By Nicolas Lancesseur, senior research lead, sovereign climate

Not all net-zero targets are created equal.

Depending on historical and current carbon emissions, some are more ambitious than others. And, crucially, many such pledges are inconsistent with nearer-term targets – the 2030 goals set out in the Nationally Determined Contributions (NDCs) as part of the Paris Agreement process – as well as countries’ existing suites of decarbonisation policies.

An analysis of these discrepancies can help investors gauge, in the current international momentum for climate action, the risk incurred by countries that do not engage seriously enough to decarbonize their economies. These analyses also help investors wanting to construct portfolios of sovereign debt that are better aligned with the objectives of the Paris Agreement.

To undertake such an analysis, for our Net Zero Atlas paper, Beyond Ratings and FTSE Russell have developed an innovative methodology to assess a country’s level of commitment to decarbonisation and to provide an indication of ‘Paris-alignment’ for sovereign issuers. It offers an analytical framework that allows investors to systematically compare climate commitments.

Temperature Rise

To do so, it provides a measure of the “Implied Temperature Rise” associated with a country’s commitment to limit its GHG emissions.

This provides a consistent, if highly stylised, metric to measure commitments across countries and over time, and to assess their alignment with global warming trajectories.

FTSE Russell funded a research project led by individuals from the International Institute for Applied Systems Analysis (IIASA) and the NewClimate Institute to construct a database based on the mitigation measures implemented by 30 countries, representing 81% of global emissions (see Nascimento et al. 2021)[1].

Scenario Analysis

For each country, an Implied Temperature Rise was calculated for three scenarios: Net Zero targets (generally with a 2050 time horizon, but to 2045 for Germany and Sweden, and 2060 for China), NDCs and Current Policies, following four steps[2].

The first is to estimate annual GHG emissions per capita and population for each country for 2030 (separately for NDCs and current policies) and for the date of its net-zero target. This is based on the reductions implied by the announced NDCs and net-zero targets, assuming that countries meet their goals.

For Current Policies, this is based on detailed projections that assume no additional mitigation action will be taken beyond the currently implemented policies.

Carbon Budget

The next step is to assign percentage shares of the global annual carbon budget in 2030 and mid-century to individual countries – that is, the total emissions that can be emitted while holding the global average temperature rise to below 2°C.

We then calculate the implied global emissions for each country’s Net Zero target, NDCs and Current Policies, approximately on the level of global emissions that would result from all other countries having the same implied level of effort as the country in question.

Finally, we then translate carbon emissions volume into a temperature increase to provide an implied temperature rise for each country.

On average, we find that the current Net Zero targets will, if met, collectively deliver a global temperature rise of 2.1°C, well above the 1.5°C targeted by the climate talks. Among the G20, the most ambitious target is that of the UK, which is aligned with 1.5°C, and the least ambitious is that of Saudi Arabia, which is aligned with 2.9°C of warming. This is due to the latter’s relatively high level of per capita emissions and the percentage of its carbon budget that it has already consumed.

Emerging Markets

The research also shows that few existing NDCs are aligned with Net Zero commitments: the average NDC implies 2.8°C of warming, 0.7°C higher than the average Net Zero target. Countries’ current policies only slightly lag their NDC commitments, leading globally to a 3°C warming trajectory.

But this average masks some laggards, including several rich-world countries, whose current policies are some way behind their NDC goals. For example, current policies in the US and Canada are tracking towards a 4°C+ trajectory, but their 2030 NDC commitments are aligned to 3°C. Germany and South Korea are also some way adrift.

This suggests that it could prove very challenging for carbon-intensive economies to align with 1.5°C over the course of a decade through domestic action alone, and that they might need to turn to the Paris Agreement’s Article 6 international market mechanism to fund carbon mitigation overseas.

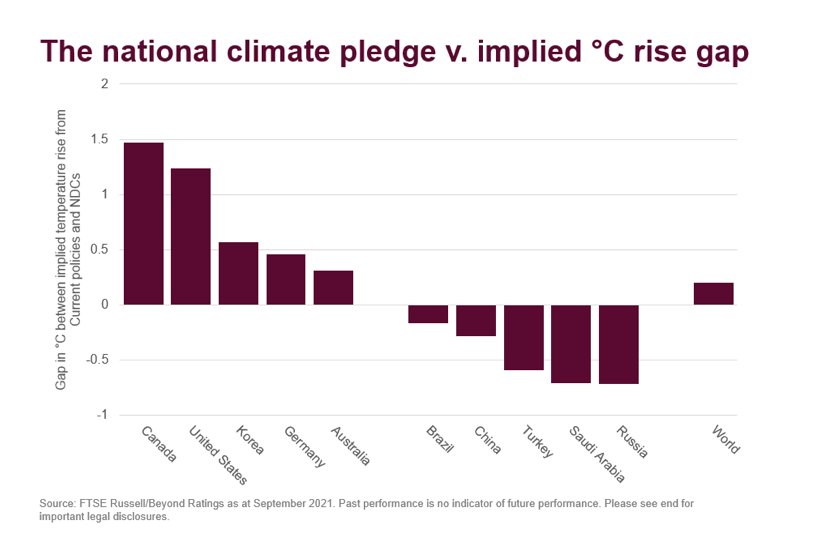

Conversely, a number of large emerging economies actually have more ambitious policies than NDCs. Russia, for example, has policies in place that are aligned to a 0.7°C lower trajectory than its NDCs. Turkey’s policies are 0.6°C lower, and China’s 0.3°C. These countries appear well-positioned to increase the ambition of their NDC commitments (see chart below).

Portfolio Implications

So what does this mean for investors? We believe this research has two practical applications.

The first is to enable investment managers to construct sovereign debt portfolios that are aligned, to the extent possible, with the 1.5°C Paris Agreement warming trajectory.

While an entirely aligned portfolio would currently be impossible – or at least extremely poorly diversified – portfolios could be constructed that offer considerable improvement in alignment compared with the benchmark (a portfolio tracking the FTSE World Government Bond Index would be aligned with an implied temperature rise of X.X°C, for example).

Second, a country’s Implied Temperature Rise provides a measure of sovereign climate risk. A country whose current policies, NDC or Net Zero target is substantially misaligned with the 1.5°C trajectory is likely to face pressure to ratchet up its climate policies.

Takeaway

In addition to growing moral pressure from the international community and domestic stakeholders, climate laggards face more concrete economic penalties. For example, the EU’s proposed Carbon Border Tax Adjustment aims to penalize exporters that are not subject to an appropriate carbon price.

A rapid response to these pressures is likely to create a greater drag on sovereign performance than a more gradual decarbonisation.

The announcement in Glasgow on 1 November that India has become the latest major economy to commit to Net Zero – albeit not until 2070 – illustrates the extent to which the international community now recognises the imperative to halt emissions.

But it also shows that investors need to understand the detail behind each country’s commitments.

This post first appeared on December 15 on the FTSE-Russell blog.

Photo Credit: GPA Photo Archive via Flickr Creative Commons

References

[1] Nascimento, L., Forsell, N., Batka, M., Kuramochi, T., Illenseer, N., Subtil, C. and Lancesseur, N., 2021, Tracking climate mitigation efforts in 30 major emitters: Economy-wide projections and progress on key sectoral policies https://newclimate.org/2021/11/02/tracking-30-major-emitters/

[2] See Emin, G. et al., 2021, How to measure the temperature of sovereign assets, FTSE Russell

DISCLOSURE

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put.

Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance.

Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.