Cliff Asness doesn’t have the name recognition of a Warren Buffett or a Carl Icahn. But among “quant” investors, his words carry a lot more weight in my view.

Asness is the billionaire co-founder of AQR Capital Management and a pioneer in liquid alternatives. For all of us looking to build that proverbial better mouse trap, Asness is our guru.

Unfortunately, he’s been getting his butt kicked lately. His hedge funds have had a rough 2018, which prompted him to write a really insightful and introspective client letter earlier this month titled “Liquid Alt Ragnarok.”

“This is one of those notes,” Asness starts with his characteristic bluntness. “You know, from an investment manager who has recently been doing crappy.”

Portfolio Builder

Rather make excuses for a lousy quarter (Asness is above that), he uses his bad streak to get back to the basics of why he invests the way he does.

As I mentioned, Asness specializes in liquid alternatives. In plain English, he builds portfolios that aren’t tightly correlated to the S&P 500. They’re designed to generate respectable returns whether the market goes up, down or sideways.

You don’t have to be bearish on stocks to see the value of alts. As Asness explains:You do not want a liquid alt because you’re bearish on stocks or, more generally, traditional assets. That kind of timing is difficult to do well. Plus, if you’re convinced traditional assets are going to plummet, you want to be short, not “alternative.” In other words, liquid alts are a “diversifier” not a “hedge.”

You should invest [in a liquid alt] because you believe that it has a positive expected return and provides diversification versus everything else you’re doing. It’s the same reason an all-stock investor can build a better portfolio by adding some bonds, and an all-bond investor can build a better portfolio by adding some stocks.

Diversification

When you invest in multiple strategies that aren’t tightly correlated with each other, your risk and returns are not the average risk and return of the individual strategies.

The sum is actually greater than the parts. You get more return for a given level of risk or less risk for a given level of return.

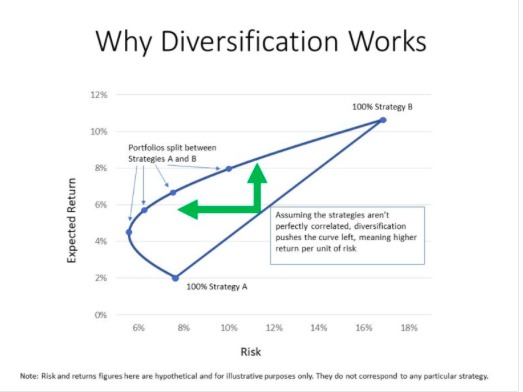

Take a look at the graph below. This is a hypothetical scenario, so don’t get fixated on the precise numbers. But know that it really does work like this in the real world.

Strategy A is a relative low risk, low return strategy. Strategy B is higher return, higher risk.

Geeky Analysis

In a world where Strategies A and B are perfectly correlated (they move up and down together), any combination of the two strategies would be a simple average.

If A returned 2% with 8% volatility and B returned 16% with 11% volatility, a portfolio invested 50/50 between the two would have returns of 9% with 9.5% volatility.

That is what you see with the straight line connecting A and B. Any combination of the two portfolios would fall along that line (assuming perfect correlation).

But if they are not perfectly correlated (they move at least somewhat independently), you get a curve. And the less correlation, the further the curve gets pushed out.

Volatility

Look at the dot on the curve that shows an expected return of about 8% and risk (or volatility) of 10%. On the straight line, that 8% curve would have volatility of about 14%, not 10%.

And accepting 10% volatility would only get you a return of about 4% on the straight line.

This is why you diversify among strategies. Running multiple good strategies at the same time lowers your overall risk and boosts your returns.

That is why I think the key is finding good strategies that are independent. In my opinion, running the basic strategy five slightly different ways isn’t real diversification, and neither is owning five different index funds in your 401k plan.

Diversification is useless if all of your assets end up rising and falling together, in my view.

Photo Credit: Mike Lawrence via Flickr Creative Commons

{kind=link}

{kind=link}