Equity markets are off to a rocky start this quarter. As of October 15th, the S&P 500 Index was down 5.49% quarter-to-date but still up 2.40% for the year.

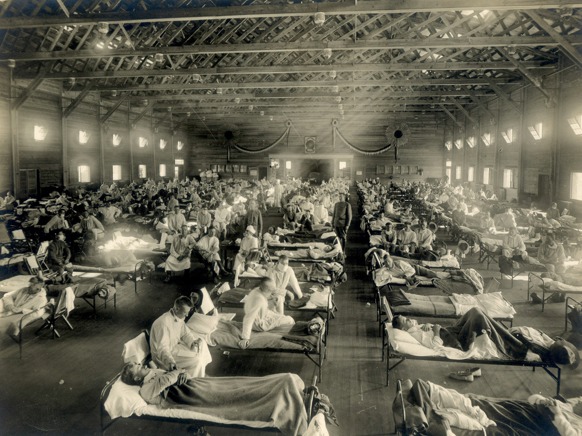

Ebola is dominating the headlines, but it’s useful to place the outbreak in historical perspective compared to other pandemics such as the deadly Spanish influenza that killed millions after World War I.

Long view

In the United States, there are only two known Ebola cases at this time and governments globally are ramping up action plans.

From a historical perspective on past pandemics, I came across the following analysis from Merrill Lynch citing research by Fidelity.

“The stock market impact of three major pandemics was analyzed by Fidelity, and the results were mixed. During the Spanish Flu of 1918, the S&P 500 dropped almost 25% and recovered by almost 9% the following year.

However, in the Asian Flu of 1957, the S&P 500 was up 24.7% that year and the market followed up with a 2.9% gain in 1958. Similarly, the market gained ground during the Hong Kong Flu of 1968, with a 12.5% increase by the S&P 500 in 1968 and a 7.4% increase in 1969.

Given the global nature of supply chains today vs. 50 or 100 years ago, however, it is not hard to imagine that in a pandemic scenario, global trade would be significantly impacted and could result in a meaningful decline in the stock market.”

Oil prices

As for the ISIS threat in Iraq and Syria, nobody would have thought a few years ago that you would see oil prices collapsing under such disruptive circumstances.

Given this, current domestic economic issues are contained to a great degree and there may be an underlying thought that if this country decided to take greater military involvement, the ISIS threat could be greatly diminished.

This is a pretty simplistic view of a bad and complex situation. Nevertheless, I think it makes sense from a market perspective.

As for oil prices, this is one of the positive forces alluded to earlier. This is helping pocketbooks here and also puts additional strain on Russia (very dependent on energy revenues) and its expansionary exploits.

Also helping are economic numbers that have been favorable and the Fed that continues to be data dependent and careful in its steps to normalize interest rates.

China slowdown

On the other hand, Europe is not looking strong and conditions in China may be slowing.

A resulting impact of all this is that the dollar has strengthened which is helpful in some areas but not very helpful in the area of exports that become more expensive.

Given this and the low level of expected inflation, the Fed may be compelled to be more careful with its monetary policies.

Tapering is likely to end this month but increases in short-term rates could get pushed out to a later date depending developments and data.

At this time, markets are giving indications that the first move may not take place until next fall verses earlier expectations of a summertime move.

In closing, I still believe a long-term perspective is the best and most potentially productive way to view this market.

DISCLAIMER: The investments discussed are held in client accounts as of September 31, 2014. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.