Author: Dan Plettner

Author: Dan Plettner

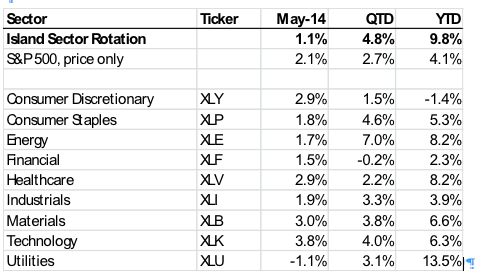

Covestor models: Pure Short Opportunistic, MLP Direct Ownership, Taxable Income, Well-Intentioned Activism, Long/Short Opportunistic, Core

Greater China Fund (GCH) recently announced that an absolute majority of shareholders voted to terminate the advisory agreement with Baring Asset Management. Greater China Fund’s board had failed to respond to the needs of value-minded shareholders last year.

Alpine Global Premier Properties (AWP) earlier this month completed what appears to have been a very effective tender offer for both management and shareholders.

Shareholders who desired liquidity near net asset value (NAV) achieved 95 cents on the dollar while exiting about four-fifths of their position. The transaction was clearly NAV-accretive for all shareholders and the company quickly thereafter affirmed the 5 cent per share monthly distribution for July through September.

New Ireland Fund (IRL) completed a tender which was proportionately (and in absolute terms) much smaller. The pro-rated sell rate for tendering shareholders was also smaller. Its discount widened substantially post tender. I recently added to my position at the widened discount. My instinct wants to believe the board will resume NAV-accretive share buybacks to create value and tighten the discount.

If IRL showcases exemplary governance, I believe IRL would prove itself a far superior long term vehicle to the competing ETF. If the board fails to demonstrate good governance, I’ll be watching for a large block trade of Bulldog’s 9% remnant position to an alternate proxy-competent entity. That Bulldog hasn’t filed further selling post-tender at market suggests a delayed block trade to an entity like Karpus or the Horejsi Group is a particularly viable option.

Speaking of the Horejsi Group, the Boulder Growth and Income Fund (BIF) Derivative Suit Settlement Fairness Hearing is scheduled for July 28th. In full disclosure, I am in the process of composing my own objection because I see nothing in the proposed settlement’s design that meaningfully benefits normal shareholders.

The prospect of increasing the billable assets under management to remedy a path which benefitted the advisor as normal shareholders’ value diminished appears ironic. While I have asked the attorneys on record what competency the mediator has in closed end funds, my question has not been answered. The discount has actually widened to an outlier among closed end funds after terms of the proposed settlement were released.

I can barely fathom how insurers would be convinced to pay $3 million without an advisor relenting any of its asset captivity whatsoever – particularly should a judge decide to apply the criminal fraud statute to allow for limited discovery.