Late in 2012, Bank of America analyst Michael Hartnett set off an interesting debate in global financial circles with his “Great Rotation” investment thesis in which he predicted a huge shift in capital from the bond market to stocks. He made his call in a provocatively titled report: The Bond Era Ends.

The basic idea: the U.S. economic rebound, led by a housing recovery and stronger corporate earnings, would make equities a far more rewarding investment than bonds, which had been a smart investment during most of the recession and economic recovery period but are at present richly priced.

Though the stock market has bounded from one record high to another and bonds have taken a beating of late as the U.S. Federal Reserve prepares to taper its quantitative easing programs, not everyone is buying Hartnett’s market call. Here’s the case against the Great Rotation.

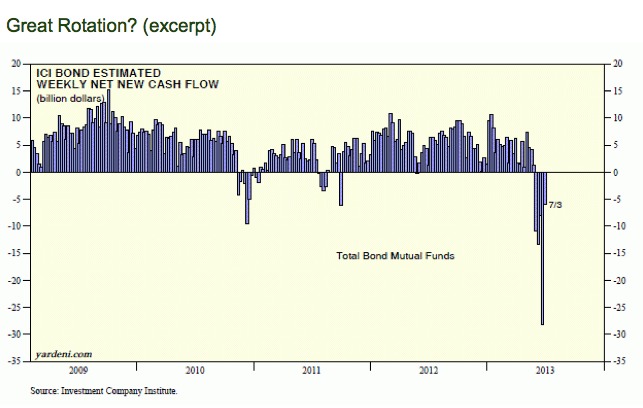

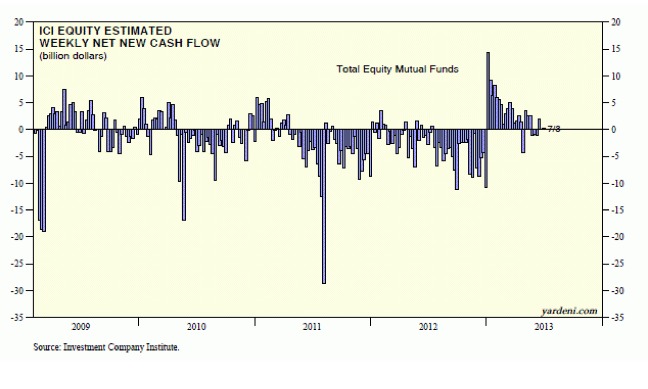

Market strategist and economist Ed Yardeni posted two charts on his blog this week that suggest it’s far too early to confirm a big exodus of cash into stocks, though bond outflows in recent weeks have been notable. Here’s Yardeni’s take:

What is the likelihood of a “Great Rotation” out of bonds and into stocks? Weekly data estimated by the Investment Company Institute show that $66.7 billion poured out of bond mutual funds during the past five weeks through July 3, while only $0.3 billion flowed into equity mutual funds. So far, the evidence suggests more of a Great Liquidation out of bonds and into cash than a Great Rotation into equities.

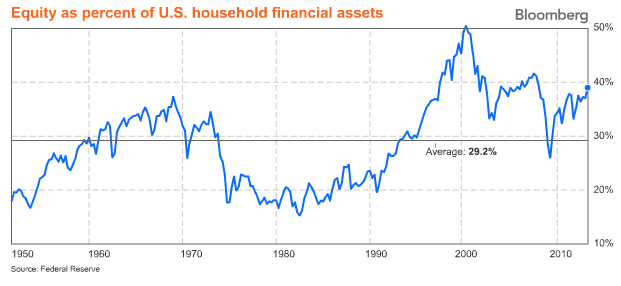

Sanford C. Bernstein & Co.’s chief market strategist Vadim Zlotnikov recently told Bloomberg that he doubts investors will push stocks higher by moving away from bonds. He points to Fed data showing that equities as a percentage of household financial assets were at about 39% at the end of March. That’s about the level in 2007–and well above the 29% historical average going back to 1950. The New York strategist points out:

Sanford C. Bernstein & Co.’s chief market strategist Vadim Zlotnikov recently told Bloomberg that he doubts investors will push stocks higher by moving away from bonds. He points to Fed data showing that equities as a percentage of household financial assets were at about 39% at the end of March. That’s about the level in 2007–and well above the 29% historical average going back to 1950. The New York strategist points out:

U.S. households’ exposure to equities is already above historical levels. With rates likely to rise over the next 12 months, the case for a rotation from bonds into equities may become less compelling.

Meanwhile, bond guru Bill Gross, co-founder of Pacific Investment Management Co., remains bullish on bonds, at least long-term. He’s been adding Treasuries to the Pimco $268 billion Total Return Fund that he manages. The proportion of U.S. government debt in the fund rose from 37% to 38% in May. In his June Viewpoint investment outlook posted on Pimco’s website, Gross makes his long-range case for bonds:

It’s important for investors to remember the reasons they own bonds in the first place – namely for the potential for the preservation of capital, income and growth, relative steadiness and typically low to negative correlations with equities. These needs – which will only become more urgent as millions of baby boomers head to retirement over the next decade and a half – are long term, regardless of what markets are doing today. So fixed income should always have a place in a portfolio. Still, there are ways to navigate challenging markets without feeling stuck. One is to expand your investment universe by going global. Here at PIMCO we like to say that there is no “bond market,” but rather “a market of bonds.” So, you should prize flexibility in your fixed income manager or core bond strategy.

Perhaps the most the compelling argument against the Grand Rotation thesis comes from Richard Bernstein, who was a well-known strategist at Merrill for two decades before leaving to open his own asset management firm. In a recent Barron’s interview, he argued the big rotation to watch isn’t from bonds to stocks—but from foreign assets into U.S. assets:

A lot of people have talked about how the great rotation will be a shift from bonds to stocks. But that’s not right. The great rotation — and the biggest decision you have to make for your portfolio — is that for five to seven years, it is not going to be bonds to stocks, but rather non-U.S. assets to U.S assets. We are maybe in the fourth inning of a secular period of outperformance for U.S. assets.

Photo Credit: josef.stuefer

{kind=link}

{kind=link}