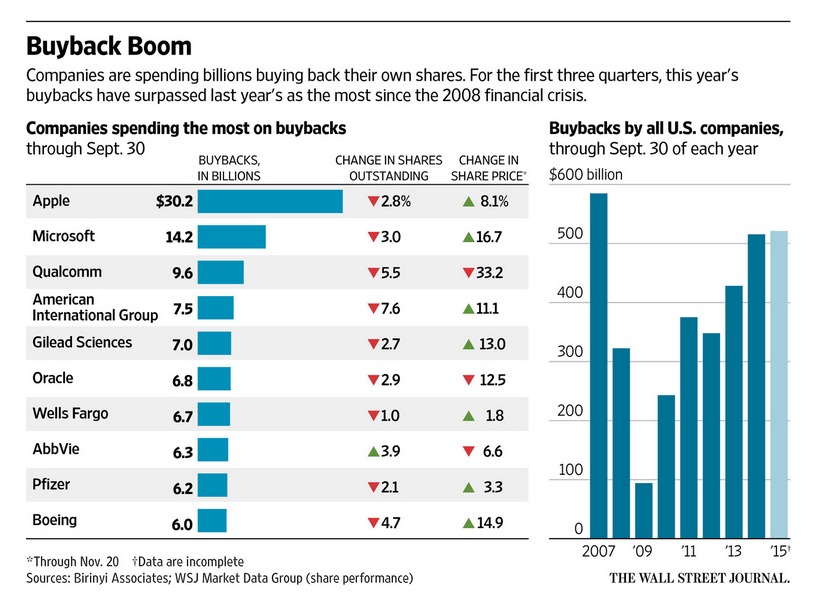

The corporate stock buyback wave has been fast and furious this year.

Buyback volumes are on track to possibly surpass the pre-financial crisis boom year of 2007.

In the year’s first nine months, US companies spent $516.72 billion buying their own shares, according to Birinyi Associates.

Among the companies that have announced buybacks in recent months are: Microsoft (MSFT), Wells Fargo (WFC), Pfizer (PFE) and Express Scripts Holding (ESRX).

Reality Bites

In theory, buybacks are a good deal for investors.

As the supply of a company’s outstanding stock shrinks, its earnings-per-share ratio rises all things being equal.

That’s the theory. In the real world, things are a bit more complicated.

Also, are stock buybacks a good thing for the overall economy?

Skeptics

Critics say the trend has artificially propped up the market, discouraged CEOs from reinvesting in new, job-creating ventures and may have even contributed to widening US income inequality.

William Lazonick, a professor of economics at the University of Massachusetts Lowell, writing in the Harvard Business Review, notes that from 2003 through 2012 some 449 companies in the S&P 500 index devoted 54% of their earnings ($2.4 trillion in all) to buy back their own stock.

On top of that, dividends accounted for an additional 37% of their earnings.

Short-Sighted

What if that $2.4 trillion were invested in new factories and businesses that might have increased jobs and wages.

Also, some skeptics point out that stock buybacks can have a distorting impact on corporate earnings.

True, by reducing the number of shares outstanding, buybacks help increase a company’s earnings per share.

When profit margins are rising, however, stock buybacks don’t have much of an impact.

They do when margin growth stalls, which has been the case the last couple of years.

Companies in the S&P 500 bought more than $550 billion of their own stock last year, inflating EPS growth by 2.3 percentage points, according to recent post by Bloomberg Businessweek.

Executive Pay

Jeremy Grantham, British investor and co-founder and chief investment strategist of Grantham Mayo van Otterloo (GMO), believes executive compensation is partly fueling the buyback trend.

When 80% of executive compensation comes from bonus and stock options, says Grantham, profit maximization trumps long-term capital investment.

Takeaway

Corporate stock buybacks are a tried and true way to boost share prices and reward investors.

Yet share buybacks also can distort earnings and may be driven by executive compensation practices that have run off the rails.

Money spent on stock buybacks are diverted from potentially productive investments in plants and new businesses.

What’s good for investors short-term may not be good for the economy long-term.

Photo Credit: Jeff Rowley via Flickr Creative Commons

{kind=link}