To get a handle on the market’s reaction to the Fed, it’s first important to understand exactly what the Fed said. Here’s Fed Chairman Ben Bernanke from last week: “If the incoming data are broadly consistent with this forecast (talking about how the Fed has improved their forecast for the economy), the committee currently anticipates that it would be appropriate to moderate the monthly pace of purchases later this year.”

In English: The Fed has increased its estimates for the U.S economy through 2014. IF this outlook comes to pass, then and only then, will the Fed start to ”taper” or reduce its current QE program. In fact in his statement, Bernanke said that if the economy would soften further, then that would be cause to continue or even increase the current stimulus. Unfortunately the markets are behaving as if the tapering is a foregone conclusion, and will start soon, as we are already half way through 2013.

Personally I will take Big Ben at his word. We will need to see improvement in economic conditions to see a change in Fed policy. Key word is improvement, improvement over current expectations. So the question that needs answered is, “Is the economy showing signs of growth above and beyond current expectations?”

I don’t see it. Fully 65% of the economic prints in March missed their targets to the downside. From May 1 through June 12 I tallied 57% of economic prints missed estimates. Last week,the Philly Fed Business Outlook surged ahead, as did new home prices. However, China’s PMI report was a disaster as the biggest decline was in exports. This shows a global slowing as China is selling less stuff to the rest of us.

Back home U.S. PMI, (a leading indicator of business activity) also was a miss, as was the new claims for unemployment – more claims = higher unemployment rate. So here at home we are 50/50 on the latest data, but also seeing troubling signs from China and Germany’s PMI, which as major exporters indicate global slowing. With real wages stagnant, and employment waning it seems to me we are in the same boat as the Chinese and Germans – looking for emerging markets to buy our stuff to bolster GDP. But don’t look now, but emerging market economies are in the tank.

Remember the Fed raised its growth expectations to come to the conclusion that tapering could be done by mid-2014. Analysts will need to raise estimates too if in fact the economy is accelerating. If they are still missing on at least 50% of their estimates I just don’t see the accelerating economy the Fed allegedly anticipates. I see it as Bernanke’s wishful thinking. He wants to go out with the economy currently on the mend, and preferably mended. Clearly from President Obama’s remarks this week, Ben is heading toward the door, time is running out for his grand plan to show its payoff.

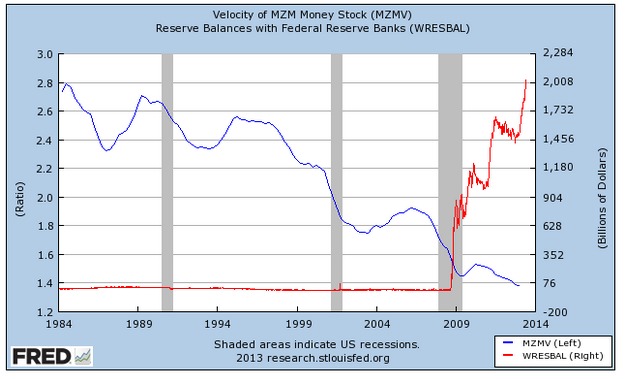

I can’t end this without a graph or two, to turn this from editorial to insightful analysis. First understand one piece of background. A bank has three things it can do with the money you put on deposit: 1. Lend it to a consumer or business 2. Invest it in securities 3. Give it to the Federal Reserve to hold in their account (the Federal Reserve is known as the Banks’ Bank).

Figure 1 is a chart from the Federal Reserve, The Red line shows the amount of money that banks have on deposit at the Federal Reserve. In four years or so this amount has ballooned from about $70 billion to over $2 trillion. The problem for the Fed and politicians is that this is the money that was supposed to find its way into consumers and businesses hands to spend, and fuel the recovery.

The Blue Line charts the “Velocity of Money” – easy concept, velocity is a way of showing how fast we turn over a dollar earned into a dollar spent. As indicated from the declining line, we are not turning over our money, we’re holding on to it. Good for savers and investors, but not so good for an economy that is 70% driven by consumer spending. In fact we have never been so slow to turn over the money we earn since 1960.

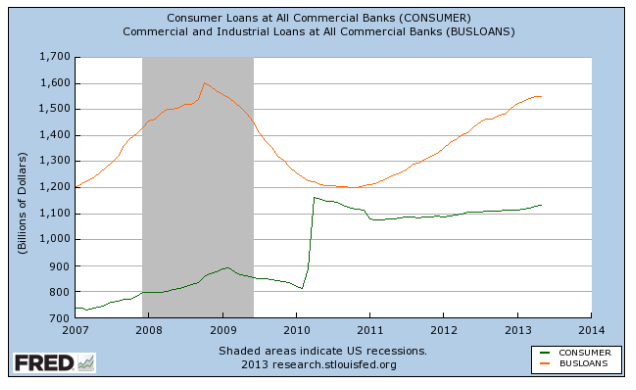

Below in Figure 2 are total consumer loans (Green Line) and business loans (Orange Line). Before looking close, look again at the Red Line in Figure 1. While money to lend (Red Line above) has skyrocketed, new demand for that money has been muted. In fact Business loans outstanding are still not back to peak levels nearly five years ago. While consumer loans popped up in early 2010 they are actually negative since.

Now back to getting those deposits out of the Federal Reserve and into consumer and businesses hands. Clearly from the low velocity number, there should be a low demand for extra money via loans. (Not to be confused with the extremely high demand for more money from employment and wage increases).

Conclusion

While I believe that Fed manipulation has caused more harm than good, unwinding it will not be easy. Especially if it fails to revive the economy from its current doldrums first. While Ben can throw money from a helicopter, it only does the economy good if we are willing to spend it, and spend it we clearly are not. If the stock market continues its slide, it won’t be from the fear of Fed tapering causing higher interest rates. It will be from the realization we are far closer to recession than an accelerating recovery.

Image: Medill DC