This post was written with contributions from Anqi Dong, CFA, CAIA. Anqi is a Senior Research Strategist on the SPDR® Americas Research Team.

Reignited trade tensions, a potential no-deal Brexit, and signs of an economic slowdown are making markets jittery.

The second half of 2019 isn’t likely to calm down. Bouts of volatility and big market swings are still expected as investors try to make sense of an increasingly uncertain geopolitical landscape, while central banks may step in to try to calm markets with their accommodative policies.

Rather than moving to the sidelines, investors should focus on areas that are less likely to be impacted by the trade conflicts, adding more resilience to the portfolio in the form of downside protection.

Strategies to lower overall portfolio risk

Several tools are available to investors to mitigate risk throughout the portfolio.

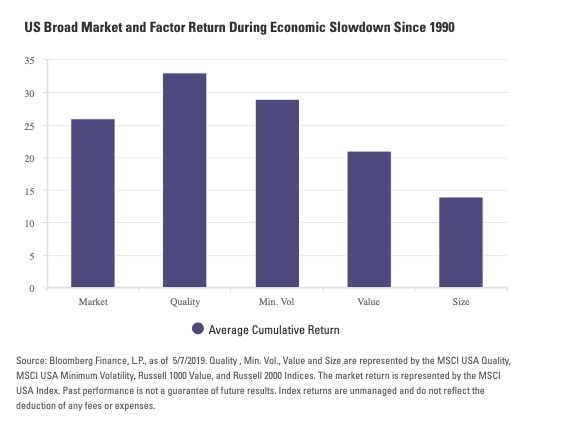

1. Equity strategies that provide upside participation but mitigate drawdownsAs shown in the chart below, low volatility and quality factors have historically performed well during economic slowdowns – defined by decelerating year-over-year growth of the Conference Board Leading Economic Indicator (LEI) Index. Since October last year, the LEI index growth has been on a downward trend, falling to 1.6% in June.

Quality has led factor performance this year, outperforming the broad market by 4.7%. Low volatility ranks at the top on a trailing 12-month basis, when the market experienced multiple drawdowns of more than 5%. As economic uncertainty persists, the two factors are likely to continue showing resilience. Targeting strategies that blend these factors together, resulting in a low volatility strategy that also has upside potential, may be ideal.

2. Let bonds be bonds

Continuing the themes discussed in our mid-year outlook, bond exposures can potentially offset equity risk within the portfolio. However, not all bonds are the same. Below investment grade credit has become highly correlated to equities.

The curve has flattened and long-term rates have fallen so dramatically that the yield per unit of duration is sub-optimal to more intermediate parts of the curve. Therefore, given the late-cycle dynamics in play, active and intermediate-duration bond strategies can offer the potential for increased income and return without uncompensated duration or equity-like risks.

3. Strike a defensive tone

Finally, gold typically performs well when volatility spikes. Gold has appreciated +6.7% on average during the last nine market downturns, while the S&P 500 has pulled back an average of -13.3%. That same trend has continued so far this year, as gold prices broke through the psychological 1,500/oz. barrier on the back of persistent geopolitical tensions and real interest rates turning negative. Gold has historically had a negative relationship to real rates. Both factors may continue to support gold prices.

The rate environment is unlikely to change, given the stance by multiple central banks to lower rates and turn policy overly accommodative to combat sluggish global growth concerns. Additionally, the geopolitical issues are unlikely to go away either given the uncertainty around trade, Brexit, and ongoing strife in the Middle East (e.g., Iran) and Asia (e.g., Hong Kong).

The turnings follow a familiar rhythm of growth, maturity, decay and — ultimately — destruction. It’s easy to connect them to the four seasons — spring, summer, fall and winter. When the book was published in 1997, Strauss and Howe were forecasting that winter was due to arrive early in the 21st century.

Followers of their work have cited such events as 9/11 and the Great Recession as evidence that the Fourth Turning was beginning as predicted. The massive national debt and increasing deficits have become symptoms of this crisis period.

For more, please read the rest of the post originally published on the SPDR Blog on August 15.

Photo Credit: Dennis Jarvis via Flickr Creative Commons

This material is from State Street Global Advisors and is being posted with State Street Global Advisors’ permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and are subject to change based on market and other conditions. Interactive Advisors is not endorsing or recommending any investment or trading discussed in the material.

The opinions expressed may differ from those with different investment philosophies. This material is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed or relied on as research or investment advice.

This information does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. This material is for informational purposes only and does not constitute investment or tax advice and should not be relied on as such. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation to buy, sell or hold such security.

This material does not and is not intended to take into account the particular financial conditions, strategies, tax status, investment horizon, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

This material may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. There will be no updates made to these forward-looking assessments.

![Marty Leclerc: Bonds no, Cisco and Dupont stock yes [Video]](/content/default.jpg)

{kind=link}