By Steven Levine, Senior Market Analyst, Interactive Brokers

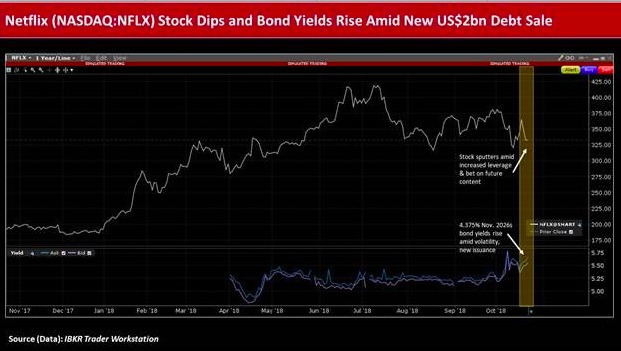

Streaming media giant Netflix (NFLX) announced a US $2 billion high yield bond sale on Oct. 22, as the company continues to build original content and grow its subscriber base.

Netflix took advantage of relative market calm to sell new euro- and U.S. dollar-denominated debt, with an aim to use the net proceeds for general corporate purposes, which may include content acquisitions, capital expenditures, investments, and working capital.

Netflix has said that its growing mix of self-produced content, which requires funding during the production phase, is “the primary driver of our working capital needs that creates the gap” between its positive net income and its free cash flow deficit.

In its the third quarter of 2018 earnings, the company said it recognizes it has been “making huge cash investments in content,” which it sees as “very likely to help us to keep our revenue and operating profits growing.”

Strong Earnings

Netflix had trounced market expectations in Q3 with earnings of US$0.89 per share compared to less than US$0.70 anticipated, while revenues were as-expected at US$4bn.

Furthermore, the company’s total net additions amounted to close to 7.0m – up 31% from a year ago – beating its own outlook for 5.0m.

Netflix had touted the subscriber gain as a new Q3 record. Meanwhile, the company maintains a negative free cash flow (FCF) position.

In Q3’2018, Netflix’s FCF was -US$859m compared to -US$465m in the same year-ago quarter, and the company said it thinks the level in 2019 will be roughly flat with the current year.

Betting on content

Against this backdrop, Moody’s Investors Service assigned a ‘Ba3’ junk-status credit rating to Netflix’s new senior unsecured note sale, noting that pro forma for the added debt, the firm’s gross leverage is set to rise to 6.2x for the last twelve months ended September 30, 2018.

Leverage had been 5.3x on a last quarter annualized (LQA) basis and 3.3x on a pro forma net leverage basis.

However, despite the continuing debt issuances used to fund the company’s negative cash flows, Moody’s analyst Neil Begley expressed optimism about the firm’s ability to continue growing its earnings and improve its credit profile.

Begley said he expects leverage to “drop gradually over time as the transition from licensed content to produced original content levels off and newer international markets begin to contribute to profits and overall margins improve.”

Content Spend

Moody’s anticipates that gross leverage will fall back to around 6.0x by the end of 2018 and below 5.0x by the end of 2020, as the company’s EBITDA growth outpaces the growth in content spend and in debt.

Begley added that he thinks Netflix is on a trajectory to “easily surpass 200 million subscribers by the end of 2021, and we believe that the company has the ability to reach cash flow break even within 5 years as they grow total margins to the low 20% range.”

Netflix, which boasts a global membership of more than 130m paid and 137m total subscribers, has been producing popular self-owned content such as Stranger Things via an in-house film and TV studio it constructed two years ago.

For Q4, Netflix said it expects a 15% rise in paid net additions of 7.6m, as well as a 13% spike in total net additions of 9.4m over with the previous year, and continues to target operating margin to reach the lower end of the 10%-11% range for the full year 2018.

Cash Flow

Netflix CFO David Wells said the company is “approaching a point where the growth in operating profit is going to grow faster than our growth in content cash spend.

And that’s really going to drive the free cash flow towards improvement. It’ll eventually break even.”

Wells added that “once we push past the point where we’re more secure,” then it will be “less about funding the immediate working capital needs of the business,” and the company will transition towards thinking about its long-term optimal cost of capital.

Netflix generally competes with other subscription on-demand video services (SVOD), including major traditional media companies such as Disney (DIS) and AT&T’s (T) WarnerMedia, which will likely pose growth hurdles as these services mature.

Photo Credit: Stock Catalog via Flickr Creative Commons

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR or IBKRAM to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The author believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.