By Mark Barnes, head of investment research (Americas), and Christine Haggerty, global investment research

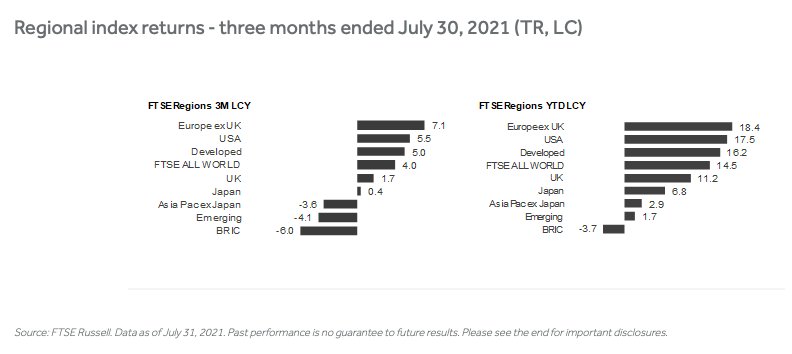

Global equity markets have diverged widely lately, with European and US stocks strongly outperforming the rest of the world. Investors have become increasingly discerning, rewarding the stocks of the economies making the strongest progress in jump-starting their economies and profit growth amid accelerating vaccination rollouts, continuing policy support and tailwinds from a global capex cycle.

Winner’s Corner

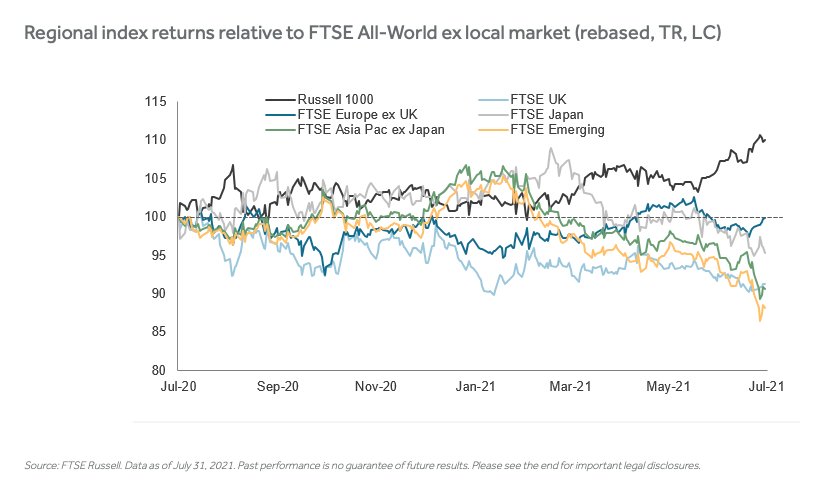

As illustrated below, the huge upswing since mid-June has catapulted the Russell 1000 firmly in the winners’ corner, with a 10 percentage point lead over the rest of the world for the past 12 months. Over that same period, relative performances elsewhere have lurched more deeply into negative territory, particularly in emerging markets, developed Asia and the UK. Despite recent strength, Europe has performed roughly in line with its global peers since last year.

In large part, US outperformance reflects the dramatic shift in investor preferences away from the cyclically sensitive stocks in favor earlier in the year into higher-quality, traditional growth industries. The latter group has rebounded strongly as the rapid spread of the Delta coronavirus variant and persistent supply-chain shortages have raised concerns about the durability of the global recovery These stocks have also benefited from the easing in US long bond yields, as it lowers the discount investors apply when valuing such companies’ future cash flows.

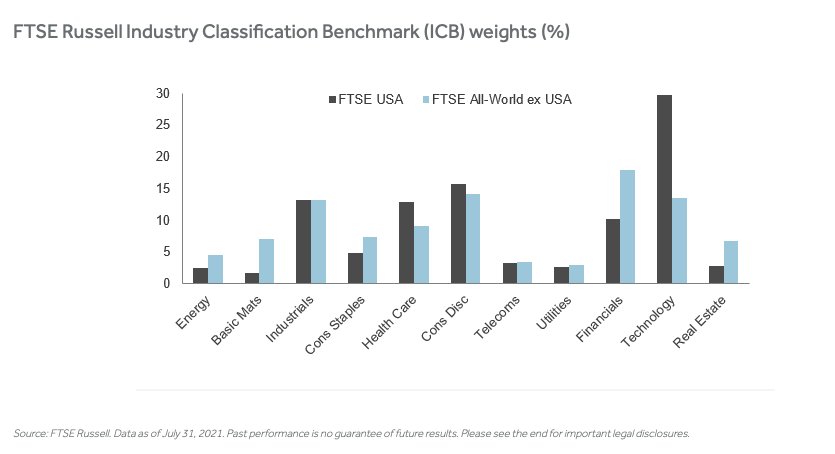

As the weights of the newly enhanced FTSE Russell Industry Classification Benchmarks (ICB) below show, the broad US market is more heavily skewed to the recent rebound in technology and health care stocks, and less so to lagging financials and energy, than overseas peers.

Conclusion

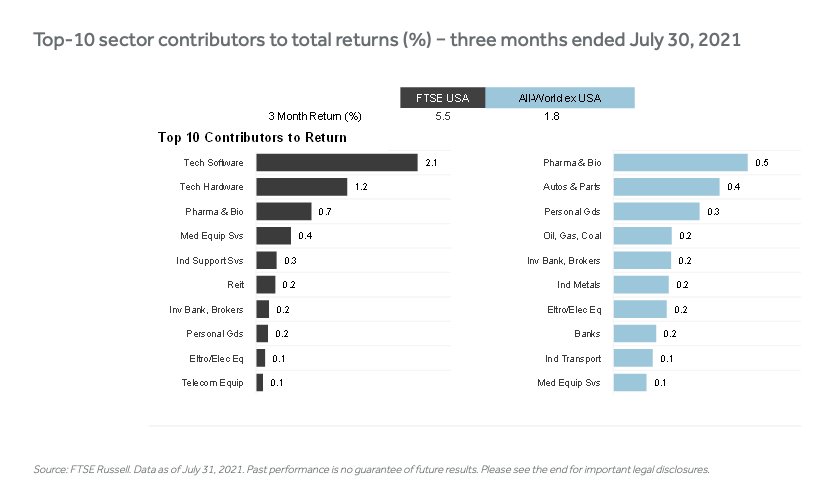

Further confirmation of this shift to growth can be found in the top-10 largest sector contributions to broad US returns for the three months ended July, which have been largely concentrated in the technology software/hardware, pharmaceutical, biotech and medical equipment stocks. These sectors accounted for roughly 80% of the total for that period. Contributions to the FTSE All-World ex USA returns were smaller and skewed to more cyclical sectors such as autos; oil, gas and coal; and industrial metals.

This post first appeared on August 4 on the FTSE Russell blog.

Photo Credit: thenails via Flickr Creative Commons

DISCLOSURE

The Russell 1000 Index is a stock market index that tracks the highest-ranking 1,000 stocks in the Russell 3000 Index, which represent about 90% of the total market capitalization of that index. The FTSE Europe ex UK and FTSE UK Index are one of a range of indices designed to help European investors benchmark their international investments, while the FTSE Asia Pac ex Japan and FTSE Japan cover the Asia Pacific Region. The FTSE Emerging Index provides investors with a comprehensive means of measuring the performance of the most liquid large- and mid-cap companies in the emerging markets. Investors can’t invest directly in indexes.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable.

Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put.

Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

{kind=link}

{kind=link}

{kind=link}