By Sandrine Soubeyran, director, research and analytics, FTSE Russell

One development that emerging market equity investors will be watching with interest this year will be the inclusion of China A Shares in FTSE Global and emerging market indexes.

During 2018, we evaluated the China A Share equity market against our Country Classification process and announced in September that China A Shares available via the Northbound Stock Connect program—the mainstream equity class in that country—would be included in our Global and Emerging Market Index.

As with all our country classification changes, we made this announcement well in advance of implementation to give market participants time to adjust.

China A Shares

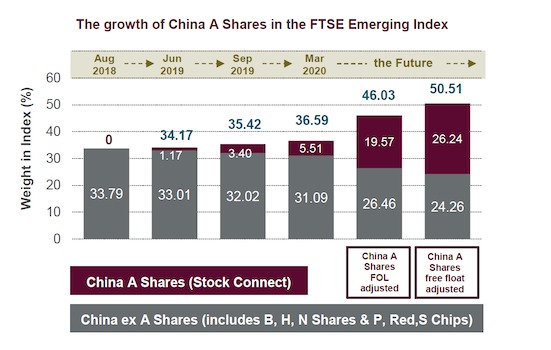

We will begin including China A Shares securities into FTSE GEIS from June 2019. To assist index trackers in their ability to efficiently replicate the underlying benchmark change, we will implement the inclusion over three separate tranches (Phase 1) through to March 2020.

After each tranche, FTSE Russell will seek market feedback on the efficiency of the implementation and to evaluate the ability of the market to absorb the additional assets before proceeding with the next tranche.

Stock inclusion will be calculated using 25% of investable market capitalization of the eligible large, mid and small cap designated securities from the FTSE China A Stock Connect All Cap Index (currently around 1,250 stocks).

As the chart below shows, upon completion of the Phase 1, China A Shares are expected to constitute c. 5.5% of the total FTSE Emerging Index, representing initial net passive inflows of $10 billion of assets under management.

Methodology

It’s vital to recognize that FTSE Russell formally reviews country classifications within its FTSE Global Equity Index Series (FTSE GEIS) using a comprehensive, transparent and consistent methodology, which verifies that important criteria for market efficiency and quality are met.

Ensuring that those investor conditions are achieved lies at the foundation of our country classification evaluation process. China A Shares classification as Secondary Emerging Market was a result of constructive engagement with Chinese regulators, stock market officials and international investors/custodians.

China’s Future

So considerations for further inclusion of further China A Shares after Phase 1 will take place within that framework: specific questions could include whether the size of the next phase should be based on any increase to the quota sizes, whether phase 1 should be repeated (i.e., taking the total inclusion factor to 50%); and whether stocks outside of Stock Connect routes should be included.

But this is unlikely to be the end of the process: in time, China’s listed equity markets are likely to dwarf the rest of the emerging markets.

According to our research, China shares could in time form half of all stocks in FTSE Emerging Markets, with A Shares, and ex A Shares (B, H, N, P, Red and S Chips) providing a quarter each.

But whatever happens will be determined using an agreed, transparent process, and asset owners and managers will be made aware of changes a long time in advance.

Photo Credit: Alfred Weidinger via Flickr Creative Commons

©2019 London Stock Exchange Group plc (LSEG Group). All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Any representation of historical data accessible through FTSE Russell Indexes is provided for information purposes only and is not a reliable indicator of future performance. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The author and its employer believe that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

![Moneyball – the trailer [VIDEO]](/content/default.jpg)

{kind=link}