’s (FOMC) new forecasts for the economy and policy showed few signs that the inflation picture is improving meaningfully. Federal Reserve (Fed) Chair Powell made clear in the December meeting that he wanted to see “substantially” more progress on inflation before the hiking would stop. The Fed is pointing out that there is no Fed put left while markets continue to misprice what the Fed is going to do.

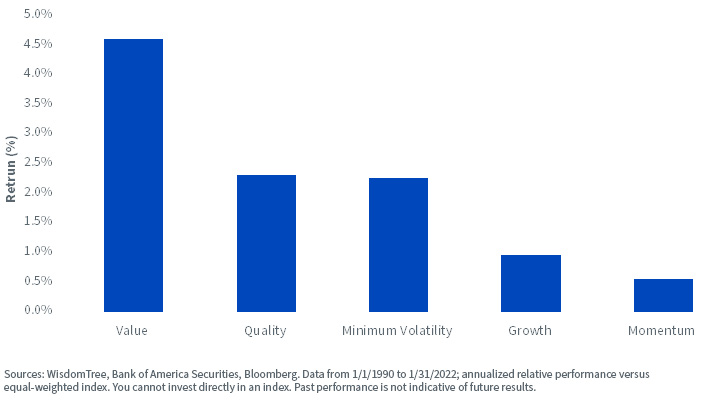

The latest European Central Bank (ECB) projections show inflation is unlikely to reach the 2% target until late 2025. At its December meeting, the ECB took a hawkish turn, and we think it is likely to hike by 50 basis points (bps) at least twice more, in February and March 2023. Similarly, in the UK, the Monetary Policy Committee (MPC) will need to see core consumer price index (CPI) inflation slow materially before the MPC stops its rate hike cycle. The key question in 2023 remains how sticky inflation will be on the upside (how soon it will approach the central bank’s targets), as it will determine the likelihood of central banks maintaining their hawkish stance on monetary policy. Historically, the value factor has demonstrated resilience during periods of interest rate volatility.

Factor Performance during Periods of Above-Average Interest Rate Volatility

De-risking Your Equity Portfolio with the High-Dividend and Value Factors

As interest rate volatility is poised to remain high, value-oriented stocks such as Financials, Energy, Utilities, Health Care and Industrials may be in better shape to withstand a slowdown. This is because value companies tend to make their money in the near term, owing to which earnings for these companies are less discounted than for growth companies whose significant profits and cash flow are expected to occur far in the future. Value stocks also have a better chance of defending and/or growing their operating margins than growth stocks.

The high-dividend factor is synonymous with an investment strategy that gains exposure to companies that appear undervalued and have demonstrated stable and increasing dividends. The strong performance of the dividend factor in 2022 has been a function of its close relationship with stocks with more stable fundamentals alongside the rising rate environment.

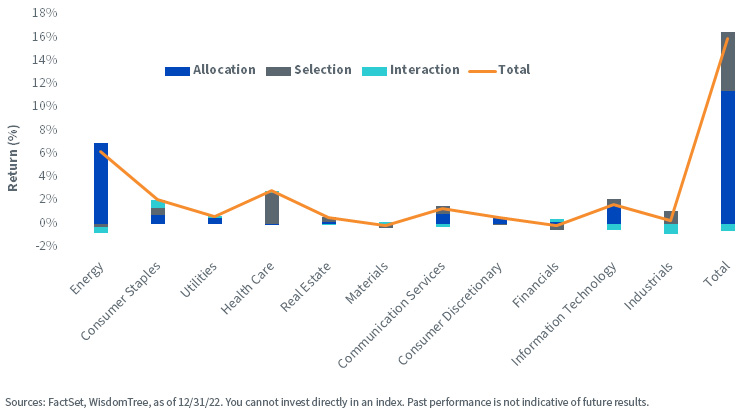

What Worked in 2022?

As illustrated in the sector attribution (below), the allocation has been positive, contributing to the tracking difference by +11%. The overweight in Energy, Information Technology and Consumer Staples benefited performance by +7%, 2% and 1%, respectively, last year.

Sector Attribution – 2022

1 Source: Bloomberg, as of 12/30/22.

This post first appeared on January 12th, 2022 on the WisdomTree Blog

PHOTO CREDIT: https://www.shutterstock.com/g/Costello77

Via SHUTTERSTOCK

Disclosure:

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.