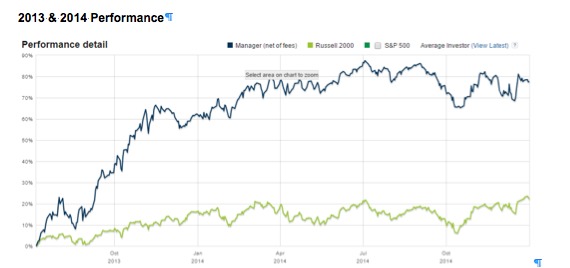

The Leveraged Value portfolio is comprised of small cap companies. The Russell 2000 is my benchmark and my goal is to outperform it each year.

Despite the volatility, 2014 was a good year for the portfolio. The strategy returned 9.5% vs 4.9% for the Russell 2000.

Small-cap oil firms

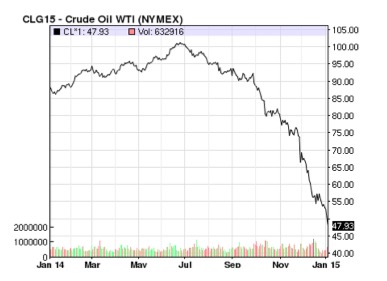

The plunge in oil prices over the second half of 2014 has given U.S. consumers a boost.

On the other hand, the trend was not so favorable for oil stocks.

Small-cap oil companies were hit the hardest, with many declining 50% to 75% from their highs.

Buying Opportunity

This certainly was a big hit to the Leveraged Value portfolio, but I believe the decline is an opportunity to increase my holdings in oil.

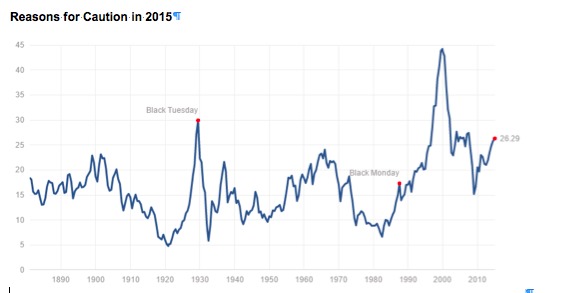

The next chart is shows the trend line of the Shiller P/E Ratio, which is based on average inflation-adjusted earnings from the previous 10 years. (This measure is also known as the Cyclically Adjusted PE Ratio.)

Without going into all the details, this metric is one tool I use to gauge if the stock market is overvalued or undervalued.

Valuations

When the Shiller P/E Ratio is high, expected future investment returns are lower and vice versa. This metric is not meant for short-term market timing.

However, historically when the Shiller P/E is extremely high (above 25), it has been followed by steep market declines.

So what should investors do?

For investors with a long-term time horizon, you may want to consider decreasing your portfolio’s allocation to US markets and substituting with international funds.

At current prices, the US stock market is easily the most expensive market in the world.

In my opinion, additional international exposure may limit your downside and give you better prospects for the future.

Strategy

Right now, the 56% allocation to the financial sector in the Leveraged Value portfolio reflects what I believe to be a very undervalued insurance sector.

The 56% concentration is a bit deceiving as approximately 15% is in banks which don’t necessarily move in tandem with the insurance sector.

In December, I doubled down on oil companies and made energy the 2nd largest sector in the portfolio.

By no means am I an oil trader, but I do believe the case for oil returning higher is much greater than oil remaining in the $40/barrel range.

Oil prices

For the more curious readers, I recommend reading Tom Armistead’s statistical analysis on the price of oil.

Due to the volatility of small cap oil stocks, the performance of the Leveraged Value portfolio vs. its benchmark will likely depend on oil prices in 2015.

In the event of prolonged low prices, I’ve identified oil companies with strong financials which I believe will best weather this storm.

DISCLAIMER: The investments discussed are held in client accounts as of December 31, 2014. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.

{kind=link}