By Steve Sosnick, Chief Strategist at Interactive Brokers

My fellow investors…. Longs, shorts, speculators, hedgers, value players, growth junkies, trend-followers, and contrarians: welcome to today’s missive.

The state of today’s market is uncertain. I say this with the recognition that markets are always uncertain, but the current environment is demonstrably more uncertain than the one to which we’d become accustomed.

VIX readings above 30, when we had consistently seen levels in the teens for most of the past two years, is a testament to that notion.

Volatility is how the markets express investors’ inability to reach a consensus on value, and there are a multitude of significant factors that defy easy consensus.

2022 Dynamics

As the year began, I alerted you to the likelihood of this scenario, saying:

“The primary theme is for investors to expect more volatility than we’ve seen over the past year-and-a-half. The changing monetary environment should be the cause.”

At the time, major indices were at or near all-time highs and VIX was about 17. Since then, we have seen a 10% correction in the S&P 500 (SPX) and a near 20% drop in the NASDAQ 100 (NDX).

The latter figure could indicate the presence of a bear market, but even though long-term moving averages are now pointing lower, we’ll refrain from making that call right now. A good portion of the declines can be explained by geopolitical events that were unanticipated and difficult to model.

Monetary Punch

Since March 2020, markets had been the beneficiaries of unprecedented amounts of fiscal and monetary stimuli.

With the passage of the recent infrastructure package, it appears that the last of meaningful fiscal support is now behind us, and as of September 2021, the Federal Reserve has been preparing us to see the reversal of fiscal stimulus.

The first step was to be the reduction of quantitative easing (QE) via a tapering of the Fed’s monthly bond purchases, followed by gradual, sequential hikes to the Fed Funds rate. Bear in mind that we still have not yet seen a rate hike in the US, though we have seen them in the UK, Canada and elsewhere.

Also bear in mind that the holdings of securities on the Fed’s balance sheet have continued to grow at a pace only slightly below the $120 billion monthly increase that defined recent QE. Furthermore, while reverse repo utilization has ebbed slightly, it remains the case that over $1.5 trillion seeks an overnight resting place at the New York Fed.

Tightening Looms

Markets have been reacting negatively to the prospect of monetary tightening – they are of course discounting mechanisms – but history shows that stock prices usually react to changes in monetary conditions with a 4-6 week lag.

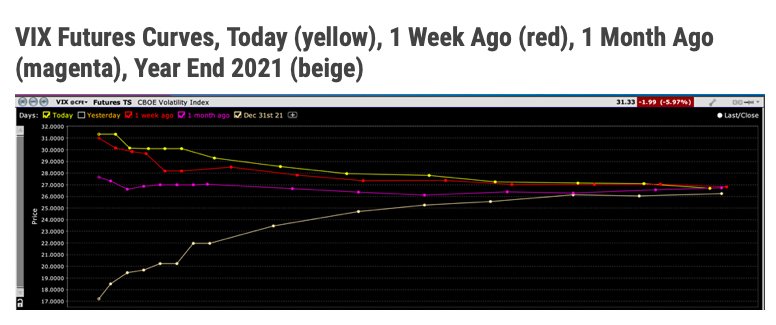

We can’t be certain what will transpire if and when monetary conditions actually change, and once again that uncertainty is likely to be reflected in continuing volatility. VIX futures reflect that point of view, as evidenced below:

Source: Interactive Brokers

VIX Futures

To be fair, VIX futures traders can be wrong. The chart above demonstrates that. VIX futures were anticipating current levels to be in the low 20’s – decently above the spot index at that time, but well below the levels we see now.

This morning we received a bout of clarity on the monetary front. During Congressional testimony, Chair Powell acknowledged that rate hikes would likely begin with a 25-basis point move in March, with similar hikes to follow sequentially unless the inflationary picture worsens.

He also believes that inflation will peak and come down in ensuing months. In other words, he still believes inflation is transitory. That said, the bond market implicitly shares that view.

The Fed

Some of you might question how much worse it would need to get before the Fed would react even more aggressively, but the Core PCE Deflator, the Fed’s preferred inflation metric, rose “only” 5% in the fourth quarter of 2021, which is below the February non-core CPI and PPI readings of 7.5% and 9.7% respectively.

A 4Q reading is well behind the rapidly accelerating conditions that we had seen even prior to the shocks in oil and grain futures that have occurred in recent sessions. Today’s rally in equities tells us that traders have largely removed faster rate hikes from their psyches, Powell caveat or not.

It is important to bear in mind that we have yet to feel the full economic effects of the events in Ukraine. I can’t think of a precedent for severing one of the world’s largest economies from the global systems virtually overnight.

Billions of dollar’s worth of Russian assets were obliterated overnight and various key futures spiked higher, yet we have not heard word of cascading troubles at the institutions that own those assets. That too can take time, as we learned from the 1998 demise of Long Term Capital Management that followed a Russian default by a few weeks.

It would be wonderful if the system was robust enough to avoid any contagion, but it is too early to say that we have fully avoided any troublesome outcomes.

Like our President, I also decline to address Tesla in this speech, by the way. God bless and good day.

This post first appeared on March 2 on the Traders’ Insight blog.

Photo Credit: greg westfall via Flickr Creative Commons

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers LLC, its affiliates, or its employees.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

DISCLOSURE: FUTURES TRADING

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.