By: Anqi Dong, CFA, CAIA, Senior Research Strategist

- Non-cyclical Consumer Staples businesses offer earnings resiliency

- The Homebuilders industry offers attractive valuations in a structurally under-supplied market

- Cybersecurity is a top area of increasing investment in IT budgets

Surprisingly, US equities finished the first quarter on a high note, up 7.5% after a few tumultuous weeks triggered by hotter-than-expected inflation data and emergency government interventions to backstop deposits in the wake of the collapse of Silicon Valley Bank and Signature Bank. The lingering effects from the regional bank turmoil — tighter lending standards and more fragile business sentiment — likely will lead to weaker growth and higher recession risk. Earnings estimates still look too optimistic and equity valuations are too stretched for a soft landing. The silver lining is that the Federal Reserve (Fed) may not need to tighten much more to rein in inflation.

Against this backdrop, we favor Consumer Staples, a defensive position with attractive valuations; homebuilders, a downtrodden cyclical industry with stabilizing fundamentals and historical low valuations; and cybersecurity, a secular growth industry with resilient near-term demand.

Consumer Staples: Non-cyclical Businesses with Earnings Resiliency

Twelve months into the most aggressive rate hike cycle, leading economic indicators continue rolling over into deeply negative territory, pointing to risk of recession. Indeed, the probability of an economic recession in the next 12 months predicted by Treasury spreads spiked to near 60% over the first quarter.1 While improved economic sentiment in the first two months this year gave investors hope for a no-landing scenario, the recent regional bank turmoil reminded them of the damage intense rate hikes can cause and the growing vulnerability of the economy.

The earnings outlook seems disconnected from this negative macroeconomic backdrop. The earnings per share (EPS) trajectory is still well above its pre-pandemic trend, implying a growth rate of 0.8% for 2023 and 12.5% for 2024, even after analysts lowered 2023 and 2024 EPS estimates by 12% and 9%, respectively, from their peak.2 Furthermore, the consensus estimate of operating margin for 2023 is higher than last year and well above the pre-pandemic five-year average.3

These above-trend projections on earnings and profit margin appear far-fetched in an environment with elevated inflation and recessionary prospects. The earnings trend during historical recessions provides context for the downside risk of the current consensus earnings estimates. During the seven economic recessions since 1963, the S&P 500 avoided a greater than 10% decline in earnings just once, in 1980.4 Excluding the two deepest declines during the Dot-Com Bubble and Global Financial Crisis (over a 50% drop), S&P 500 earnings declined an average of 16.8%.5

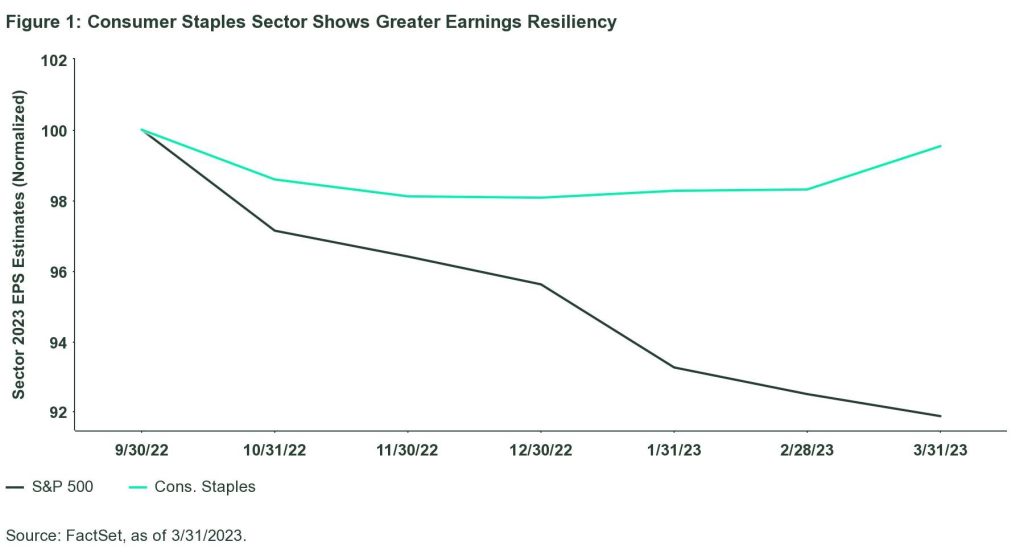

Given the increasing recessionary risk and downside risks to earnings revisions, Consumer Staples’ non-cyclical business and earnings resiliency may add value to investors’ portfolios in a challenging economic environment. Amid earnings downgrades across the broad market, Consumer Staples’ earnings outlook has been relatively stable, with 2023 EPS estimates down just 0.5% over the past six months, compared to a decline of 8% for the S&P 500. (See chart below.)

Disinflation in the sector’s input costs, such as packaging, transportation, and agriculture prices that began late last year may also support the sector’s profit margin this year.6

After lagging the broad market by 7% in Q1, Consumer Staples’ relative forward price-to-earnings valuations have come down below their long-term median (38th percentile).

Homebuilders: Attractive Valuations in the Structurally Under-Supplied Market

Last year’s aggressive Fed rate hike hit homebuilder stocks the hardest. The spike in mortgage rates and elevated home prices impaired housing affordability, resulting in sharp declines in home sales and construction activities. However, as housing prices start cooling and mortgage rates trend lower, the industry has shown some recent signs of stabilization. February existing home sales beat expectations, increasing 14.5% — the largest monthly gain since July 2020. And with inventory at historic lows, demand has shifted to the new home market. Forward-looking indicators on new construction, including housing starts and permits, are well ahead of February’s estimates , registering meaningful increases for the first time since last May.7 As a result, homebuilder confidence rose for the third straight month in March, with builders reporting better-than-anticipated new home sales and higher traffic of prospective buyers.8

The homebuilder earnings outlook is stabilizing against this backdrop. The number of earnings downgrades decreased for the fifth straight month in March to its lowest level in a year.9 Thanks to easing supply chain pressures and disinflationary trends in goods, prices of building materials have declined on an year-over-year basis for three straight months to the level of April 2021,10 turning one of last year’s earnings headwinds to a tailwind. On the demand side, strong labor markets and household balance sheets may support homebuyer confidence once mortgage rates stabilize at a lower level. Homebuilders’ strong Q4 earnings and sales surprises on the back of retreating mortgage rates suggest that once rates peak, homebuyers will jump back into the market.11

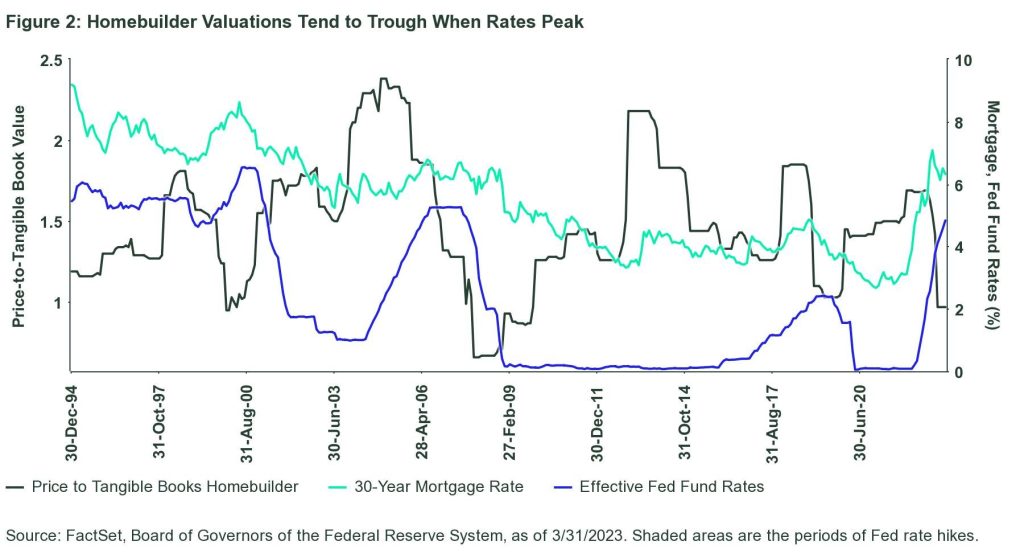

Some investors may question the bullish stance in Homebuilders when unemployment rates are expected to be higher and recessionary risks have increased after the regional bank turmoil. We believe the current valuations for homebuilder stocks are pricing in a more serious downturn than our base case where the economy experiences a mild recession without severe job losses and the deflationary process continues so that more dramatic moves in terminal rates can be avoided. Homebuilders are currently trading below their tangible book value — at the lowest level since the 2008 housing crisis, as shown in the chart below. Furthermore, homebuilders’ price-to-tangible-book-value ratio has tended to trough when rates peak, except during the 2008 housing crisis.

As we approach the end of the rate hike cycle, homebuilders may experience valuation expansion.

Cybersecurity: A Top Area of Increasing Investment in IT Budget

Remote work and cloud adoption have accelerated the digital transformation since the start of the pandemic exposing organizations to greater cybersecurity risks. In fact, cybercrime is one of the top 10 global risks ranked by severity over the next two years.12 While IT budgets have been under pressure amid an economic downturn, investments in cybersecurity have not been targeted for cost cuts, as business leaders understand the significance of cyberthreats and the financial and reputational damages they may cause.

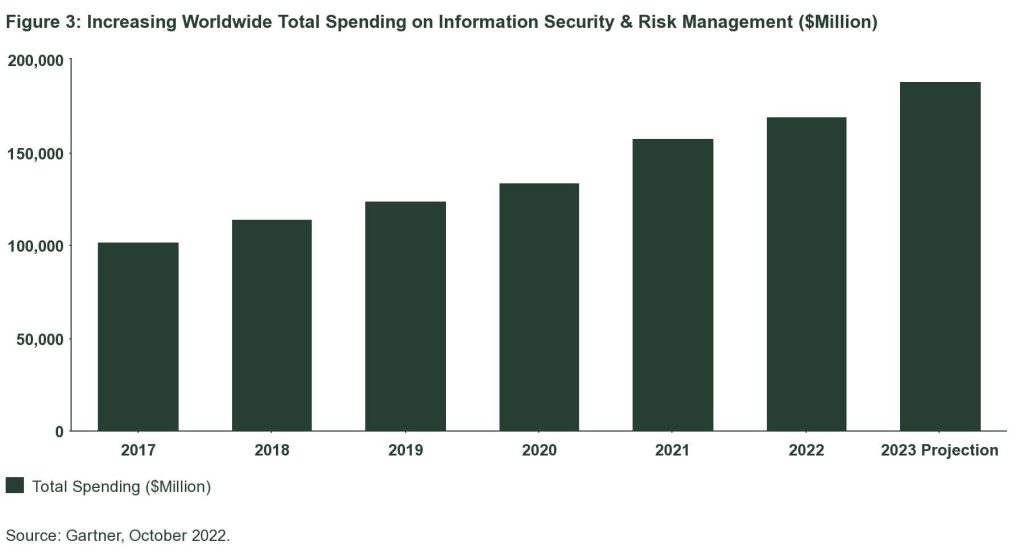

In fact, 91% of business and cybersecurity leaders believe a catastrophic cyber event is likely in the next two years, according to 2023 Global Cybersecurity Outlook by the World Economic Forum. And 43% think the cyberattack will materially affect their own organization. As a result, businesses are dedicating more resources to day-to-day defense. The Gartner Survey of over 2,000 chief information officers reveals that cyber and information security is the top area of increased investment for 2023, surpassing data analytics, cloud platforms, and artificial intelligence.13 Spending on information security products and services is projected to grow 11.3% to more than $188 billion in 2023, driven by accelerating growth in application security, cloud security, and zero trust network access.14

The US government is also strengthening the nation’s cyber-defense through public investment. President Biden’s FY 2024 budget proposal allocates roughly $26 billion to implement the recently released national cybersecurity strategy, including $13.5 billion for the Pentagon to advance its adoption of zero trust architecture and $12.7 billion (a 13% increase over the 2023 enacted level) in funding for federal civilian agencies.15

Given society’s increasing investment in cybersecurity, companies whose products and services are driving innovation in future security may present long-term growth potential.

Footnotes

1 Federal Reserve Bank of New York, as of 3/31/2023

2 FactSet, as of 3/31/2023

3 FactSet, as of 3/31/2023

4 FactSet, State Street Global Advisors, from 1/1/1963 to 12/31/2022.

5 FactSet, State Street Global Advisors, from 1/1/1963 to 12/31/2022.

6 CFRA Industry Surveys, Household Products, January 2023

7 National Association of Realtors, Census Bureau, as of March 21, 2023.

8 NAHB, as of 3/31/2023

9 FactSet, as of 3/30/2023. The industry is represented by the S&P Homebuilders Select Industry Index.

10 PPI, as of of 3/30/2023

11FactSet, as of 3/30/2023.

12Global Risks Report 2023, World Economic Forum, January 2023

13 2023 CIO Agenda, Gartner, October 2022

14 Gartner Identifies Three Factors Influencing Growth in Security Spending, Gartner, October 2022

15 Biden Administration Seeks $26B in Cyber Funding for FY 2024, Nextgov.com, March 16, 2023.

This post first appeared on April 24th, 2023 on the State Street Global Advisors Blog

PHOTO CREDIT: https://www.shutterstock.com/g/Piscine

Via SHUTTERSTOCK

DISCLOSURE

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit nor guarantee against a loss.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.

Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The authors believe that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

{kind=link}

{kind=link}