By Anqi Dong, Senior Research Strategist, CFA, CAIA

The high efficacy rate and fast approval and deployment of COVID-19 vaccines have boosted hope for a quicker-than-expected return to normal. Although the recent resurgence of new cases posts near-term challenges, we believe the global recovery is still on track for next year. In our 2021 outlook , we formed the idea of a barbelled equity portfolio – with cyclical exposures that may benefit the most from the recovery and long-term secular growth positions aimed at capturing the evolutionary impacts of the pandemic and policy pivots. In addition to the broad innovation exposure and specific banking and clean energy industries highlighted in our 2021 outlook, we see three sector opportunities that may either benefit from the cyclical recovery next year or show strong secular growth potential over the longer term.

Travel smart and drive climate changes

During the recent virtual gathering of world leaders to celebrate the fifth anniversary of the Paris Agreement, President-elect Joe Biden reiterated his campaign pledge to rejoin the agreement on the first day of his presidency and cut US emissions to net zero “no later than 2050.”1 The goal of net zero emissions by 2050 cannot be reached without tackling the largest and fastest growing source of greenhouse gas emissions – transportation.2

Earlier this year, the Trump administration finalized the Safer Affordable Fuel-Efficient Vehicles Rule, which will increase CO2 emission standards for the automakers by 1.5% a year through model year 2026, a significant reduction from the 5% annual increase in place during the Obama administration. Biden’s administration may reraise the standard and develop rigorous new vehicle emission standards to drive innovation and the adoption of clean vehicle technology. Biden could also increase demand of electric vehicles (EVs) by increasing the share of EVs in the federal fleet.

Less than 1% of the 645,000 vehicles used by the federal government are electric vehicles.3 By prioritizing EV purchases and pursuing the goal of 100% zero-emissions vehicles set in Biden’s campaign, the government may boost the demand of EVs in the coming years. Furthermore, Democratic legislators have discussed increasing the EV tax credit quota from 1.9 million cars to 7.5 million cars – adding $39 billion to the cost of the credit — as well as expanding EV charging stations nationwide, which, if enacted, will make EVs more cost-competitive and accessible to consumers.4

While sales of passenger cars contracted earlier this year due to the pandemic, the International Energy Agency expects EV sales to remain close to 2019 levels and set a new market share record in 2020, thanks to government and policy support.5 Governments globally have implemented stimulus programs this year to support the auto industry, with a focus on electric vehicles. Germany, France, Italy and Spain are providing incentives or subsidies for the purchase of EVs. China has extended its subsidy program for EVs to 2022. EV sales in Europe in the first four months of 2020 reached more than 145,000, about 90% higher than the same period last year, as the European Union phased in the new target of CO2 emission standard for new cars by reducing the emissions by 27% from the previous standard.6 With the US rejoining global efforts to reduce CO2 emissions from transportation, the growth trajectory of EV sales could be amplified further in the coming years.

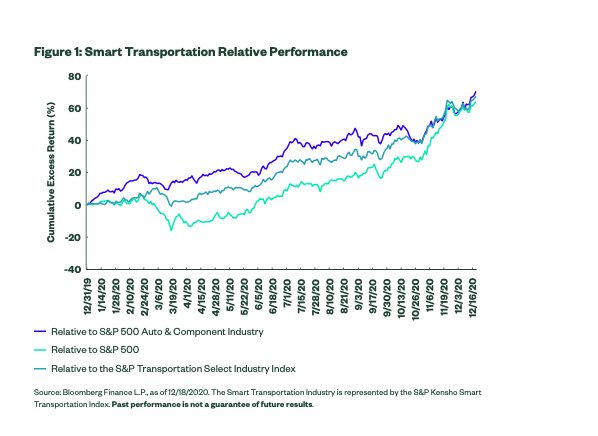

In anticipation of increasing demand for EVs, driven by policy support and emerging trends in autonomous vehicles and drone delivery services – highlighted in last quarter’s spotting trends blog – the market has shown enthusiasm for the smart transportation industry, as represented by the S&P Kensho Smart Transportation Index. Year to date, the index has outperformed the broad market by 62%, with 40% of its outperformance registered since early November, as shown in the chart below.

Investors seeking a cost-effective tool to target long-term secular growth trends in electric vehicles and autonomous vehicles and drones may want to consider the SPDR S&P Kensho Smart Mobility ETF (HAIL), an exposure seeking to capture the entire ecosystem driving innovation in smart transportation.

Increasing metal demand from the traditional and New Economy

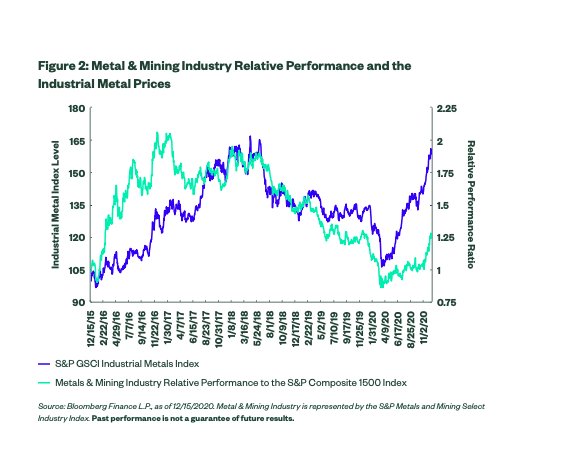

Metal markets have rallied since the market recovery, with industrial metals — such as steel, copper and aluminum — reaching their highest level since 2018,7 driven by increasing global demand. As manufacturing activities rebound from the pandemic-driven slump, metal producers and miners have ramped up production to meet surging domestic demand for cars, appliances and machinery. The stronger-and faster-than-expected recovery of the Chinese economy also fueled demand of base metals. Chinese fixed-asset investment, including capital spending on infrastructure, real estate, and machinery, continues to accelerate, growing 2.6% in the first 11 months of the year from the same period in 2019 – the third straight month of expansion.

The cyclical demand recovery has led to strong earnings sentiment and outperformance of the metal and mining industry lately. The industry EPS growth estimates for the upcoming quarter and 2021 have been revised from 31% to 59% and 134% to 171%, respectively, since the end of Q3. As shown in the chart below, the industry has outpaced the broader market by more than 30% quarter to date, moving along with the surge of metal prices. Rising inflation expectations and a weaker dollar may provide further tailwinds for the industry, as the industry has a higher beta to 10-year breakeven rates along with its deeper negative sensitivity to the dollar compared to the broader market.8

In addition to benefiting from the near-term cyclical recovery, the metal and mining industry may also benefit from increasing production of electric vehicles and investment in clean energy infrastructure in the coming years. Aluminum and advanced high-strength steels are two of the popular metal choices in EV manufacturing, thanks to their lightweight feature. Because copper is a highly efficient conduit for electricity and heat, there is 12 times more copper being used in renewable energy systems to generate power than in traditional energy systems.9 Higher energy efficiency standards in distribution transformers, electric motors and air conditioners – the three copper-intensive end markets – could increase the demand for copper across the three segments by 35% over the next 10 years.10 As the country shifts toward green energy, base metals may see a new round of demand growth. Investors seeking to capture the cyclical economic recovery in the near term and increasing demand of base metals from renewable energy over the medium term may want to consider an allocation to the SPDR Metals & Mining ETF (XME).

Seek to capture the recovery of consumer spending

US consumer spending has rebounded in Q2 thanks to the unprecedented fiscal stimulus programs that have supported household incomes. However, the recovery in consumption has not been even across sectors, with spending on durable goods 11% above its historical trendline and services spending 10% below.11 The gap in services spending points to more pent-up demand for next year.

As the vaccine becomes widely available to the general public and society gets on track to achieve herd immunity in 2021, lockdown measures will be lifted and life may gradually return to normal. Consumers are likely to increase their discretionary spending on restaurants, leisure, travel and bricks-and-mortar retail, which has been down significantly this year. Although increasing COVID-19 cases over the past two months have posed near-term challenges, as evidenced in the decline of retails sales in November, the impact could be temporary and may not derail the full recovery in personal consumption across all categories for next year.

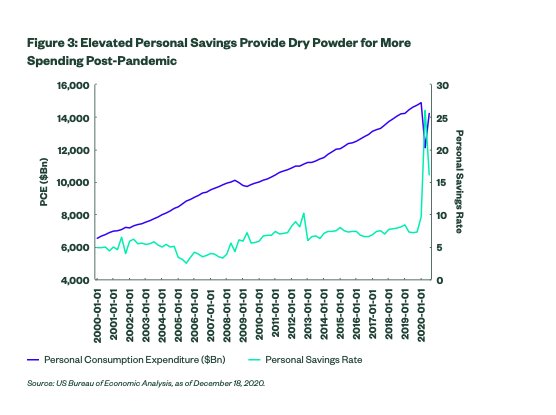

As shown in the chart below, the personal savings rate, which spiked to 33% over the summer, remained elevated at 13.6% in October and well above the long-term average of 7%, providing dry powder to fund pent-up demand after the pandemic. Household net worth broke records in Q2 and Q3. Household debt level as a percent of disposable income is at its lowest level since 1980. These are likely to support consumer confidence and bode well with the release of pent-up demand.

The positive economic backdrop has supported earnings sentiment in the Consumer Discretionary sector. The sector led earnings beats during Q3 earnings reporting, exceeding expectations by 55% with broad beats.12 Since the announcement of the first high-efficacy COVID-19 vaccine results, analysts have upgraded 2021 earnings growth estimates in the sector to 60% from 55% – the largest upgrades among all sectors.13

This article first appeared on the SPDR Blog on Jan. 4.

Photo Credit: Kevin Gill via Flickr Creative Commons

Footnotes

1 AP News, as leaders set fresh climate goals, Biden pledges US support, December 12, 2020

2 EPA, Sources of Greenhouse Gas Emissions, 2018

3 Government Accountability Office, Federal Vehicle Fleets Report, July 2019

4 Bloomberg Finance L.P., How Biden Can Get the US to Love Electric Cars, December 10, 2020

5 EIA, As the COVID-19 crisis hammers the auto industry, electric cars remain a bright spot

6 European Commission, Reducing CO2 emissions from passenger cars

7 Bloomberg Finance L.P., as of 12/15/2020

8 Bloomberg Finance L.P., as of 11/30/2020. Beta is calculated using monthly returns over the past five years ending 11/30/2020. S&P Metals & Mining Select Industry Index beta to 10-year breakeven rates is 0.59, compared to 0.32 for the S&P 500. Its beta to the Bloomberg Dollar Index is -2.78, compared to -1.05 for the S&P 500

9 Copper Development Association, Copper Alliance

10 Bloomberg Intelligence, as of 12/04/2020

11 US Bureau of Economic Analysis, as of 10/31/2020

12 FactSet, as of 12/18/2020.

13 FactSet, as of 12/18/2020.

14 FactSet, as of 12/18/2020.

Disclosures

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The discussion of any investments in this presentation is for illustrative purposes only and there is no assurance that the adviser will make any investments with the same or similar characteristics as any investments presented. The investments identified and described do not represent all of the investments purchased or sold for client accounts. The representative investments discussed were selected based on their similarity to indices shown. The reader should not assume that an investment identified was or will be profitable.

The S&P Kensho Smart Transportation Index is designed to measure the performance of companies focused on autonomous and electric vehicle technology, commercial drones, and advanced transportation systems in the Smart Transportation Sector. The S&P GSCI Industrial Metals Index provides investors with a reliable and publicly available benchmark for investment performance in the industrial metals market. S&P Select Industry Indices are designed to measure the performance of narrow GICS® sub-industries. The Index comprises stocks in the S&P Total Market Index that are classified in the GICS transportation sub-industry. The S&P Auto component index comprises constituents of the S&P500 that are classified as members of the transportation equipment sector as defined by the BSE industry classification system. One cannot invest directly in any of the indices mentioned in this post.

The views expressed in this material are the views of SPDR ETFs and SSGA Funds Research Team through the period ended December 28, 2020 and are subject to change based on market and other conditions and do not necessarily represent the views of State Street Global Advisors or any of its affiliates. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. The information provided does not constitute investment advice and it should not be relied on as such.

Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs.

Diversification does not ensure a profit or guarantee against loss.

Concentrated investments in a particular sector or industry tend to be more volatile than the overall market and increases risk that events negatively affecting such sectors or industries could reduce returns, potentially causing the value of the Fund’s shares to decrease.

Passively managed funds invest by sampling the Index, holding a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. This may cause the fund to experience tracking errors relative to performance of the Index.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions. Funds investing in a single sector may be subject to more volatility than funds investing in a diverse group of sectors.

Investing involves risk including the risk of loss of principal.