By Nitesh Shah, Director of Research, WisdomTree Europe

Our commodity outlook for the coming year will be shaped by three major drivers:

- A higher inflationary environment than we have seen in recent decades

- A structural increase in demand for commodities driven by an infrastructure boom

- A renewed focus on the environment that will increase the demand for certain commodities and at the same time present challenges for supply growth

While none of these drivers are new, and we have been talking about them for the past year, in this blog post we will provide an update on how each of these drivers is progressing. In 2021, commodities were an outperformer, and we are entering 2022 with extremely strong momentum.1

Reflation

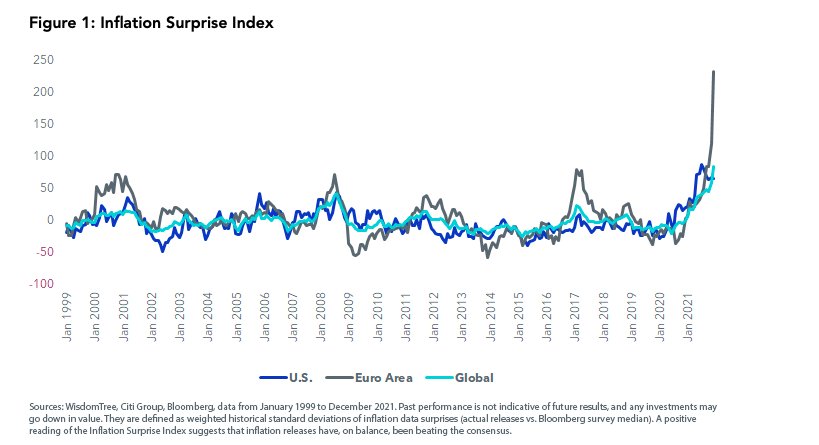

Although we have been talking about inflation rising for some time, the market seems to have been caught by surprise.

Figure 1 shows an Inflation Surprise Index—i.e., the extent to which actual inflation has come in higher than expected by the market.

Inflation Higher

Although central banks—including the U.S. Federal Reserve—have dropped their “inflation is transitory mantra” and are preparing to tighten policy, their actions can only impact demand growth.

A key source of much of the inflation we have seen in the past year has been supply-side disruptions. As Omicron cases rise globally, there is a cogent reminder that supply-side frictions are not guaranteed to dissolve. So, as we get used to living with COVID-19, we may also have to get used to living with elevated inflation.

Hedging Strategies

Investors looking to hedge against elevated inflation, especially unexpected inflation, would be wise to look at the commodity complex.

Whether we talk about gasoline pipeline disruptions driving up the price of gasoline or drought conditions pushing up the price of food, there are many commodities whose prices will react, providing a natural hedge to the increasing price pressures felt in a consumption basket.

Infrastructure Boom

Following the COVID-19 pandemic, the political will to support infrastructure projects has strengthened. In Europe, a budget of close to €2.018 trillion in current prices has been devoted to the recovery.

More than 50% of the budget will support modernization through research and innovation, fair climate and digital transitions and developing resources for health preparedness. All these initiatives will require some form of infrastructure improvements.

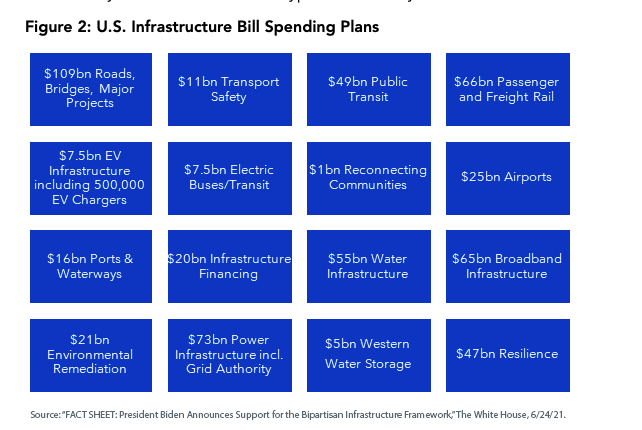

In the U.S., the Senate passed a US$1.2 trillion infrastructure bill . While watered-down from its original US$2 trillion design from the White House, the bill’s approval was unusually bipartisan. Figure 2 highlights some of the infrastructure initiatives the bill contains. We believe that this will act as a strong catalyst for commodity demand in the U.S.

Infrastructure projects are commodity intensive, and they tend to last a long time. Therefore, the impact on commodity markets may transcend more than a typical business cycle.

Energy Transition

We believe an energy transition will take place, where we will move rapidly away from the consumption of hydrocarbons, which produce lots of greenhouse gas emissions, to renewable energy sources.

Driving this trend are the commitments to the Paris Agreement—a legally binding international treaty on climate change with a goal to limit global warming to well below 2 degrees Celsius and preferably to 1.5 degrees Celsius, compared to pre-industrial levels.

All the materials that support renewable energy and the technologies that enable the practical use of renewable energy such as batteries will be in greater demand.

An electrification of road transportation will augment this trend. In the commodity markets, this will be broadly favorable for base metals including copper, nickel, aluminum, zinc and tin.

The Supply Challenge

In addition, a renewed focus on environmental outcomes will push miners into better environmental practices: more careful dealing of tailings, avoiding mining in ecologically sensitive areas, reducing green-house gas emissions in the mining process.

All of these will be welcome developments to make the industry more sustainable. However, we may find that mining activity slows while the industry makes this adjustment.

In 2021, China’s crackdown on its aluminum industry, which relies heavily on coal for its power needs, was an example of supply pressures arising from tighter environmental policies. With China being the world’s largest aluminum producer, the metal could remain undersupplied for years as the industry transitions to cleaner alternatives for its energy needs.

Conclusion

Commodities entered a bull cycle in 2020 after what we believed was the worst of the COVID-19 pandemic was behind us, and this rally continued into 2021. However, lingering COVID-19 effects are hampering supply chains and driving inflation higher.

Commodities are a hedge for inflation and generally are likely to prosper, especially in the shadow of a monetary largess that is already in the system.

In my opinion, even if the inflation catalyst wanes as we move to the next business cycle, the boom in infrastructure and an energy transition will likely propel many commodities for years to come.

This post first appeared on January 27 on the WisdomTree blog.

Photo Credit: Charlie Day via Flickr Creative Commons

Footnotes

1 In calendar year 2021, the Optimized Roll Commodity Total Return Index (EBCIWTT Index) rose 27.3%, real estate (RUGL Index) rose 27.2%, world equities (MXWD Index) rose 16.8% and bonds (LGSVTRUU Index) fell 3.5%. All data sourced from Bloomberg.

2 “Recovery plan for Europe,” European Commission. https://ec.europa.eu/info/strategy/recovery-plan-europe_enRichard Cowan and Susan Cornwell, “U.S. Senate pivots to $3.5 trillion bill, key to Biden’s agenda,” Reuters, 8/10/21.

Disclosure

Commodities are generally volatile and are not suitable for all investors. Investments in commodities may be affected by overall market movements, changes in interest rates and other factors such as weather, disease, embargoes and international economic and political developments

{kind=link}