By Andrew Little, Research Analyst, Global X ETFs

A bipartisan group of Senators seemingly struck a $1.2T U.S. infrastructure spending deal that has the support of the Biden Administration. The topic has dominated the national conversation in the U.S. since President Biden outlined the American Jobs Plan in March. With moderate Democrats in the Senate and President Biden wanting derivative legislation to pass with bipartisan support, those in Washington spent much the past three months negotiating a deal. Important to such a deal is the Senate’s 60% supermajority requirement to bypass the filibuster. Without 60 senators’ support, any legislation would effectively be dead on arrival absent budget reconciliation, which permits a simple majority but goes against the bipartisan wishes of moderate Democrats.

On June 24th, infrastructure negotiations yielded a fruitful result. President Biden announced his approval of a bipartisan infrastructure deal struck across the aisle in the Senate.

WHAT DOES THE DEAL LOOK LIKE?

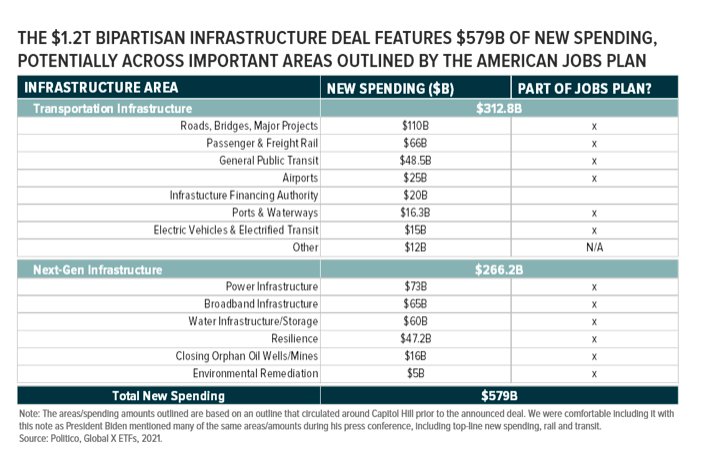

While the specifics of the deal have yet to be fully articulated, the details announced so far (as of June 25th, 2021) match an outline that circulated in advance of the agreement. These include $1.2T of top-line spending, $579B of which would be new spending (different from repurposed/already-allocated dollars) across traditional and next-generation infrastructure areas.

Though the deal does deviate from the $2.3B of spending outlined in Jobs Plan in terms of how much and on what, many exclusions seem to be tangential to physical infrastructure. Some are more in-line with President Biden’s social infrastructure agenda, including $400B for in-home care, $213B for affordable housing, and almost $150B for education/child-care. Other exclusions may already be covered by legislation the Senate passed in recent months, including The U.S. Innovation and Competition Act, which would allocate $250B for manufacturing and innovation, and The Drinking Water and Wastewater Infrastructure Act, which seeks to invest $35B in water infrastructure. All this said, it is important to note that the outlined $579B of new spending is not final and that there isn’t much clarity around the repurposed/already-allocated portion of the top-line $1.2T. Further, the above-mentioned legislation still must pass through the House and receive Biden’s signature. It is also possible that those behind the bipartisan deal intend on wrapping these bills into their final package.

WHAT’S FLESHED OUT & WHAT IS STILL UNDERWAY?

The exact details of the deal have yet to be articulated, as noted. What seems certain is that the deal includes $1.2T of total spending and $579B of new spending. And while the above-mentioned outline of where new spending could be directed seems to align with the announcement of the deal, there are mixed communications on its finality. Prior to President Biden’s approval, Senator Bill Cassidy (R-LA) noted “we have a framework and we are going to the White House,” while Senator Rob Portman (R-OH) stated “we’re very, very close [to a framework].”1

It also appears as if there is a general agreement on how the new spending will be funded. A primary sticking point to the Jobs Plan was Republicans’ unwillingness to fund infrastructure spending by raising taxes. With a deal secured, it appears as if Republicans’ qualms were addressed. Just hours after President Biden’s announcement, Senator Romney (R-Utah) tweeted, “we’ve reached a deal on an infrastructure package that focuses on physical infrastructure—roads, bridges, airports—without raising taxes or adding to the deficit.”2

How could the public sector raise $579B without raising taxes? An outline of financing sources also circulated last week and includes, but is not limited to:3

- State & local investment in broadband

- Allowing states to sell unused toll credits

- Auctioning portions of the 5G spectrum and using proceeds

- Selling strategic petroleum reserves

- Improving IRS tax collection abilities

- Public private partnerships, direct pay bonds, private activity bonds

- Improving unemployment insurance program integrity

- The positive economic impact of infrastructure development

HOW COULD THIS GET PASSED INTO LAW?

President Biden explicitly noted that while he approves of the Senate’s bipartisan infrastructure deal, he will only sign it into law in tandem with social infrastructure legislation. For reference, the White House followed the American Jobs Plan announcement with the American Families Plan, which outlines $1.8T of spending on social infrastructure.

Much of what was in the Jobs Plan, but was excluded from the bipartisan deal, overlaps with the spending areas mentioned in the Families Plan. And different than on infrastructure legislation, President Biden is in favor of using budget reconciliation to pass legislation derived from the Families Plan. This could allow Democrats to roughly cover the Families Plan and what was excluded from the Jobs Plan, though moderate Democrats might oppose reconciliation and Republicans could renege on their support of the bipartisan infrastructure deal. At the same time though, liberal Democrats in the House and Senate are noting dissatisfaction with the compromises made in the bipartisan infrastructure deal. It is possible they may not vote in favor of it without a separate social infrastructure reconciliation bill.

In our view, the bipartisan infrastructure deal will pass through the Senate and House with the necessary supermajority. As a part of this, we expect a slightly pared-down social infrastructure bill will also pass through Congress via budget reconciliation. We do not think moderate Democrats will oppose this – just this week, key moderate Joe Manchin (D-W.Va) indicated his support for such reconciliation.4 We also believe that Republicans backing the deal negotiated with this in mind and will continue to support their infrastructure legislation if concessions are made on social infrastructure prior to reconciliation. And if this is not the case, we expect Democrats to pass dual legislation through reconciliation, with moderates conceding after having given bipartisanship a try.

WHEN COULD THIS GET PASSED INTO LAW?

Regarding a possible timeline, we expect the Senate to draft legislation for the bipartisan infrastructure deal through the July 4th recess, allowing them to move it over to the House in early- to mid-July. Democrats would then have to draft and vote on a budget resolution, a preceding procedural step for reconciliation bills, prior to the August recess, during which they would draft a social infrastructure budget reconciliation bill. Following that recess, and through the end of the year, we expect the Senate and House to pass both bills and for President Biden to sign them into law before the end of the year.

CONCLUSION

President Biden’s approval of the bipartisan infrastructure deal is the closest the U.S. has come to sweeping infrastructure spending in recent history. If passed into law, the deal would represent the largest infrastructure package ever enacted in the United States. In our view, such spending will translate to revenues for companies involved in infrastructure development and that derive a significant share of their revenues from the U.S. (for example, see Four Companies That Could Help Develop Infrastructure in the United States).

This article first appeared on June 25 on the Global X blog.

Photo Credit: Tatiana Vdb via Flickr Creative Commons

FOOTNOTES

1. WFSB, “Senators say deal reached on infrastructure proposal as bipartisan agenda faces make-or-break moment,” June 24, 2021.

2. Twitter, @SenatorRomney, June 24, 2021, 3:12PM.

3. Capitol Hill, “Proposed Financing Sources for New Investment,” viewed June 24, 2021.

4. NBC, “Manchin open to Biden’s ‘human infrastructure’ plans and undoing some Trump tax cuts,” June 22, 2021.

DISCLOSURE

Investing involves risk, including the possible loss of principal. Narrowly focused investments typically exhibit higher volatility. Investments in infrastructure-related companies have greater exposure to the potential adverse economic, regulatory, political and other changes affecting such entities. Investment in infrastructure-related companies are subject to various risks including governmental regulations, high interest costs associated with capital construction programs, costs associated with compliance and changes in environmental regulation, economic slowdown and excess capacity, competition from other providers of services and other factors. PAVE is non-diversified.

This information contains a manager’s opinion, is not intended to be individual or personalized investment or tax advice, and should not be used for trading purposes.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

Carefully consider the fund’s investment objectives, risks, and charges and expenses. This and other information can be found in the fund’s full or summary prospectuses, which may be obtained at globalxetfs.com. Please read the prospectus carefully before investing.

{kind=link}