One of my recent purchases for my Healthcare portfolio on Covestor’s platform is Medtronic, Inc. (MDT). Being located in the Midwest, I am always proud of America’s most innovative companies originating in the ‘heartland.’ Medtronic is headquartered just north of Minneapolis in the city of Fridley. Medtronic has a classic history of American innovation. As the Medtronic website relates:

Today, we are the world’s largest medical technology company, but we come from humble beginnings. Medtronic was founded in 1949 as a medical equipment repair shop by Earl Bakken and his brother-in-law, Palmer Hermundslie. Did these two men set out to change medical technology and the lives of millions of people? No. But they did have a deep moral purpose and an inner drive to use their scientific knowledge and entrepreneurial skills to help others.

To learn more about the company, visit Yahoo’s company profile here. I first wrote up Medtronic on November 13, 2003 (excuse the typo on the entry that says incorrectly 2002). I then revisited this stock pick on November 29, 2009. One has to be impressed with the wide breadth of medical technology products coming out of this company and the continued innovation. In fact, in 2010 Medtronic was recognized by the Massachusetts Institute of Technology Review as one of the 50 most innovative companies in the world.

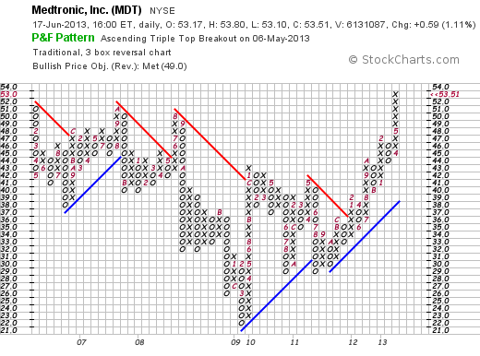

What really attracted me to the company last month was the strong technical strength of the stock as it began to clear past stock price ‘highs’ set in 2007 and 2008. As this StockCharts.com ‘point & figure’ chart shows, the company has had a better performance since bottoming out at about $21 in March, 2009, and has moved strongly ahead, at first with a sharp correction in May, 2011.

(click to enlarge)

To be sure, Medtronic (MDT) has found itself embroiled in controversy over the years with the Medtronic Infuse scandal being typical as accusations of payments from Medtronic to investigators publishing review articles. In May, 2012, the Department of Justice closed their investigation of Medtronic without finding any wrongdoing in regards to the Infuse Bone Graft product.

For the most part, this ‘overhang’ of litigation that has suppressed the stock price, from my perspective, has been removed. However, trial attorneys are still seeking plaintiffs for continued litigation against the company. In any case, the above chart appears to suggest that investors have breathed a collective sigh of relief with the Justice Department’s decision.

Part of the continued bump in the stock price has been the company’s latest financial results. On May 21st Medtronic reported 4th quarter results. Net income came in at $969 million, or $.96/share ahead of last year’s $991 million or $.94/share. Sales also grew to $4.46 billion against last year’s $4.3 billion. Adjusted earnings were $1.10/share ahead of analysts’ estimated $1.03 in earnings. Sales also exceeded expectations of $4.38 billion. The company raised guidance for revenue to $17.1 billion to $17.3 billion in 2014, ahead of FactSet estimates of $16.9 billion.

Reviewing the Morningstar.com financials on MDT, we can see that Medtronic is continuing to grow its revenue with $13.5 billion reported in 2008 increasing to $16.2 billion in 2012 and $16.4 billion in the trailing twelve months. More recently, the rate of revenue growth has decreased from rates of growth between 2008-2010.

Diluted earnings per share have grown from $1.95/share in 2008 to $3.41 in 2012 and a slight dip to $3.38 in the TTM. Outstanding shares have steadily decreased from 1.14 billion in 2008 to 1.03 billion in the TTM. Medtronic continues to actively buy back its own shares supporting some of the ‘per share’ results noted.

In terms of the balance sheet, Morningstar reports Medtronic with current assets of $9.5 billion, and current liabilities of $5.9 billion yielding a Current Ratio of 1.61. Medtronic increased free cash flow from $2.88 billion in 2008 to $3.97 billion in 2012 and $4.28 billion in the TTM.

Looking at some Key Statistics on Medtronic from Yahoo, we can see that this is a large cap stock with a market capitalization of $54.37 billion. The trailing P/E is a moderate 15.88 with a forward P/E (fye Apr 26, 2015) working out to 12.99. The PEG ratio, however, remains rich at 2.03 with only a modest growth in earnings expected.

Yahoo reports 1.02 billion shares outstanding with 1.01 billion that float. As of May 31, 2013, there were 10.64 million shares out short yielding a short interest ratio of only 2.0. (Under my own arbitrary 3 day rule for significance).

The company pays a dividend of $1.04 yielding 2%. The payout ratio is a moderate 31% suggesting ample room for possible further dividend boosts. The last time the stock was split was back in September, 1999, when shareholders got a 2:1 stock split.

To summarize, over the past several years Medtronic has been embroiled in some controversy regarding research results and payments to investigators. The Justice Department has found no evidence of significant wrongdoing and has closed its case. The company, meanwhile, has continued to generate cash, using it to pay an increasing stock dividend and purchase back its own shares.

The company produces many innovative products spanning multiple fields of medicine from Orthopedics, to Cardiology to Nephrology. It is unnecessary to remind anyone that as our population ages and as more people in this country through the Affordable Care Act (‘Obamacare”) and overseas through growing middle class populations in nations like India and China find their access to healthcare improving, that purchases of medical devices by practitioners is likely to continue to grow.

Finally, in my opinion, after years of essentially going ‘nowhere’, the stock appears to be breaking out and demonstrates positive price momentum. Like all of my purchases, I always reserve the right to sell any position on either technical or fundamental weakness, a discipline I believe is essential to success in investing.

The investments discussed are held in client accounts as of May 31st, 2013. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.

{kind=link}

{kind=link}