By Sergiy Lesyk, director, research and analysis, FTSE Russell

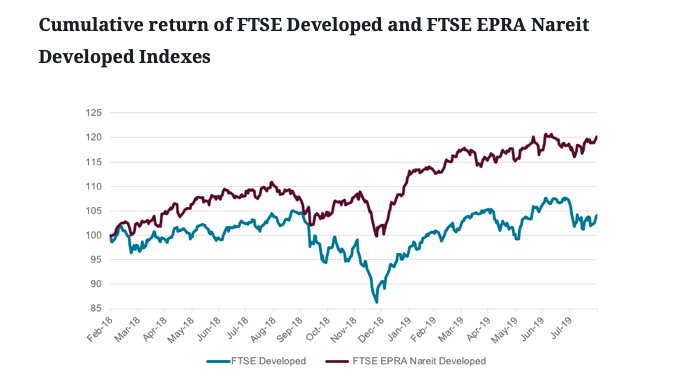

Since the start of 2018, we have noticed remarkable outperformance of real estate equities. In the last 18 months, the FTSE EPRA Nareit Developed Index has outperformed the aggregate equity index, the FTSE Developed Index, by around 15% (Chart 1).

Source: FTSE Russell as of August 29, 2019. Past performance is no guarantee of future results. Please see the end for important legal disclosures.

Several reasons have been cited to explain the difference in performance between real estate and global equity markets. This recent article from Invesco, lists some of them. The US-China trade war stimulated investors’ search for market segments, which were less exposed to its adverse consequences, like US domestic real estate. As tenants are locked in their lease agreement for several years, real estate provides a more stable and certain income stream, compared to sectors exposed to international trade. At the same time, the US unemployment rate, at a 50-year low, and low interest rates globally has provided a favorable macroeconomic backdrop.

Fed Pivot

Since Q4 2018, the Fed has pivoted away from the tightening monetary policy of 2015-18, a more dovish stance, and cutting interest rates as the US economy cooled. At the same time, escalating US-China trade war tensions added to stock market volatility. This resulted in investors allocating their assets into more defensive areas, such as fixed income, quality equity, infrastructure and listed real estate.

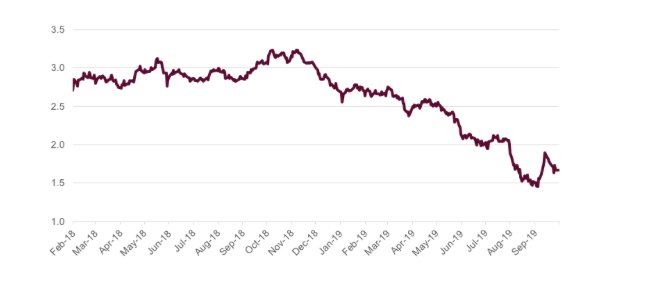

This defensive move had a dramatic effect on the 10-year US government bond yield, which halved from about 3% to 1.5% at the end of August 2019 (Chart 2).

Source: FTSE Russell as of August 29, 2019. Past performance is no guarantee of future results. Please see the end for important legal disclosures.

As the 10-year US Treasury yield declined and the rent expectations remained static, valuation of real estate stocks increased.

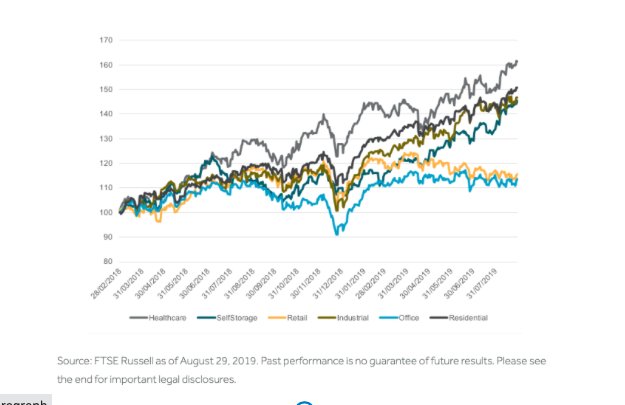

As Chart 3 demonstrates, the performance was not universal, however. Real estate is quite a diverse sector and the market is not indiscriminate, as seen by the wide dispersion of returns within the different segments. Less traditional areas, such as Healthcare and Self-storage, significantly outperformed traditional retail and office real estate, because of the structural challenges faced by retailing and the cyclical exposure of commercial real estate. Retail was weak as consumer shopping preferences continued to shift online, which in turn underpinned the good performance of the Industrial segment (includes warehousing for online retailers). The Residential, Self-storage and Healthcare segments did well on the back of high employment, moderate inflation, robust wage growth and strong consumer demand. Self-storage has been particularly volatile to the end of September, with its performance initially tracking that of Office, and then catching up with the Industrial segment.

Takeaway

For investors, the analysis and understanding of the drivers behind real estate performance are important in the context of future trends: listed real estate investors may want to think about whether to lock in their profits or keep the exposure.

For investors in direct property, this could be less relevant as the period of the recent strong performance is relatively short and it takes time to sell physical property (we elaborate more on this topic and other considerations of investing in real estate in our recent research note on our website.).

The FTSE Vietnam Index managed to almost stay flat in May, in stark contrast to other Asian equity indexes that were down almost 10% over the month.

Photo Credit: Shinya Suzuki via Flickr Creative Commons

This article first appeared on the FTSE Russell blog on July 25.

© 2019 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”).

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell indexes or research or the fitness or suitability of the FTSE Russell indexes or research for any particular purpose to which they might be put.

Any representation of historical data accessible through FTSE Russell indexes or research is provided for information purposes only and is not a reliable indicator of future performance. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

{kind=link}

{kind=link}

{kind=link}