By Maxwell Gold, CFA, Head of Gold Strategy, and Diego Andrade Senior Gold Strategist

A lot can change in a year. As global economies begin to reopen in response to wider vaccine distribution, risk assets continue to take center stage among many investor discussions. However, amid this continued bullish sentiment lies a backdrop of certain rising risks — namely, stretched equity market valuations and bond yields remaining below inflation, which have created a potential asymmetrical return profile.

These factors emphasize the importance of diversification, a trait that gold — the original liquid alternative — has historically provided. Gold is one of the oldest financial instruments, dating back thousands of years, and may offer unique risk mitigation and diversification characteristics for portfolios compared to other liquid alternatives.

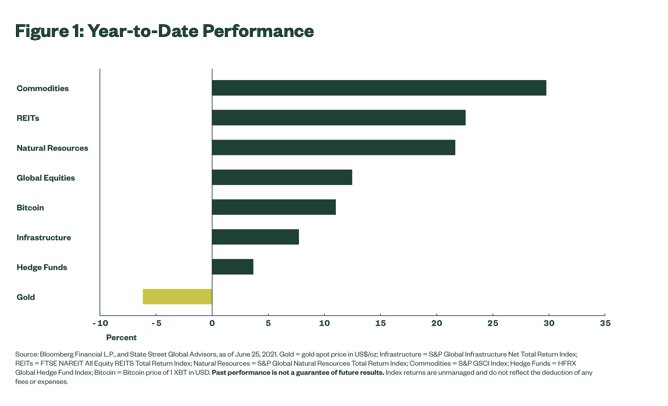

Following a strong 2020, with gold reaching an all-time high of US$2,067/oz last summer, gold performance has remained subdued year to date, as shown below. Some have claimed that other liquid alternatives which have outperformed recently, or even cryptocurrencies such as Bitcoin, should replace gold’s role in portfolios as the preferred diversifier and potential portfolio hedge.

Adding liquid alternative asset classes such as real estate investment trusts (REITs), natural resources, global infrastructure, liquid hedge strategies or broad commodities may potentially help investors mitigate risk in a traditional 60/40 portfolio. But gold, the original liquid alternative, has historically shown it may serve portfolios more effectively.

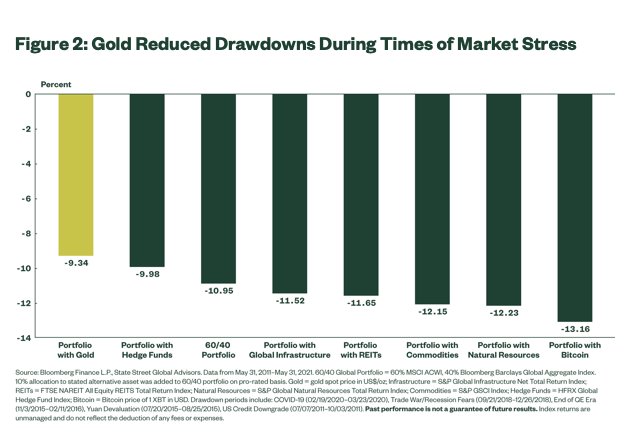

Protecting Portfolios During Tail Events

In a fervent bull market, like the one we find ourselves in now, mitigating risk may not be front of mind. Yet, it remains incredibly important. More so now given the asymmetrical return profile for stocks and bonds that features less of a fundamental backstop (high valuations, low yields) if a correction does occur, even though the reopening of economies will continue to be the driver of growth in the near term.

This aspect of persistent downside risk mitigation is on display in the chart below, illustrating that each time equities dropped more than 10% over the last decade, a 10% portfolio allocation to gold would have reduced portfolio drawdowns by 161 basis points (bps) on average compared to a traditional 60/40 portfolio, while the same allocation to most other liquid alternatives would have had the opposite effect — increasing average drawdowns.

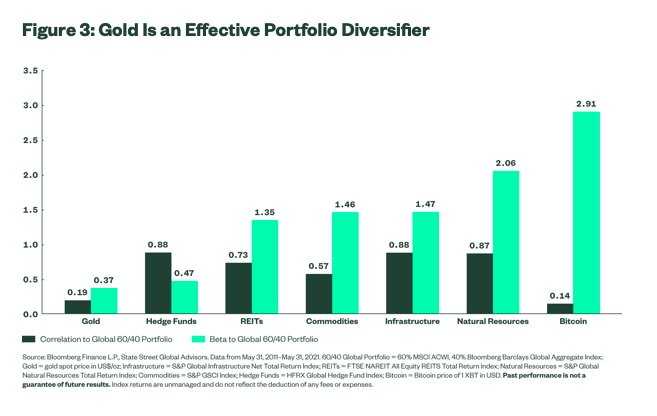

A True Alternative to Risk Assets

Gold has not only exhibited a low correlation to global stock/bond portfolios, but exhibited a low beta as well. While correlation showcases directional tendencies in movement of two assets, beta attempts to measure the explanatory power and quantify possible cause and effect.

Gold’s performance is explained by more than just the vicissitudes of global equity and debt markets. Gold is driven by its own market’s fundamentals — gold demand in the form of jewelry, technology, central banks, and investment along with changes in gold supply globally. Compared to gold, other liquid alternatives and Bitcoin have higher betas to global stock/bond portfolios; this shows that their performance is determined by these markets. This may result in a less effective source of portfolio diversification.

To read this article in its entirety, please click here and visit the State Street Global Advisors blog.

Photo Credit: K.Hurley via Flickr Creative Commons

DISCLOSURE

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Commodities and commodity-index linked securities may be affected by changes in overall market movements, changes in interest rates, and other factors such as weather, disease, embargoes, or political and regulatory developments, as well as trading activity of speculators and arbitrageurs in the underlying commodities.

Investing in commodities entails significant risk and is not appropriate for all investors.

Diversification does not ensure a profit or guarantee against loss.