Author: Bill DeShurko, 401 Advisor

Author: Bill DeShurko, 401 Advisor

Covestor model: Dividend and Income Plus

The Dividend and Income Plus portfolio has lagged the overall market since mid-June when the recent market rally started. The portfolio has maintained a 20% cash weighting and has continued to hold our “low beta” selection of dividend paying stocks.

The rationale to remain in “coast” mode is that in my opinion the rally has been primarily fueled by Mario Draghi’s comment that the ECB stood ready to take “any action necessary” to preserve the Euro and by extension the EU, including Greece. The problem is that the ECB does not have the authority to follow through on such statements.

Simply put, the ECB is prohibited from “printing” the money they would need to implement a U.S. style round of quantitative easing (QE). It is pretty well accepted, that absent such action, there is just not enough economic backing to backstop the financial bleeding in Europe.

The bull argument continues with the “bad news is good news” theme. With China’s economy softening, U. S. economic data “softening” at best, the economic stage is being set for a global simultaneous easing from China, the U.S. and Europe.

The best bull argument is that things are getting worse, so there has to be Fed intervention which would fuel a global rally. I am not willing to buy into that scenario. However, if we actually see such action come to fruition, we will change the look of our portfolio, jump on the bandwagon, and look for higher beta (more aggressive holdings) to capture gains if the rally truly emerges. With the risk to the markets extremely high if such hopes don’t materialize, I will wait for the central banks to literally “show me the money” before making a commitment with client’s hard earned investment dollars.

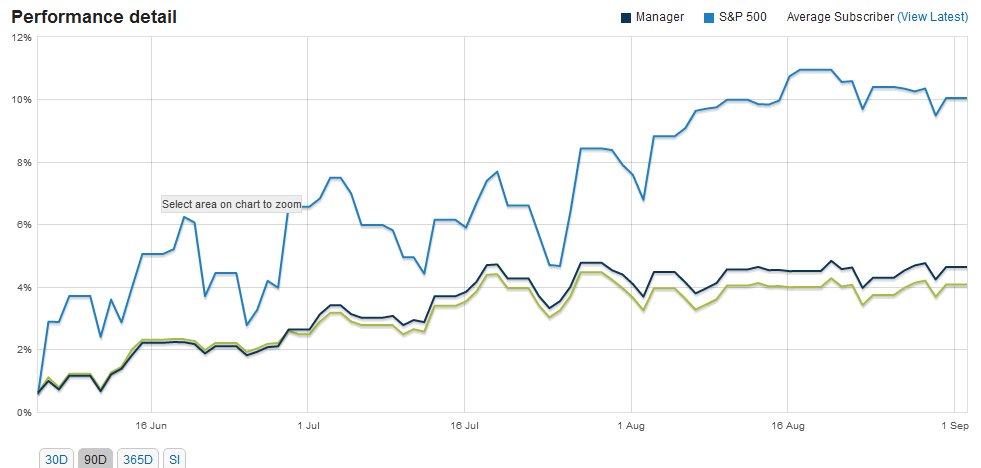

Below is a screen shot from Covestor.com comparing my Dividend and Income Plus Portfolio to the S&P 500 for the prior 90 days. While the underperformance is clear, so should be our lack of volatility. In fact the portfolio sports a beta of .63, or a volatility measure of 37% less than the S&P 500. And even with our 20% cash position, the portfolio is sporting a very healthy 4.5% dividend yield as of late August.

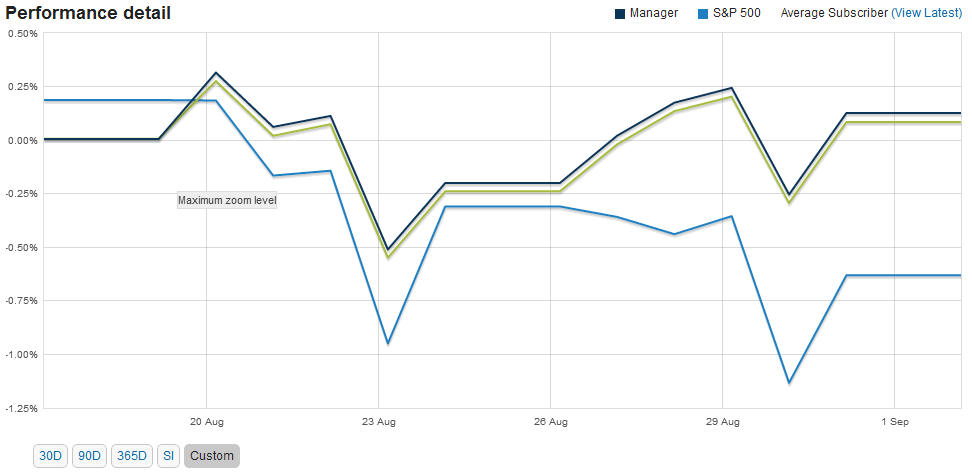

Combining the low volatility with the dividend yield, we are extremely happy with our overall performance, especially for the risk adverse income investor, such as a current or near retiree. Furthermore, looking at the graph below, again from covestor. I zoom in our recent performance.

Since the recent market peak on August 17th, the portfolio has outperformed the market by .7% over just two weeks.

I expect September to be a volatile month and expect to close the recent gap in relative performance with the S&P 500. Primarily by maintaining value while the S&P 500 corrects. I hope to be true to our motto, “It is not what you make, but what you keep that matters”.