By Steve Sosnick, Chief Strategist at Interactive Brokers

There are few things that investors fear more than inflation. For many, this is an abstract fear, since few equity investors have seen a period of sustained inflation during their investing careers, but it remains an existential concern nonetheless.

Inflation erodes the prices of most financial assets, and investors dislike anything that erodes their assets. With the Federal Reserve actively seeking an inflation level of about 2%, and commodity prices rebounding – including some like copper and lumber approaching multi-year highs – this a concern that investors must address.

Bond Prices

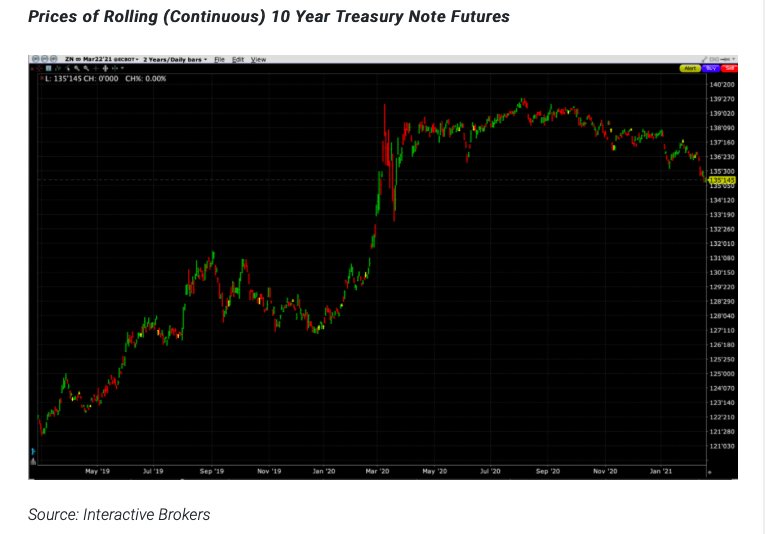

The 10-year Treasury note is perhaps the best indicator of the market’s inflationary fears. After a startling run-up in price (remember that bond yields are the inverse of bond prices), we can see that the rally has begun to fade.

We can see from the chart below that even though bond prices have dipped, they are still well above pre-Covid levels. One might look at the chart below and wonder what the fuss is all about.

Inflation Omens

As I write this, the 10-year yield is about 1.34%. By any historical standards that is not a worrisome level. Yet it was enough for Christine Lagarde, the President of the European Central Bank (ECB) to state that the ECB was “closely monitoring” sovereign bond yields. The rise in US Treasury yields was putting pressure on yield in Europe – apparently enough to justify a statement from the Continent’s main central banker. Our 10-year notes rallied in response, having recouped much of the decline that had pushed rates to nearly 1.40% this morning.

It is important to remember why bond prices reflect inflationary fears. It is typical to see longer term bonds trade with higher prices than their shorter-term counterparts. There are a few reasons for this. First, is a liquidity preference. Investors are willing to accept lower yields for instant access to their money. This is how banks can offer such low interest rates on checking accounts.

Another is credit risk. Less can go wrong for a company if there is less time until a bond matures. Of course this is not a major concern for Treasury investors, since the US government is typically seen as the best credit available. The final reason, and the one most relevant here, is inflationary expectations. If bond investors view their future payments as being rendered less valuable because of inflation during the ensuing years, they will demand higher interest to compensate for those inflationary expectations. That is what we are beginning to see in the bond market now.

Fed Policy

The Fed’s desire to see higher inflation, along with guidance that they will be reluctant to tighten monetary conditions until they see the Consumer Price Index persisting above 2% has led investors to be concerned that inflation could follow.

I was quoted in last weekend’s Barron’s about this: “The Federal Reserve has told us that they are not raising rates until they see the whites of inflation’s eyes.” I paraphrased a famous quote from the Battle of Bunker Hill, when revolutionary soldiers were given orders to hold their fire until the British soldiers were close, and I think it sums up the Fed’s thinking about inflation. They have stated numerous times that they have no intention of reversing their extraordinary monetary accommodation until they have seen repeated data that shows inflation has arrived.

Why the worry, then? If the Fed wants inflation and the economy is delivering what it wants, why should investors care? The problem is that once inflation creeps into an economy, it is hard to control. The most common way to control inflation is to tighten monetary policy. Asset prices have been soaring thanks to monetary and fiscal stimuli. Any reversal in that trend is perilous for asset prices.

Takeaway

As of now, that is a serious, but second-order fear. In the ensuing weeks we are likely to get another round of fiscal stimulus. There are negotiations that may reduce the size from $1.9 trillion, but it is likely to be quite sizable nonetheless. The current fear is that the new round of monetary stimulus is likely to arrive just as the economy is rebounding from Covid. That could cause the economy to overheat, with inflation as the result.

Worrisome inflation is not here yet, but markets try to discount future events. The market has already largely discounted the arrival of a significant stimulus package, now it is trying to discount its after-effects. And it’s not clear that the market enjoys those potential after-effects.

This post first appeared on February 22 at Traders’ Insight.

Photo Credit: Zooey via Flickr Creative Commons

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

DISCLOSURE: FUTURES TRADING

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

{kind=link}