Let’s face it: 2015 hasn’t been a vintage year for stocks. Don’t let your tax bill make it worse.

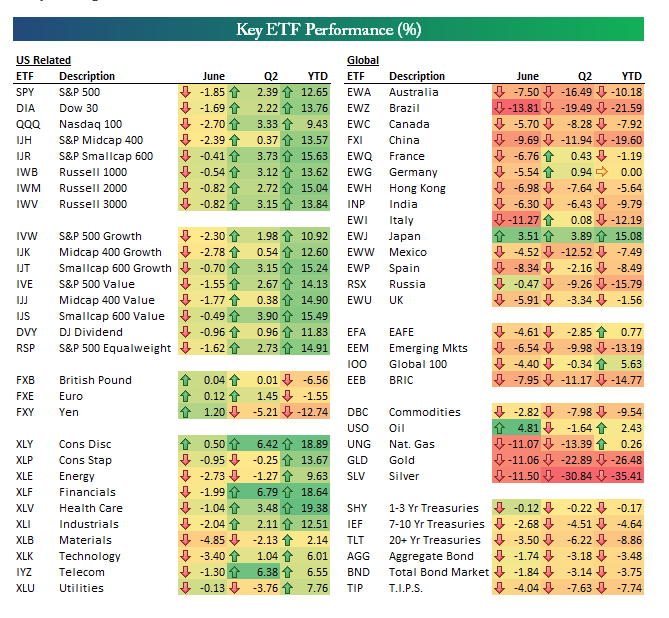

Major indices like the Dow Jones Industrial Average and S&P 500 Index are treading water and may well end up in negative territory for the first time since 2008.

Take Action

To cushion the blow, it’s time to take action before the year-end to reduce taxes and tune up your personal finances.

Here are six tips worth considering.

1) Tax-Loss Harvesting

In a volatile year like this one, you may have some losses in your portfolio.

If so, one way to reduce your tax liability is through tax-loss harvesting.

The basic strategy here is to sell off losing investments before year-end to reduce the tax liability on capital gains on your winning investments.

Should you decide to buy back the security later, make sure you consult with a tax attorney first.

The IRS does not allow dumping a stock for tax purposes and turning immediately around and buying it back, a so-called wash sale.

There is usually a waiting period depending on the investment involved.

2) Capital distributions

You might also consider checking into whether your mutual funds or ETFs are making capital gain distributions before year-end.

Oftentimes a fund manager will decide to sell a stock to lock in profits or to raise cash for shareholder redemptions.

In such cases, the fund will then distribute at least 95% of the gains to shareholders and that’s a taxable event.

If the fund has already delivered robust returns in 2015 and you were considering selling it in 2016, it may make sense to sell before the record date of the capital gain distribution.

3) Retirement contributions

If you plan to max out on your contributions to your 401(k) or an IRA to save on a tax-deferred basis and lower your 2015 tax bill, now is the time.

Contributions to your 401(k) or other retirement plans need to be made by December 31.

The limit on 401(k) contributions for those under 50 is $18,000 this year and in 2016.

4) Charitable giving

Writing a check to a charity is a tried and true tax savings strategy late in the year.

However, some investors also opt to donate stocks and bonds to a worthy cause.

The tax advantage is two-fold: You can deduct the current market value of the asset from your taxable income and don’t have to worry about paying any tax on capital appreciation that you may have accumulated.

5) Flexible spending accounts

These flex plans allow employers to set aside money on a pre-tax basis to pay child care or medical bills.

Trouble is, these accounts follow the “use it or lose” rule.

So if you are concerned you won’t be able to spend the money in the account before the end of the year, all may not be lost.

The IRS does allow a grace period for this set-aside money until March 15.

Check to see if your employer has adopted this program.

Takeaway

With a little bit of effort and planning, you may be able to lower your 2015 tax bill and shore up your portfolio for the year ahead.

You shouldn’t leave any money on the table, especially in such a disappointing year for stocks.

This article contains general information regarding taxes. Covestor is not an accounting firm. Please consult your accountant or tax attorney for personalized advice regarding your specific situation.

Photo Credit: DonkeyHotey via Flickr Creative Commons