The biggest financial news of 2013 is that the Fed’s quantitative easing is finally starting to wind down. The Fed is reducing its $85 billion in monthly purchases of US Treasuries and mortgage backed securities by $10 billion.

Throughout 2014, the Fed is expected to continue to “taper” off their securities buying binge and ultimately end it entirely. The program became necessary because the Fed’s normal monetary tool–controlling the federal funds overnight lending rate between banks– became less effective as interest rates got closer to zero.

Is the stock market heading for a correction? This Bloomberg chart down below is making the rounds. History may not always repeat itself, but sometimes it rhymes. Notice the similarities between the S&P 500 Index (SPX) move since May 2012 with the movement of the index in 1929 and 1930 during the Depression era. Yes, past results are no guarantee of future performance, but paying attention to your surroundings is always highly recommended.

US Borrowing Binge

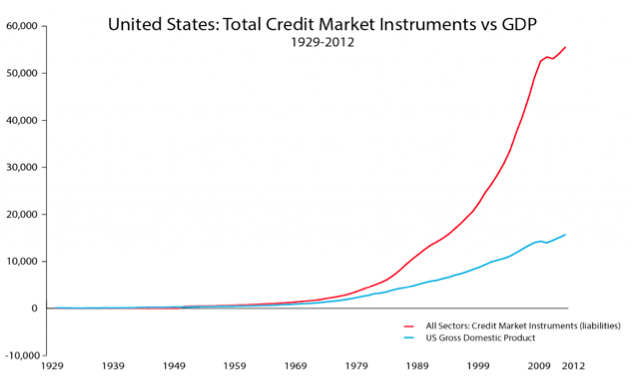

This next graph showing bond issuance levels in the United States came from the St. Louis Fed and was discussed at length by Grant Williams with Mauldin Economics. In essence, he states that we have been a multi-decade credit induced binge, which has been disguised as “growth,” ever since we dropped the Gold standard in 1971.

Notice how highly correlated this is to the larger move down in interest rates in the chart of the US Treasury “Long Bond.” (Second chart below.) Interesting also how parabolic the debt issuance starts to go in 2009/2010.

Clearly this is no coincidence: U.S. interest rates moved incredibly low for 30 years and debt issuance mushroomed. Meanwhile debt levels in the UK, Canada, Sweden, and Korea, among others, are also up substantially.

Also widely discussed by Grant and others and certainly worth noting: the Federal Reserve Banks balance sheet reached a record $4 trillion worth of assets, but only total capital of $55 billion. So the Fed has about 70 times more assets than capital and clearly very highly leveraged.

As a point of reference, some of the more highly leveraged firms during the global economic collapse of 2008 such as Lehman Brothers and Bears Stearns were about half as leveraged as the Federal Reserve is currently. We are not sure, given the fact the Fed prints its own currency, this is as much a problem here, but certainly an interesting situation.

We feel like the genie is clearly out of the bottle, and getting him back in will be a challenge. A further observation from Dennis Gartman, editor of The Gartman Letter: the Feds balance sheet has quadrupled in the last 5 years, but nearly doubled in the last year alone.

Hall of Shame

As 2013 comes to a close, Leonardo DiCaprio is starring in The Wolf of Wall Street about the boiler room king of Stratton Oakmont, Jordan Belfort. He is a devotee of the classic “pump and dump” scam which made Robert Brennan of First Jersey Securities famous in the 1980s.

This was a surreal ending to 2013 perhaps, but seriously I can’t remember a year where more mega-fines were handed out, and this time some people actually had to admit guilt. I hope the money actually gets into the hands of those affected.

Consider the tens of billions in fines for the real estate and foreclosure debacles, the Libor crisis fines, the London Whale of JP Morgan (JPM), and the insider trading problems at SAC capital. These massive fines indicate their business models and practices need some tweaking. There is also a currency fixing crisis investigation underway. The Wolf of Wall Street hasn’t wowed the critics, but the film is certainly timely.

In other developments, former Chairman of Goldman Sachs and Ex-Governor of New Jersey Jon Corzine avoided criminal charges for his role in the collapse of MF Global.

Gold lost its allure and delivered a horrible performance during the calendar year. Despite the incredible current physical demand out of the Far East (largely China and India), the SPDR Gold Trust ETF (GLD) continued to slump, despite the rally in the stock market.

I don’t believe gold is some barbarous relic, but over time, one of the true stores of value. And I recommend that investors check out the analysis of gold bull Richard Russell, who writes the Dow Theory Letter, about gold for those who are interested.

I think GLD is a suitable way to own gold, as most people would be hard pressed to find a better solution. Owning gold coins is an obvious alternative, but perhaps a more inconvenient way.

Bitcoin is clearly one of 2013 ‘s most interesting financial stories. The virtual currency is “mined” by data server farms solving complex math problems and earning Bitcoins in the process.

Although the virtual currency can be used on Virgin Air to buy a trip into space, its too crazy to view as foreign exchange substitute, given its incredible volatility, and lack of an country of origin.

It reminds me of the dot.com era, and I can’t pretend to know enough about it to ever invest, so we will watch from a far. I’m also cautious when it comes to Facebook (FB) and Twitter (TWTR). I’m wary about the runup in their stock prices, given the unusual metrics of these companies.

2013: Winners and Losers

As for the Covestor Oceanic Capital portfolios, I used to like Microsoft (MSFT), but it stumbled at the end of 2012. The breakout happened this fall after the announcement that CEO Steve Ballmer would step down within 12 months and someone new would take over. Clearly the concept of some fresh blood at the helm excited stock investors.

Obviously GLD and Market Vectors Gold Miners EFT (GDX) were the biggest losers for my portfolios, substantially limiting my performance. We really lament calendar year time horizons, we feel they effectively encourage shorter term views, and therefore holding periods. This type of investing encourages the worst behavior of all; playing beat the clock. It tends to make us force things by over-trading in the hopes of accelerating our gains.

Stocks in 2014

The new year will likely continue the present trends, the Federal reserve is on our side, so domestic equities I believe may continue to do well. I expect stock prices to rise 10%-plus in 2014. I will likely look to trim things back to the allocation levels I started with last year, and then add to other allocations.

In my opinion, international and emerging equities should continue to roll and even gather a bit more momentum, and we look for further gains this year, likely we will be increasing our allocation slightly to each sector.

The real estate sector should continue to gradually move forward and gain some steam. Things have gotten back to pre-crisis levels in some areas and the Federal Reserve will likely be paying close attention. The central bank will not want mortgage rates to rise too rapidly and potentially cut off what seems now to be a good recovery. This asset class should also continue to do well this year and we will look to bump up our allocation slightly.

Bond ETF holdings have clearly broken out of their 30-year bull market and we can only see holding shorter term maturities as a hedge for any adverse movements in the stock markets. The longer maturities will likely feature a slow bleed of value as interest rates rise, interrupted by sporadic counter-cycle rallies.

Oil & gas prices seem poised to come down in price with the political instability in both Libya and Iran quieting down. It behooves both countries to get their exporting act together and get their petro-dollars. They need hard currency and it may not be long before the U.S. stops importing oil entirely and totally changes the dynamics of this market.

Commodities seem like they could continue to be softer this year, but I will keep my smaller allocations there as a hedge, knowing that China or India could surprise and boost demand. Throughout my career I’ve seen quite a few Black Swan events, and they never seem to announce themselves in advance.

The markets have been doing well for almost five years and feel good right now, but the debt ceiling debate in the summer of 2011 reminded us all of the value of owning assets that will respond well in times of crisis.

Ultimately we feel our gold position will rebound, and longer term serve us well again, but with the Fed continuing to promise low rates into the foreseeable future, possibly into 2015, we may need to hedge against continued good fortune.

DISCLAIMER: The investments discussed are held in client accounts as of December 31, 2013. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.