By: Steve Sosnick, Chief Strategist at Interactive Brokers

The “January Effect” is a well-known market phenomenon with a reasonable amount of logic behind it. It theorizes that stocks that were beaten down by tax-loss selling during the latter months of a year can rebound substantially once the calendar turns. The tax code explains not only the desire for investors to lock in losses before a tax year ends, but also why bounces tend to occur only after a delay. The “wash-sale” rule highly incentivizes investors to wait 30 days before re-entering an investment in which one has taken a loss.

When we consider the multitude of formerly high-flying stocks that sank sharply into year-end 2022, there were ample opportunities for both tax-loss selling and a sizable rebound this month.

The January effect can go a long way to explaining rallies that we are seeing in stocks like Meta Platforms (META) and Amazon (AMZN) over the past couple of weeks. Bearing in mind that 2023 is only two weeks old, their 13% and 16% year-to-date moves are quite impressive. Of course, when the former lost nearly 2/3 of its value in 2022 and the latter was essentially cut in half during that year, we need to put the current moves in perspective. One can argue that those stocks and a whole raft of similar names, were oversold into late December and ripe for a bounce. Considering that many of the most affected stocks are among the most significant in market-capitalization weighted indices like the S&P 500 (SPX) and especially the NASDAQ 100 (NDX), it is logical that we would see those measures bounce as well.

But the January effect appears to be only one piece of the current rally. We are seeing high ratios of advancing to declining stocks on both NYSE and NASDAQ listed names. That indicates broad-based buying. It may be led by January effect stocks, but it is hardly limited to them. The Russell 2000 Index’ (RTY) 7% year-to-date gain outpaces SPX’ 4.3% and NDX’ 5.8% jumps. It is also important to keep in mind that US markets are relative underperformers. A wide range of European, Asian and emerging markets are accelerating even faster than the US. For example, the Euro Stoxx 50 Index (ESTX50) is up over 11% year-to-date. The global rally can hardly be explained simply by US tax policy. Investors around the world are much more willing to assume equity risk than they were just a few short months ago.

Why the enthusiasm? At one level, things are not as dire as they might have appeared last autumn. We were very concerned about how the Ukraine invasion would impact energy supplies to Europe ahead of winter. I’m not sure if their freakishly mild winter is a good thing in the long-term, but it certainly has been beneficial from a short-term economic basis. China has relaxed its zero-covid policy, leading many to be enthusiastic about the positive impact of that nation’s reopening on the global economy. Meanwhile, central banks appear to be relaxing their pace of rate hikes, leading many to believe that it harkens a potential return to accommodative policies.

That strikes me as a leap in logic. Less restrictive does not automatically mean accommodative. Ask yourself why a central bank that has gone to historic lengths to fight inflation would immediately reverse its rate hikes. It is quite logical that central bankers might stop raising rates if inflation ebbs, another to simply assume that they will start cutting them without a definitive signal that price pressures have clearly abated.

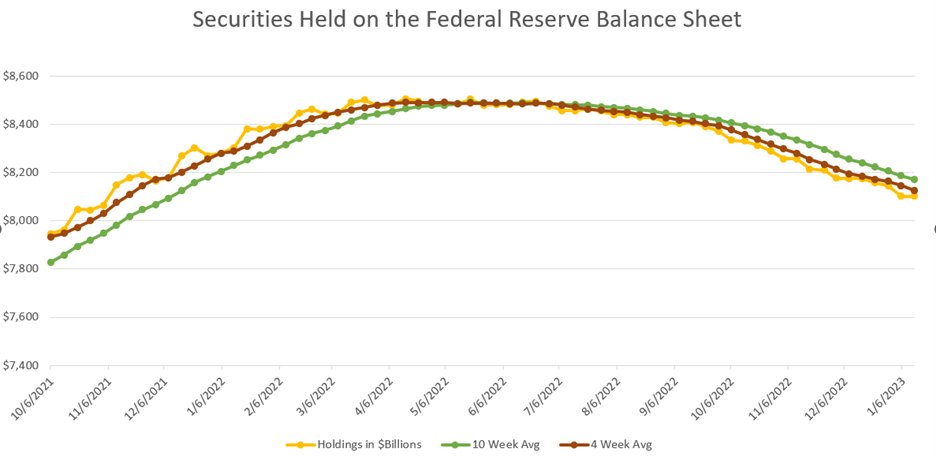

Yet the market appears to be assuming that this leap in logic will occur. We have noted that Fed Funds futures are pricing in three 25 basis point rate cuts by this time next year. Based upon what? It is hard to imagine that the Fed will say “mission accomplished” on the inflation front with less than a full year of hard data to that effect. Various Fed talking heads have made their intention to maintain peak rates through year end quite clear. And don’t lose sight of the fact that the Fed and other central banks remain committed to shrinking their balance sheets. We have just about given back all of last year’s balance sheet increase, but that included an end to quantitative easing (QE) and a slow start to quantitative tightening (QT). If we maintain the current pace of QT, we are likely to give back all of 2021’s QE in 2023. That is certainly a restrictive policy.

Of course, a rapidly weakening economy or a major financial accident could justifiably induce the world’s central banks to return to accommodation. But that is at odds with the idea of economic recovery or even a soft landing. It undercuts much of the basis for the recent rally. Investors need to decide if they’re hoping for a solid economy or central bank accommodation. It is hard to imagine getting both.

This post first appeared on January 17th, 2022 on the IBKR Traders’ Insight Blog

PHOTO CREDIT: https://www.shutterstock.com/g/X_Man

Via SHUTTERSTOCK

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers LLC, its affiliates, or its employees.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

{kind=link}

{kind=link}