The S&P 500 Index, which most financial professionals use to track the performance of the overall U.S. stock market, has now officially tripled in value — along with breaking through the 2,000 level for the first time, ever.

In a recent post, we looked at how often investors should expect 5% corrections, based on market history. This time, however, we’ll examine previous bull markets in which U.S. stocks have tripled, and see what lessons there are to be learned.

After all, when it comes to investing, you want to be looking ahead, not in the rear-view mirror. And remember, history never repeats exactly — it rhymes.

Here are 3 things investors should know now that the market has tripled from the 2009 financial-crisis low:

1. This has only happened four other times in recent history

The Armo Trader blog notes that that since 1962, the S&P 500 has tripled from a major low on four occasions.

So the S&P 500 is up 200%, but the interesting thing about the current bull market is that so many individual investors don’t trust it.

Who can blame them? Investors burned by the dot-com implosion and the financial crisis within a decade are afraid of another nasty drop, and many have missed the rally.

Now, it’s even harder for them to get off the sidelines because the market has already enjoyed a great five-year run. And some investors think stocks are too pricey.

“The United States stock market looks very expensive right now,” Yale economics professor and Nobel Prize winner Robert Shiller wrote in a recent New York Times column.

Finally, some investors find it psychologically difficult to buy stocks when they’re at all time highs, which takes us to our second point…

2. All-time highs don’t mean the market is automatically due for a pullback

It has been over two years since a 10% correction, and five years without a 20% decline.

Some bears point to all-time highs and the lack of a correction as proof that we’re overdue for a pullback.

However, independent trader and market technician Ryan Detrick warns not to be fooled into thinking new highs are bearish.

Making new highs in the S&P 500 “isn’t some bearish event like so many claim,” he says. New highs actually “tend to happen in clusters that can last years.”

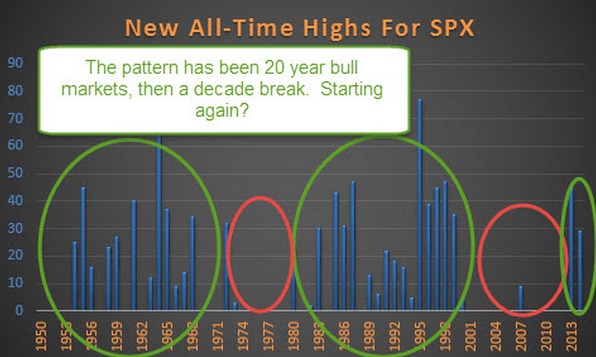

In the chart below, Detrick shows that new highs have been a common feature of bull markets since 1950.

“Could we really have another 15 years of the this bull market? I have no idea to be honest. Still, my best advice is be open to it,” he writes. “It has happened before and very well could happen again.”

Notice how Detrick is using history as a guide to manage expectations, rather than as a crystal ball for precise forecasts.

Which takes us to point #3.

3. No one knows when the bull market will end

Investors have more information at their fingertips than ever before. Yet no one piece of data or research will tell investors when a bull market is over. They don’t ring a bell at the top of the market, as the old Wall Street adage goes.

That said, history shows that bull markets tend to end when investors are “euphoric,” which is a subjective term, writes Yahoo Finance contributor Ben Carlson.

“[M]arkets are emotionally-driven. There are so many moving parts involved that it’s impossible to simply use a single variable or even a handful of variables to tell you exactly when the good times will end,” he says.

“Market historians often want to pinpoint what single factor tells investors to buy or sell. The reasons are often obscure and based on ‘animal spirits,’ or irrational, unpredictable, herd behavior,” adds Reuters columnist John Wasik.

To sum it all up, it seems that investors have yet to reach that euphoric level that have signaled previous major market tops. At the same time, the mood has improved significantly from the depths of the financial crisis.

So we’re probably somewhere in the middle, although exactly where is open to debate.

Continue learning: How often should investors expect 5% market corrections?

—

{kind=link}