By: Pierre Debru, Head of Quantitative Research & Multi Asset Solutions at WisdomTree in Europe

2022 continues to prove difficult for investors around the globe. The conjunction of heightened geopolitical risks, increasingly hawkish central bankers and runaway inflation forced many investors to change tack and modify their asset allocation significantly in the last 12 months. Duration has been lowered across asset classes, and a survey we commissioned recently revealed that 77% of European professional investors use equities to hedge against inflation1.

Fighting Inflation by Wielding Pricing Power

Not all equity investments are equal in the face of inflation. The key differentiator is their pricing power. Pricing power describes the ability of a company to increase its price without impacting demand or losing market share to competitors. In an inflationary environment, margins are under pressure because companies “import” inflation, whether they want it or not. Overall costs for the companies increase through labor, supply or energy. The only tool to mitigate the impact of inflation on margin is to increase prices. Companies with pricing power will be able to do so the most efficiently, creating tailwind versus competitors.

Certain types of companies tend to have higher pricing power:

- Companies that deliver essential services tend to wield a lot of pricing power as they have somewhat captive clients. This is the case for many companies in the Consumer Staples, Health Care, Utility or Energy sectors.

- Companies that deliver high-quality products or services and possess a distinct competitive advantage can also increase prices efficiently.

- Luxury goods companies benefit from their clientele’s relatively low price sensitivity.

- Some companies can benefit from favorable supply-demand dynamics at a particular point in time. This is, for example, the case of semiconductors in 2021 or energy companies this year.

History Is One of the Best Guides to the Future

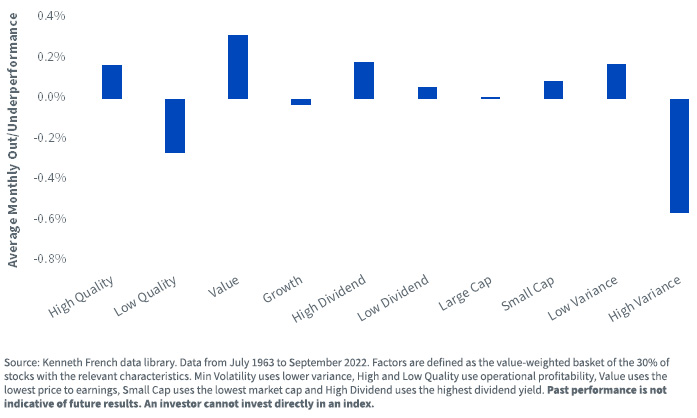

As is our habit when trying to assess the future, we turn to the past for guidance. The below graph focuses on U.S.-listed stocks since the 1960s. It assesses the average outperformance or underperformance of different groupings of stocks since the 1960s when inflation is higher than the last five-year average. We observe that on average:

- High-quality stocks weathered inflation better than low-quality stocks

- Value stocks beat growth stocks

- High-dividend stocks outperformed low-dividend stocks

- Small cap and low volatility did better than large-cap or high-vol companies

Overall, high-quality, high-dividend and cheap stocks appeared to fare better in high-inflation environments.

Historical Monthly Overperformance vs. S&P 500 When Inflation Is above Five-Year Average

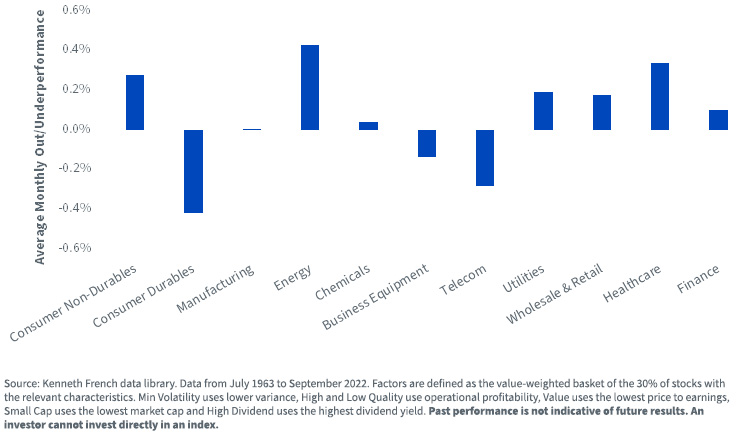

The same analysis on sectors shows that value-oriented, high-dividend sectors also tend to do better against inflation. Energy, Health Care, Consumer Non-Durables (Food, Tobacco, Textiles) and Utilities exhibit the strongest average outperformance during high inflation.

Historical Monthly Overperformance vs. S&P 500 When Inflation Is above Five-Year Average

It is clear here that the quantitative data aligns with our qualitative assessment. The factors and sectors that historically outperformed when inflation was high are those that have the most chance to harbor high-pricing-power companies. This should give investors clear indications on how they can tilt their portfolios to fight inflation.

Quality and Dividend Growth to Fight Inflation

In light of the unique challenges equity investors face, we believe that high-quality companies focusing on dividend growth could help strengthen portfolios. High-quality companies exhibit an “all-weather” behavior that tends to deliver a balance between building wealth over the long term and protecting the portfolio during economic downturns. Dividend-paying, highly profitable companies tend to:

- Exhibit higher pricing power, allowing them to defend their margins by passing the cost inflation to their customer

- Exhibit lower implied duration, protecting them in a rate-tightening environment, thanks to a focus on short-term cash flows

- Provide a defensive tilt and an enhanced capacity to weather uncertainty

This post first appeared on December 8th, 2022 on the WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/rozbyshaka

Via SHUTTERSTOCK

Pierre Debru is an employee of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management Inc.’s parent company, WisdomTree Investments, Inc.

1 Source: CoreData Research, Pan-Europe Professional Investor Survey Research, July/August 2022

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.