By Sandrine Soubeyran, director, research and analytics, FTSE Russell

China’s equity markets are rapidly opening to global investors, not least as index providers begin increasing China exposure in their mainstream indexes.

But the People’s Republic of China’s enormous bond market is changing, too. It has already come a long way since the first bond in the market was issued in 1980.

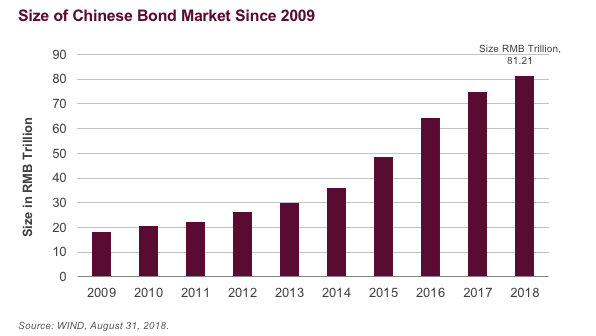

It now ranks as the third largest bond market in the world behind the United States and Japan, having quadrupled in size since 2009.

Bond Menu

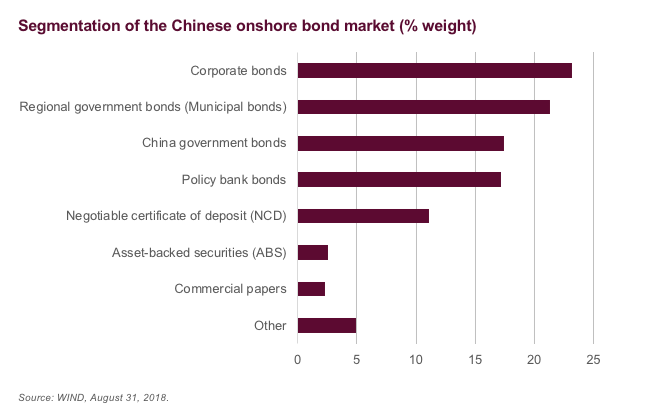

China’s domestic bond market is dominated by sovereign and regional government bonds with a growing credit sector.

Investors view policy bank bonds (non-commercial, 100% state-owned banks that lend in support of government priorities) as having similar risk as sovereign bonds.

Municipal bonds have been growing rapidly since 2015.

Onshore Market

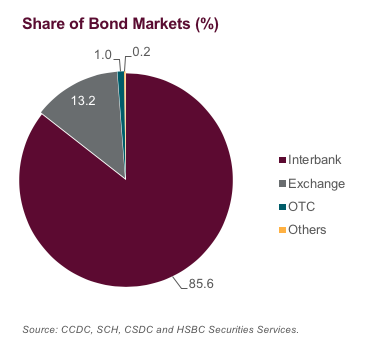

Chinese onshore bonds are mostly traded through the interbank bond market, which includes a wide range of financial institutions.

Much of the outstanding debt issuance has been tilted towards short maturities, with many issues due to mature in less than four years.

Sweeping changes

China’s onshore bond market has historically attracted domestic investors, but the balance has been slowly changing due to government efforts to attract a wider investor base.

China’s onshore bond market is quickly liberalizing through policy initiatives, including Qualified Foreign Institutional Investor (QFII) and Renminbi Qualified Foreign Institutional Investor (RQFII) schemes, which allow institutional investors who meet certain qualifications to invest in a limited scope of cross-border securities products.

Bond Connect

In July 2017, Bond Connect was launched, allowing investors from mainland China and overseas to trade in each other’s bond markets through connection between the related mainland and Hong Kong financial infrastructure institutions.

However, limitations have hampered access for international investors.

Sovereign credit risk has been difficult to assess given the potential large liabilities not reflected by the level of government debt and fiscal deficit.

Foreign Ratings

Also, there has not been any coverage of onshore CNY credit bonds by international rating agencies, which are in the process of getting a license.

International foreign ratings agencies were recently permitted to operate in China to rate domestic Chinese issuers, but at the time of writing, none had been granted a license. Prior to the change in the rules, global rating agencies could only hold minority stakes in joint-venture operations and not issue ratings on local bonds.

Default Rates

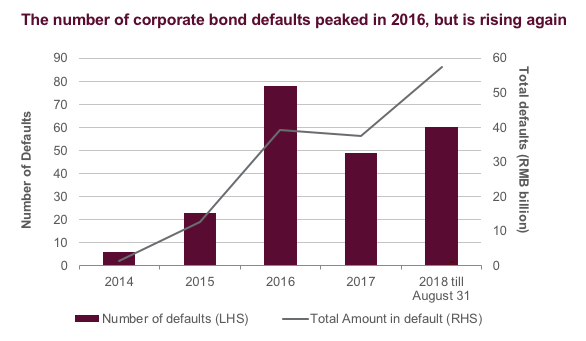

As the authorities continue to restrict off-balance sheet lending and push up funding costs, corporate bond defaults have risen six-fold since the end of 2015.

And 2016 saw the largest number of bond defaults (78), which represented RMB 39.3 billion in principal amount. In the first eight months in 2018, the issue sizes were significantly larger with 60 bond defaults representing RMB 57.38 billion in principal amount.

Nearly 20% of bond defaults have been by state-owned enterprises as regulators moved away from the old model of implicit guarantees for most debt securities to allow defaults to take place.

Photo Credit: A_Peach via Flickr Creative Commons

This article first appeared on the FTSE Russell blog on December 6, 2018.

© 2018 London Stock Exchange Group plc (LSEG Group). All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Any representation of historical data accessible through FTSE Russell Indexes is provided for information purposes only and is not a reliable indicator of future performance. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The author and its employer believe that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

{kind=link}