By Robin Marshall, director, fixed income research at FTSE Russell

When US investment grade bonds are downgraded and cross the ratings threshold into high yield territory, they join the sector known as “fallen angels.” And while they’re technically categorized as high yield (HY) bonds, it’s important to note that fallen angels were initially issued as investment grade (IG) credits. This is why they tend to have distinct characteristics that set them apart from the rest of the US HY bond market.

A fallen angel (FA) is a corporate or sovereign bond downgraded from IG—a minimum rating of BBB- with S&P, Moody’s or Fitch—to a HY credit rating of BB+ or below. Fallen angels differ from other HY issues in numerous ways. Because they were issued as IG credits, when compared to HY bonds FAs tend to have longer duration, lower coupons, higher credit ratings, weaker covenants and lower default rates.

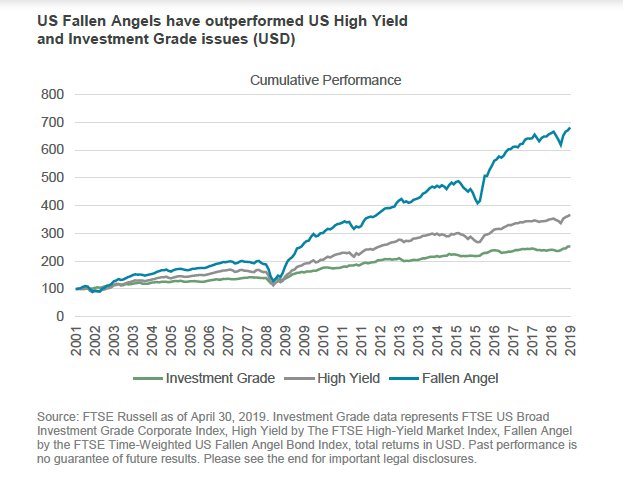

And generally speaking, they’re also more concentrated in sectors subject to specific shocks than HY issues. Fallen angels have also differed from HY issues with respect to performance. The FTSE Time-Weighted US Fallen Angel Bond Index (FABI) measures the performance of US and Canada-domiciled FAs after they enter the sub-IG asset class. As shown below, this index outperformed market cap weighted HY issues in the period 2002 – 2016.

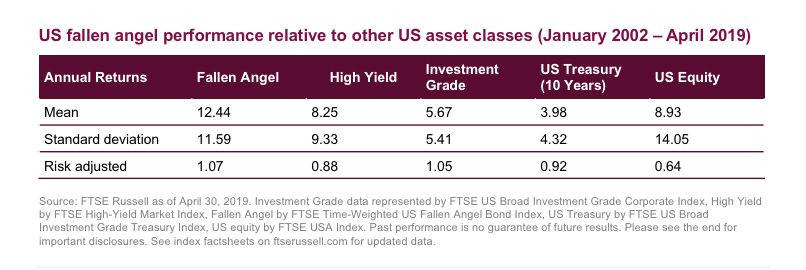

Since 2002, FAs have also posted higher returns on an annual basis relative to other fixed income classes, but with more volatility. The higher volatility can partly be explained by the time period immediately following the announcement of an FA’s downgrade from IG, where empirical evidence suggests it will see the sharpest drop in performance. As such, as shown below FAs have displayed higher standard deviation of returns than HYs. However, FAs still reported higher risk-adjusted returns for the period not only relative to HY, but also to US Treasuries and US equities.

What’s behind FAs’ outperformance? It can in large part be attributed to initial overselling, which drives FAs to artificially low prices relative to equivalent credits in the HY asset class. This can occur for several reasons. First, after the downgrade to sub-investment grade, indexed IG funds and other funds that aren’t permitted to hold sub-IG issues are forced to sell the FA.

The other two factors potentially driving the overselling of FAs relate more to behavioral finance. Institutional investors can overreact to the news of a downgrade, further causing the bond to suffer a “cliff-edge” effect on departure from the IG asset class. And in some cases, the selling can start even before the downgrade is announced. Given the distinct nature of IG and HY, even the risk of an issue leaving the IG universe can cause advance selling of the bond, because an active IG portfolio manager wants to avoid being caught with a sub-IG holding.

FAs’ unique characteristics can also be performance drivers. As noted earlier, FAs tend to have more duration than the rest of the HY asset class, since HY issuers may struggle to issue longer maturity bonds. This would have helped relative performance during the 2011-16 period, given very low interest rates and a benign credit environment.

Whether from overselling or as a result of their distinct characteristics, when studied as a separate asset class, FAs have historically exhibited higher risk-adjusted returns than HY issues. These performance differences demonstrate that while FAs join the ranks of HY bonds when they’re downgraded to speculative territory, many unique characteristics continue to set them apart.

Please see our recent paper for more details on what makes fallen angels unique. Receive a weekly blog recap from FTSE Russell

Photo Credit: Kiwi-Wings via Flickr Creative Commons

This article first appeared on the FTSE Russell blog on Sept. 27.

© 2019 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”).

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind.