By Steven Levine, Senior Market Analyst, Interactive Brokers

While the Federal Reserve hiked interest rates at its monetary policy meeting as expected, a host of event risks could impact the direction of further rate decisions.

The latest 25-basis point rate hike marks the eighth time the Fed lifted rates since it committed to a zero-bound interest rate policy about a decade ago – soon after the titanic failure of Lehman Brothers shook the global financial system.

Normalizing

Indeed, since the end of 2016, the FOMC has been on a path towards gradually normalizing monetary policy, amid a general upswing in the economy, underscored by what the Fed has highlighted as “strong” job gains, as well as strengthened growth in household spending and business fixed investment.

At its previous meeting in early August, the FOMC kept the target range for the fed funds rate at 1.75-2%, however, the market generally expects another rate hike at its meeting in December, followed by additional hikes at least through the first half of next year.

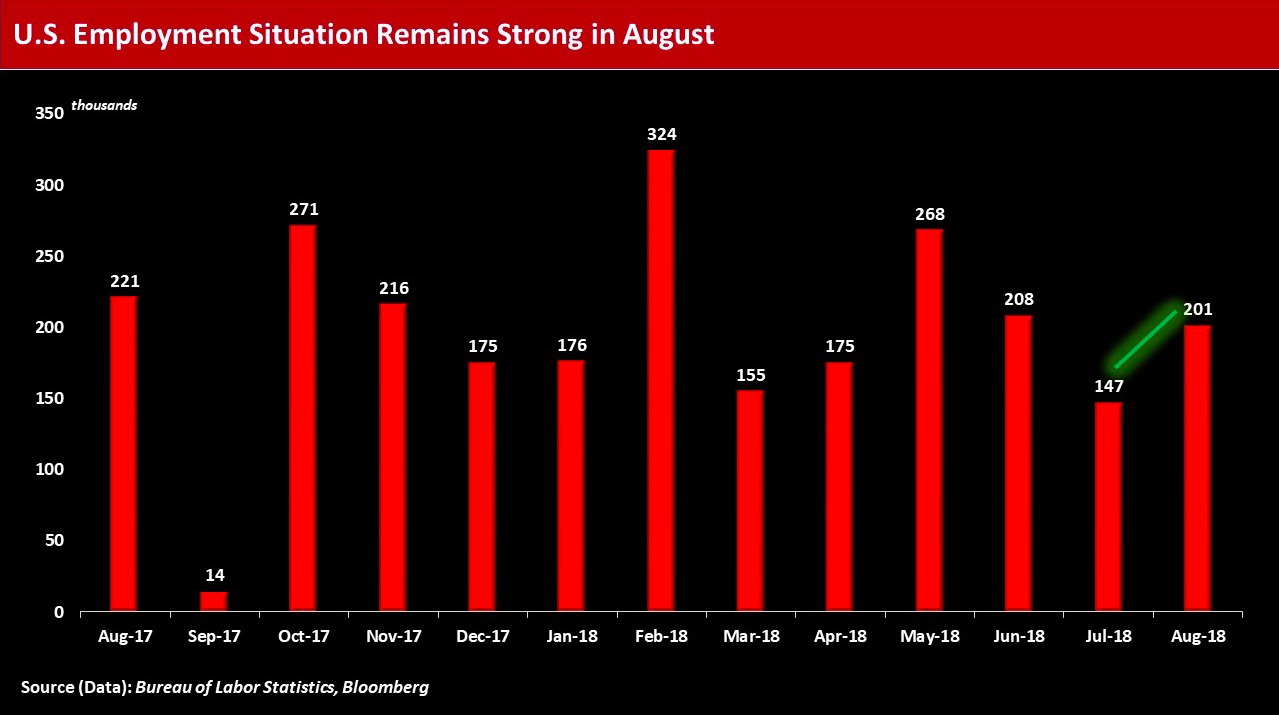

The expectations have been supported by rosy economic data, including a healthy labor market, with wage growth in August having risen for the first time in about eight months.

More Hikes

Jefferies chief financial economist Ward McCarthy recently noted he thinks the FOMC will raise the longer run fed funds rate – the so-called long run neutral rate – to 3% from 2.9%, which he said will likely be achieved by mid-year 2019.

Against this backdrop, McCarthy continued that “the next significant policy debate over the next twelve months will occur once neutrality has been achieved. At that point, doves will want to hold steady and hawks will want to continue to raise rates so long as the dual mandate objectives are still met.”

He added that the “most logical compromise, in our opinion, would be for the FOMC to slow the pace of gradual rate hikes but continue to raise rates above the current estimate of longer run neutrality, nonetheless.”

The ‘most logical’ scenario McCarthy outlines would suggest three rate hikes in 2019, as well as in 2020.

Yield Curve

While economic activity in the U.S. remains expansive, a myriad of potential event risks continues to derail the momentum, with the threat of yield curve inversion ever-present in the background.

Analysts have noted that when the yield curve inverts (when long-term rates fall below short-term rates), a recession typically ensues. This scenario has included the past two recessions, which occurred in 2001, as well as from 2007 to 2009.

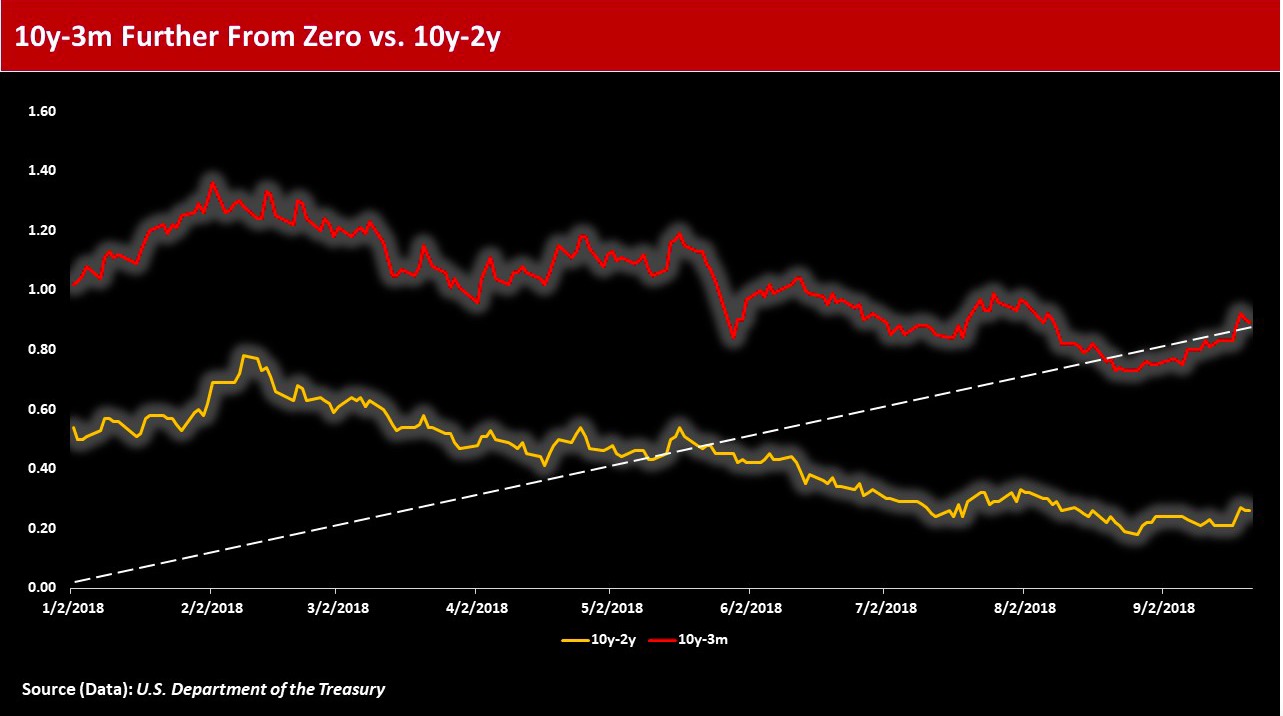

To date, market participants may view the prospect of a yield curve inversion as remote – especially as a recent rise in the yield on the 10-year U.S. Treasury note seems to support the case for an upward slope. The 10-year was last quoted at around 3.10% after recently reaching a 52-week high of almost 3.13%.

Also, for those market players using the difference between the 10-year and three-month (10y-3m) Treasury rates over the 10-year and 2-year note (10y-2y) term spread, the likelihood of an inversion appears much lower.

Eurodollar Futures

However, when surveilling three-month Eurodollar futures contracts, which reflect the cost in the future of borrowing money for 90-days, and are typically impacted by FOMC monetary policy decisions, the shape of the yield curve over one-year periods, at different junctures, shows a gradual flattening that ultimately slopes downward.

While the Dec-18 / Dec-19 spread is currently sloping upward by 49bps, for example, the curve gradually flattens, until the still-positive shape of the Dec-19 / Dec-20 spread at 3.5bps transitions – and the Mar-20 / Mar-21 contract ultimately marks the first so-called ‘calendar spread’ that is negative (at -1bp).

Political Shocks

There are numerous scenarios that could justify a flattening and potential inversion of the curve, including protracted flight-to-quality purchases stemming from domestic and global geopolitical volatilities.

Uncertainties over the outcome of special counsel Robert Mueller’s probe into alleged Russian interference in the 2016 presidential election, for example, could upend the stability of U.S. leadership and trigger flights to safer assets such as longer-dated U.S. Treasuries.

Other risks include UK Prime Minister Theresa May’s ability to successfully form a so-called Brexit agreement with the EU.

There’s also the threat of nuclear war resulting from reignited flare ups between the U.S. and North Korea, as well as the potential escalation of hostilities in the Middle East stemming from U.S.-imposed sanctions on Iranian oil, and whether the U.S. can form a treaty with Iran over its ballistic missile program.

Another trigger that could spur an economic collapse comes closer to home and may not be at the forefront of global concerns – namely the increasing burden of domestic household debt.

Analysts at McKinsey noted that broader measures of household financial wellness, beyond mortgages, “remain worrying.” They observed, for instance, that outstanding student loans now top US$1.4 trillion, exceeding credit card debt, and unlike nearly all other forms of debt, they cannot be discharged in bankruptcy.

Debt Bomb

The New York Fed recently cited figures from the Center for Microeconomic Data (CMD) that showed nearly 11% of aggregate student loan debt was 90+ delinquent or in default in the second quarter of 2018, a “small increase” from the prior year.

Meanwhile, tuition rates appear to keep rising, and state funding appears on average to be declining, spurring increasing numbers of students with low-to-no credit history into federal borrowing programs, or private debt markets.

According to the Employee Benefit Research Institute (EBRI), the median outstanding student loan balance increased from US$5,363 in 1992 to US$19,000 in 2016 – a 254% increase. The average student loan balance had a similar increase from 1992 to 2016 of US$11,751 to US$34,293 — 192% growth.

As tuition costs rise, and if wage growth remains relatively steady, default rates could well climb higher, denting droves of credit scores and causing limited, or no access to consumer credit.

This scenario would most likely result in far fewer purchases of homes, cars and other large-ticket items, as well as diminish prospects for small business formations – potentially leading to a deflationary environment that could reverse the current course of Fed tightening.

While student loans have been weighing on the potential future of economic growth, they are by no means the only form of borrowing that has been rising.

Fed Policy

Aside from the risks of geopolitical upheaval, as well as potential waves of student loan debt defaults, the Fed’s own program of quantitative easing (QE) could negatively impact the shape of the yield curve.

While researchers Michael Bauer and Thomas Mertens at the Federal Reserve Bank of San Francisco have argued that the recent flattening of the yield curve may not suggest an imminent inversion, they have warned about the potential effects of the Fed’s unprecedented stimulus measures.

Bauer and Mertens admit that uncertainty over the effects of QE on interest rates, as evident from certain statistical measures, is likely skewed to the downside because they assume a specific underlying model that is itself “highly uncertain.”

They also noted that “while a lower term premium contributes to easier financial conditions and therefore stimulates economic activity, this was also the case in the past and at times may have contributed to economic overheating, heightened financial stability risk, and ultimately higher recession risk. There is no clear evidence in the data that ‘this time is different’ or that forecasters should ignore part of the current yield curve flattening because of the presumed macro-financial effects of QE.”

Flip-side

The other side of the argument for a flattening, and potential inversion, of the yield curve necessarily include a reduction of event risks, changes in fiscal policy that enable students to better manage their debt, as well as successfully uncovering and mitigating any so-called ‘black swans’.

Analysts at Rareview Macro listed a slew of potential catalysts for higher-yields in the long-end of the yield curve, including a drop in the hefty volume of recent corporate bond issuance, a reduction in pension purchases since the September 15 tax deadline, an increase in global yields either stemming from interest rate hikes or moving to remove accommodation, as well as progress over Brexit and de-escalation on the Korean Peninsula.

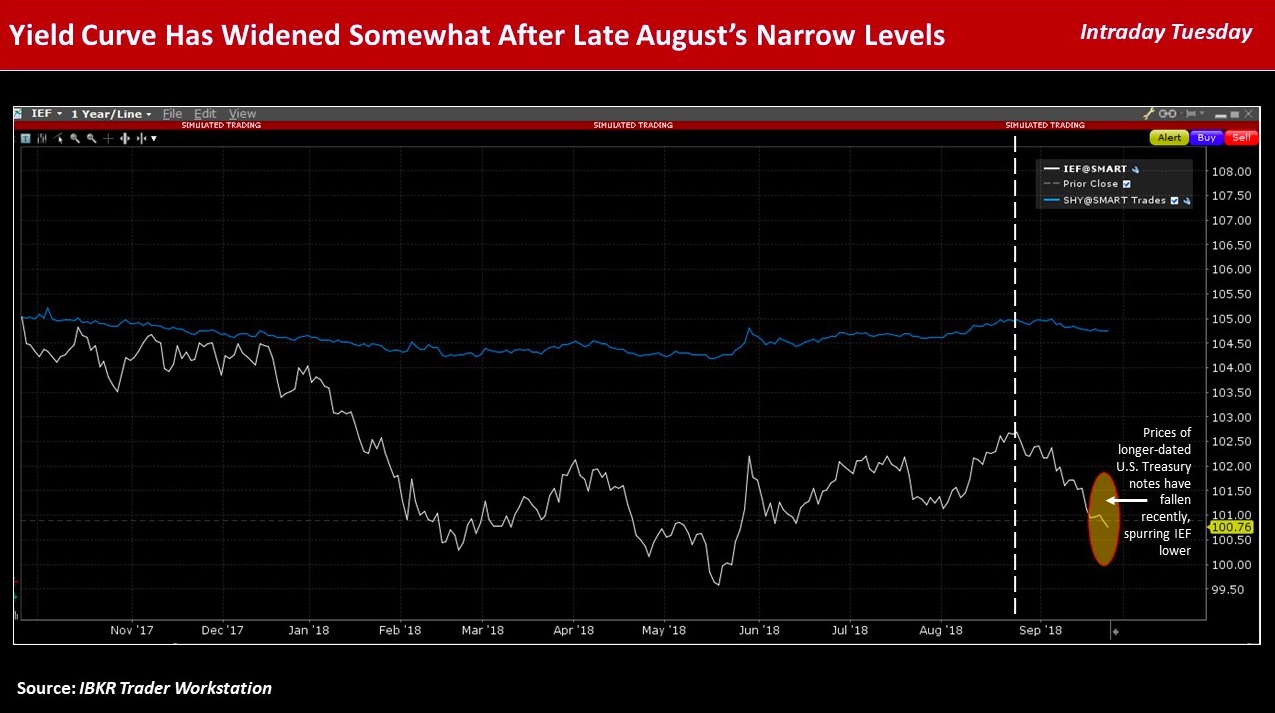

For now, the yield on the 10-year remains at a relatively elevated level – above 3% — ahead of the FOMC’s decision Wednesday, in preparation for its expected rate hike, as well as on the back of a somewhat softer U.S. dollar, as well as heightened trade war tensions between the U.S. and China.

Defensive Stocks

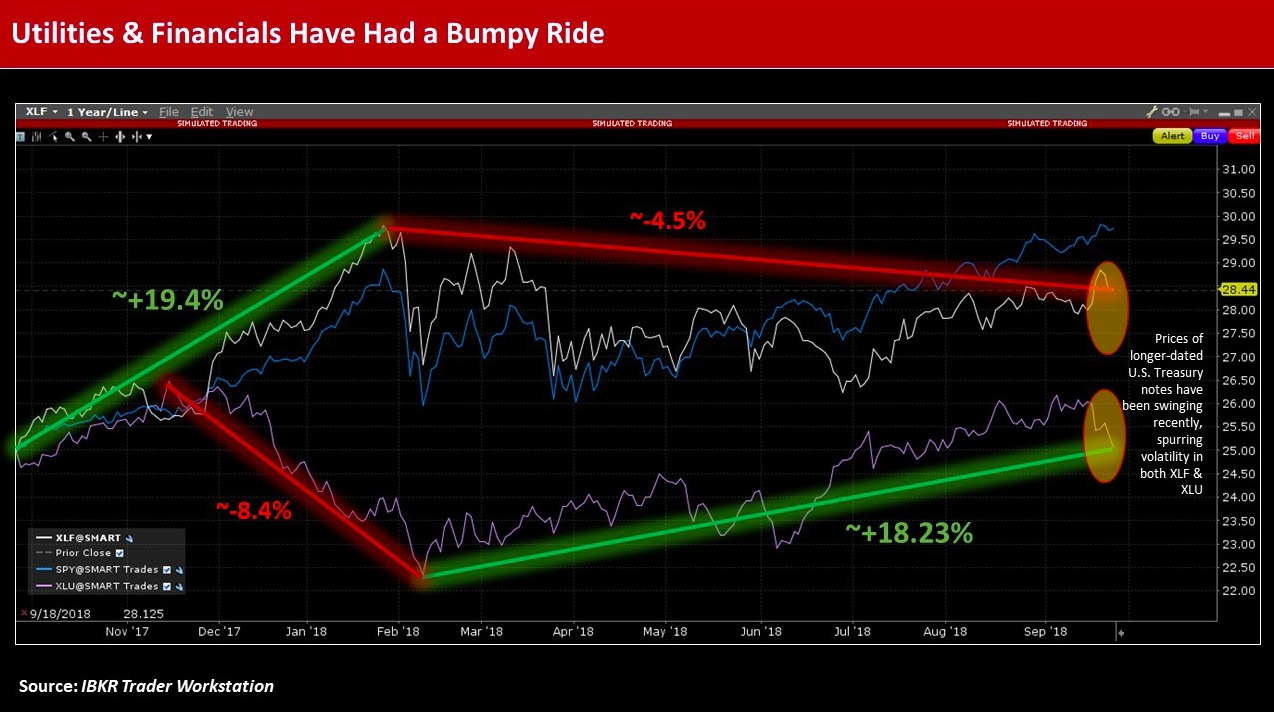

Investors in interest rate sensitive stocks, such as utilities and financials, will ultimately be faced with the uncertainties over the direction of rates until one side of the inversion argument is resolved.

Performance of the Financial Select Sector SPDR Fund (XLF) and Utilities Select Sector SPDR ETF (XLU) have had a rather choppy ride recently, amid the fluctuations of headline risks, levels of risk tolerance, and direction of U.S. interest rates.

To date, XLF has retraced about 4.5% of the almost 19.4% in gains it achieved from its 52-week year-on-year low to its peak in late January, while XLU has recently grown about 18.23% from having lost roughly 8.4% from mid-November 2017 to early February.

In the meantime, some holders of high grade, U.S. dollar-denominated bonds appear to have been compensated for the uncertainties.

In secondary market activity, investment-grade utility and financial sector bonds have each tightened by roughly 4bps in the past ten days. However, these bonds have underperformed all other sectors – except for real estate, which have narrowed about 3bps over the same period.

Photo Credit: Angus MacRae via Flickr Creative Commons

—

Disclosure: The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR or IBKRAM to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice. Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The author believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

{kind=link}

{kind=link}