By Brian Manby, Senior Analyst, Research

As the first quarter comes to a close, there has already been a lifetime full of headlines in financial markets. From Bitcoin to GameStop to rising bond yields, there’s no shortage of market fairy tales, but the renaissance in global small caps and value stocks looks to be more of an enduring fact than fantasy.

Small caps have dominated to start the year, and value investing is finally gaining momentum. February was the best month for U.S. value relative to growth since the technology bubble in the early 2000s, outperforming by nearly 6%.

While small caps and value stocks have benefitted from a changing paradigm in the U.S., developed market small-cap value stocks have not been left behind either.

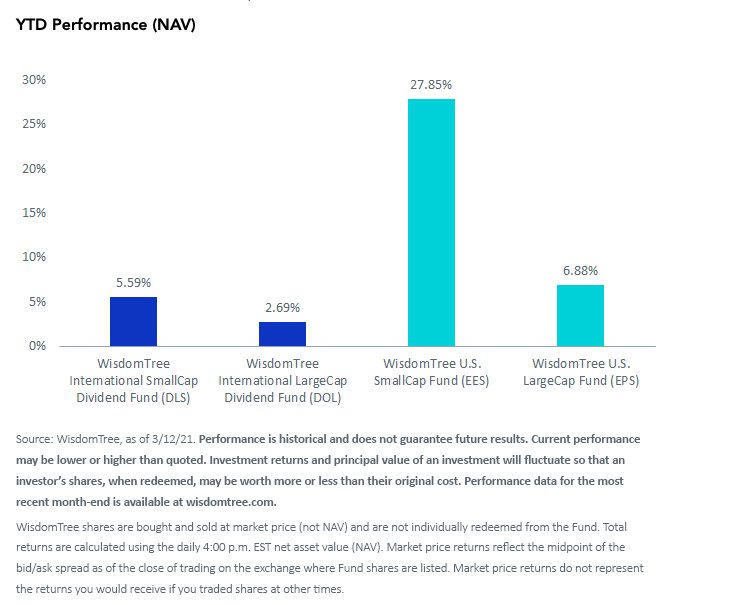

Take a look at the following chart, which relates the year-to-date performance of WisdomTree’s value-focused strategies in the U.S. and developed regions.

Please click the Fund’s respective ticker for standardized performance: DLS, DOL, EES, EPS.

While the magnitude of outperformance has certainly been more pronounced in the U.S., developed small-cap value has doubled the performance of its large-cap counterpart as well.

We think this is emblematic of a changing paradigm and a new beginning for the downtrodden size and value factors.

Sector Catalysts

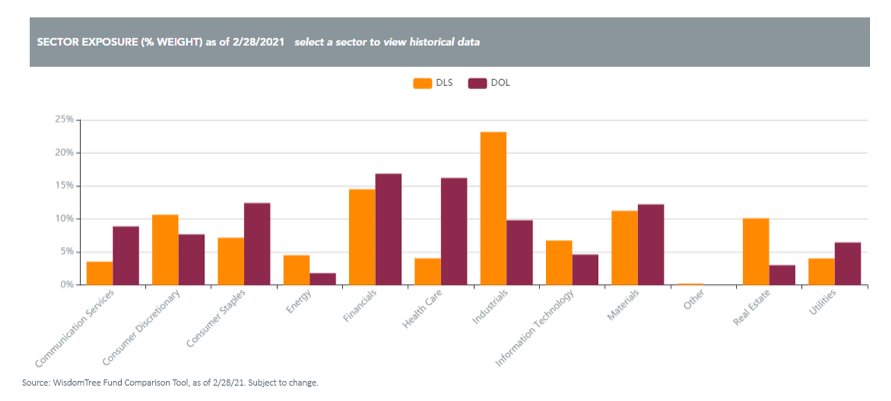

We think sector composition tendencies have been especially helpful in fueling the recent rally in small-cap value, especially in an economic environment that gives cyclical sectors plenty of runway.

Many investment strategists anticipate a revival in economic growth in 2021, commensurate with the reopening of global economies, the COVID-19 vaccine distribution and a resurgence in consumer activity. Those trends may set up traditional value sectors, such as Industrials, Energy, Financials and Real Estate, for lasting success—key exposures in WisdomTree’s International SmallCap Dividend Fund (DLS) and relative over-weights compared to its large-cap counterpart (DOL, the WisdomTree International LargeCap Dividend Fund).

Most notable is the 10% overweight in Industrials, which signals two potentially beneficial characteristics about DLS in today’s market environment.

First is the relationship between a revival in economic activity and how that would benefit sectors that are levered to this activity. Industrials, by definition, may be best positioned for an industrial comeback.

The Yield Appeal

Second is the propensity for dividends in developed markets. Value investing and dividend payments are practically synonymous. After many European companies suspended their dividends last year during the throes of the pandemic, their resumption may be additive for a value rally that already seems to have caught a tailwind.

But one common fear when investing in smaller companies relative to larger ones is the sacrifice in dividend yield, particularly in the U.S.

We concede there is some merit there. After all, smaller companies may be at a disadvantage compared to larger companies, which have more robust operations, stronger balance sheets and enduring profitability. Naturally, larger companies may have more flexibility to create value for shareholders via dividend payments, resulting in more attractive yields.

However, while small-cap investing currently requires a dividend yield sacrifice in the U.S., it can reward with a yield pickup in developed markets.

The yield on DLS is about 30 basis points higher than DOL as of the end of February. Compare that to the U.S., where larger companies (proxied by EPS, the WisdomTree U.S. LargeCap Fund) eclipse the yield of smaller ones (proxied by EES, the WisdomTree U.S. SmallCap Fund), and suddenly there’s an even more compelling case for size investing abroad.

Lower Ratios, Greater Appeal

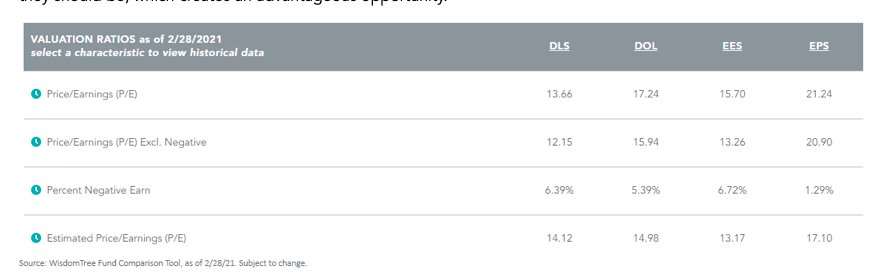

We’d be remiss to ignore the valuation profile of international small-cap value as well. Despite the attention they’ve earned this year, coupled with an impressive performance record, small-cap value stocks around the world still trade at comfortable discounts to their large-cap peers. That tells us that investors are not yet as serious about small caps as they should be, which creates an advantageous opportunity.

Despite their rally to begin the year, both U.S. and developed small-cap value stocks are trading at a 20%–25% discount to large caps on a price-to-earnings (P/E) ratio basis. Similarly, there are even discounts available in forward P/E measurements.

Even with their auspicious start to the year, international small caps are still lagging U.S. small caps, so the inexpensive valuations of the former should reassure you that they may still have room to rally further without fear of overpaying.

A Changing Paradigm

In the current market environment, we believe the tables are turning in favor of small caps and value investing as the economy continues to recover.

We’ve made the case before for small-cap investing in the U.S., and we believe now more than ever it’s just as important to consider small-cap allocations abroad. There may be rewards that the rest of the market has not discovered just yet.

This article first appeared on April 6 on the WisdomTree blog.

Photo Credit: William Warby via Flickr Creative Commons

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)